FTSE arrives at key technical juncture as Chinese concerns mount

Another lacklustre session has come to pass for European equity markets. Investors’ appetite for stocks has diminished notably in recent times, largely because of concerns […]

Another lacklustre session has come to pass for European equity markets. Investors’ appetite for stocks has diminished notably in recent times, largely because of concerns […]

Another lacklustre session has come to pass for European equity markets. Investors’ appetite for stocks has diminished notably in recent times, largely because of concerns about the possibility of a sharp slowdown in China, the world’s second largest economy, and the lack of economic growth in the Eurozone in spite of the ECB’s on-going QE stimulus programme and a weaker euro. Commodity prices have been hammered not only because of concerns over the health of the Chinese economy but also due to oversupply reasons. Copper prices for example have dropped to a fresh 6-year low today and crude oil is continuing to bleed lower due to growing supplies from the OPEC. The PBOC’s decision to sharply devalue its currency last week is another major deflationary force which could lead to a drop in demand for not just commodities but also luxury goods such as German cars.

Among the major European indices, the UK’s FTSE is one of – if not the most – heavily exposed markets to China due its large number of commodity-linked constituents. Unsurprisingly, the index has been making a series of lower lows in recent times and the index is currently finding itself below all its main moving averages, including the 200-day.

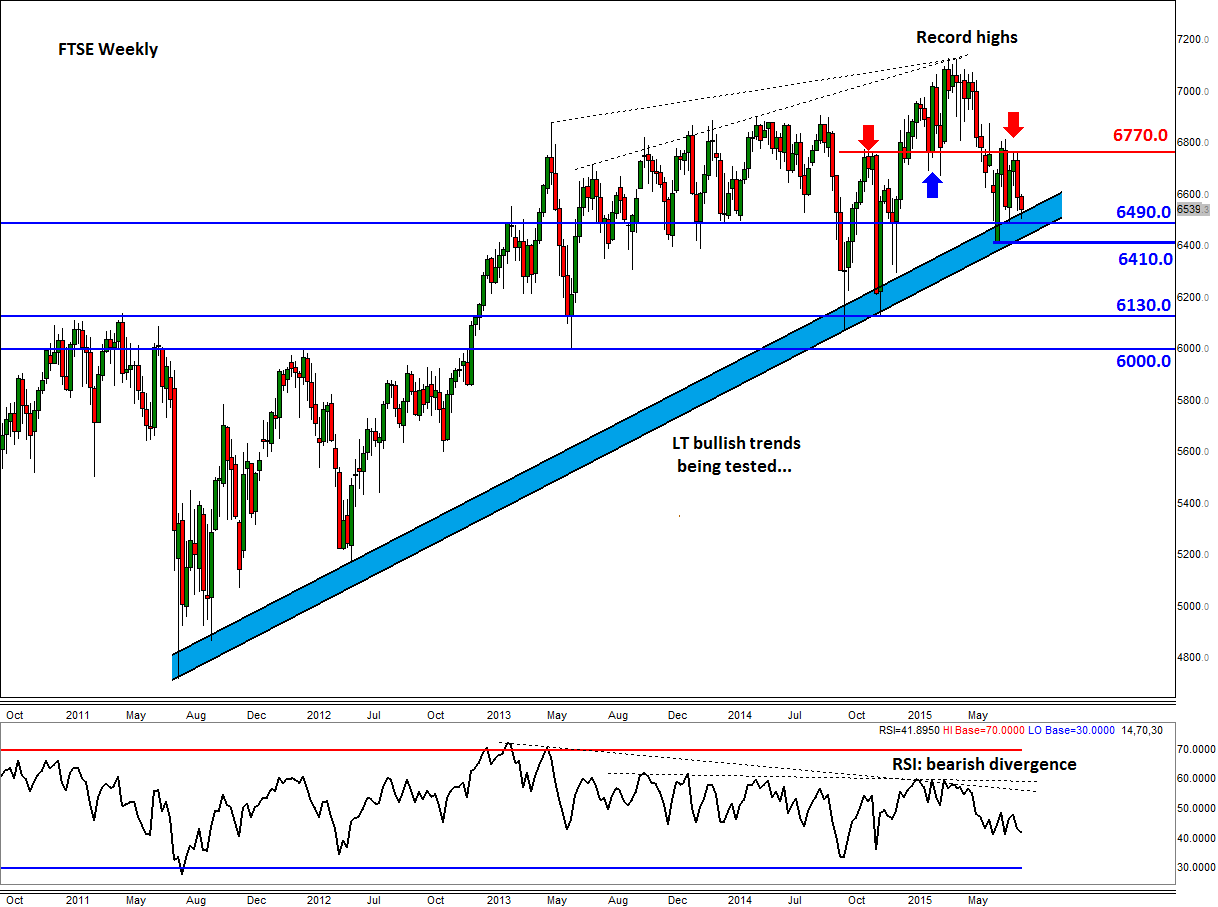

Today we are looking at the long-term weekly chart. As can be seen, a general trend line has been in place since mid-2011. This has provided strong support on numerous occasions, including twice in July when we were at height of the Greek crisis 2.0. Though the FTSE may once again find some support from this trend line, the probability of a breakdown is quite high this time for after all the fundamental outlook is looking bleak.

Indeed, if the index falls through the rising trend range, and take out the July low of around 6410 then things could get really ugly. Should this scenario play out, the index may then go on to drop to the next support of 6130 at the very least. What it may do thereafter will depend on the market sentiment at the time, but for the index to drop all the way to 6130, there is no reason why it can’t reach or indeed break 6000 next.

Conversely, if the bulls show their presence around these levels, then the FTSE may stage a relief rally all the way back to the top of the recent range, around 6770. This is also where the 200-day average comes into play. The long-term bias would turn bullish once more if it manages to break and hold above 6770.

I am currently neutral on the FTSE and will hold that view while it hovers around the long-term trend line without showing a clear signal about the near-term direction.