French election Correlations start to rise as investors get nervous

At City Index we have been taking a look at correlations this week, specifically how the S&P 500 has experienced a break down in its […]

At City Index we have been taking a look at correlations this week, specifically how the S&P 500 has experienced a break down in its […]

At City Index we have been taking a look at correlations this week, specifically how the S&P 500 has experienced a break down in its relationship with other risky assets. One correlation that is, unsurprisingly, holding up, is the relationship between French 10-year bond yields and European stock indices.

We would expect French bond yields and European stocks to be highly correlated as we lead up to the French election, the first round of voting is on 23rd April. With just over a week to go, the race is getting more interesting as the Far-Left candidate Melenchon is seeing his support surge, while front-runner Macron has seen his chances of winning the keys to the Elysee Palace dip from last week’s high. The risk is that the far left and the far right make it into the second round run-off. Although this outcome still has a slim probability, the market is showing signs of nervousness about a shock result from the French election.

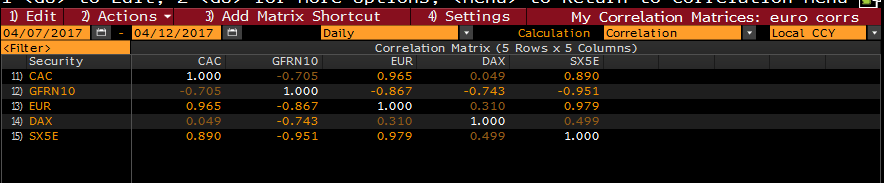

The correlation matrix below shows the short –term correlations between the Cac 40, French 10-year bond yield, EURUSD, Dax and the Eurostoxx index.

Figure 1:

Source: City Index and Bloomberg

Here are a few conclusions: