FTSE drops as commodity stocks hit by falling metal and oil prices

After a relatively calm open, the European stock markets have turned decisively lower, with the UK’s FTSE 100 dropping some 1.1 per cent at the […]

After a relatively calm open, the European stock markets have turned decisively lower, with the UK’s FTSE 100 dropping some 1.1 per cent at the […]

After a relatively calm open, the European stock markets have turned decisively lower, with the UK’s FTSE 100 dropping some 1.1 per cent at the time of this writing. Shares in energy and in particular mining companies are taking the brunt of the sell-off today, tracking weaker commodity prices. The price of iron ore has hit its lowest level since 2005 while crude oil is trading at levels not seen since the Global Financial Crisis. Crude oil’s selling is a continuation of the renewed pressure that began on Friday after the OPEC meeting ended with the cartel failing to even agree on an oil production ceiling. Commodities are generally falling mainly because of excessive supply and concerns about future demand as China’s economy slows down.

The latest data from the world’s second largest economy paints a bleak picture as exports there fell for the fifth consecutive month, down 6.8% in November from a year-ago period, while imports declined 8.7%. Unsurprisingly, miners such as Anglo American, Glencore, BHP Billiton and Rio Tinto were dominating the bottom half of the FTSE with large losses of 6 to 10 per cent. Anglo American was the worst performing stock, hit by news the company is suspending dividends until the end of 2016, owing to the “severity of commodity price deterioration…” The miner is planning to cut down its business divisions to three from six as it seeks to trim its assets by 60% and reduce workforce. This sort of unfortunate news and industry consolidation are stories likely to make headlines going forward until at least the commodity market adjustment ends, which could take several months at the very least. With the FTSE dominated by miners and energy stocks, it isn’t going to be pretty.

The UK economy is also not looking great. Today’s data shows that manufacturing production fell 0.4% month-over-month in October compared with forecasts of a small 0.1% drop and a rise of 0.8% the month prior. Industrial production increased just 0.1%, though this was in line with the expectations. Earlier, the Halifax House Price Index (HPI) came in at -0.4% month-over-month versus -0.1% expected.

But generally speaking, the European and U.S. economic calendars are light this week and the focus remains on China after the disappointing trade number and ahead of the inflation data on Wednesday. The next big event for the stock markets is likely to be next week’s much-anticipated Federal Reserve policy meeting. The slightly stronger U.S. November jobs report has strengthened the case for the Fed to increase interest rates for the first time in almost a decade at its December 16 policy meeting. But given that the ECB stopped short of expanding the size of its monthly asset purchases, the Fed may well deliver a so-called “dovish” rate increase in order to stop the dollar from significantly appreciating against the euro and other currencies. A potentially dovish Fed may help to support stocks. It could, however, be a long wait until next Wednesday for the stock market bulls.

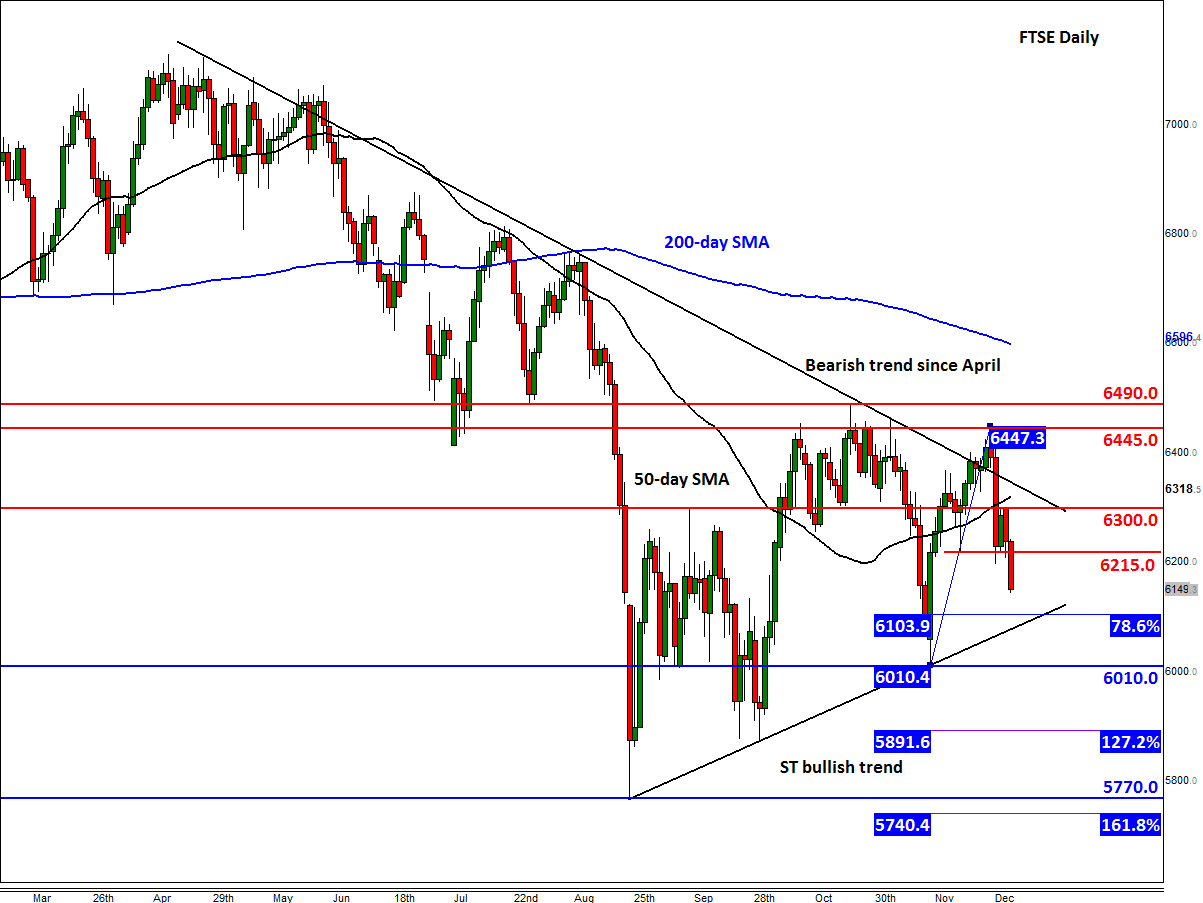

As far as the FTSE is concerned, the UK benchmark stock index continues to break down short-term support levels such as 6300 and 6215 most recently. These levels may turn into resistance upon re-test. A bearish trend line that has been established since the index peaked in April is still intact and the moving averages are in the “wrong” order, with the 50-day SMA below the 200. So, the trend is bearish as things stand. It could get worse for the bulls if the index breaks a short-term support that comes in around the 78.6% Fibonacci level of the most recent bounce at 6100. A particularly bearish development would be if the index forms a new lower low and break last month’s low of 6010. If seen, the FTSE could easily revisit this year’s earlier low of 5770 before it decides on its next move.