Emmanuel Macron’s tough love and Johnson’s threat to pull his deal sets the pound up for a rougher week ahead

Could France, the only country not to have supported giving Britain an extension till the end of January, really be riding to Boris Johnson’s aid?

The speculation is that France’s President Emmanuel Macron blocked an EU attempt to delay Brexit for three months, raising the prospect that the government could remain in the dark re. an extension until just hours before the 31st October deadline. The idea is that this ‘tough love’ would be an incentive for UK lawmakers to approve PM Johnson’s deal. They’ve agreed to it but rejected his fast-track formula for pushing it into law. Macron favoured an extension till 30th November, or even sooner. Other EU 27 leaders baulked at the higher no-deal risks that gambit would entail.

The internal EU impasse helped delay a decision till Monday, after Parliament has voted on Johnson’s latest call to end the Brexit “nightmare” with an election, on 12th December. But he needs a two-thirds majority in Parliament to get one, and Labour is still saying it won’t get behind an election till….yep, the EU grants an extension. We’re going around in circles, and the pound is slipping even further from Monday’s 5-month highs. Assuming Johnson loses the motion for an election and the EU okays an extension, the pound could stabilise again. However, the PM’s aides are already murmuring that he may scratch his Brexit bill entirely if he loses the vote, due to the risk of further amendments that could require the re-opening of discussions with Brussels. Some clarity will come by late Monday, though not much.

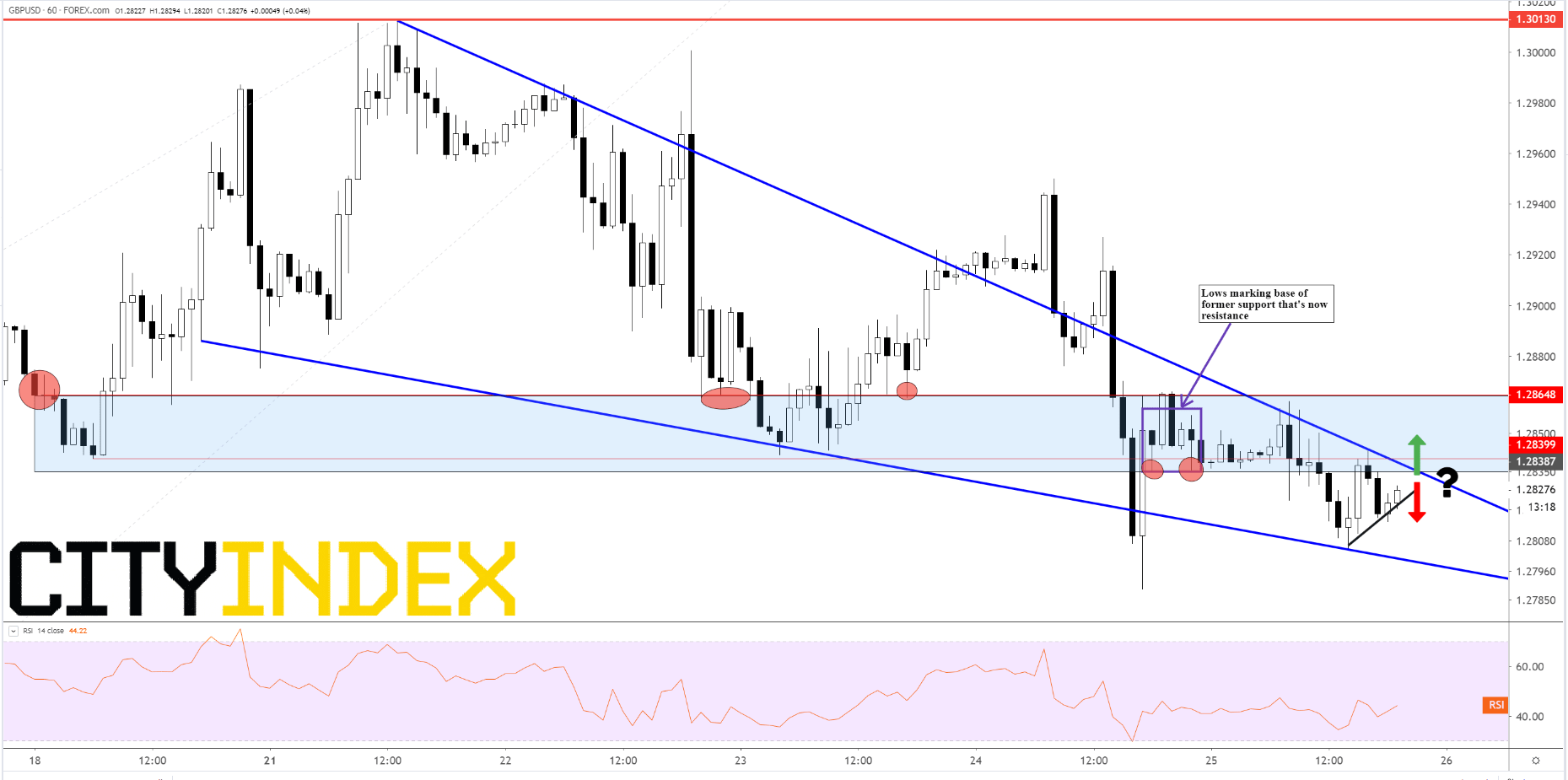

Chart thoughts

The short-term view makes clear rising risks to the closely watched mid-$1.28 levels that have provided critical support over the last week. A top almost at $1.30 dead at the beginning of the week has been followed by a down leg that’s chopped away at the band of lows mapping the region of prior support, and hence switching it to resistance:

- Most recently circa $1.2835: notched by two late-NY session hourly lows from Thursday

- Multiple tags close to $1.2865 concentrated on this mid-week and late last week

Price action, which has in this session drifted higher, suggesting at least some profit taking, now posits the question of whether cable is ready to attack the region anew, though this time from the underneath, heading back up.

GBP/USD – Hourly [1945 BST 25/10/2019]

Source: City Index

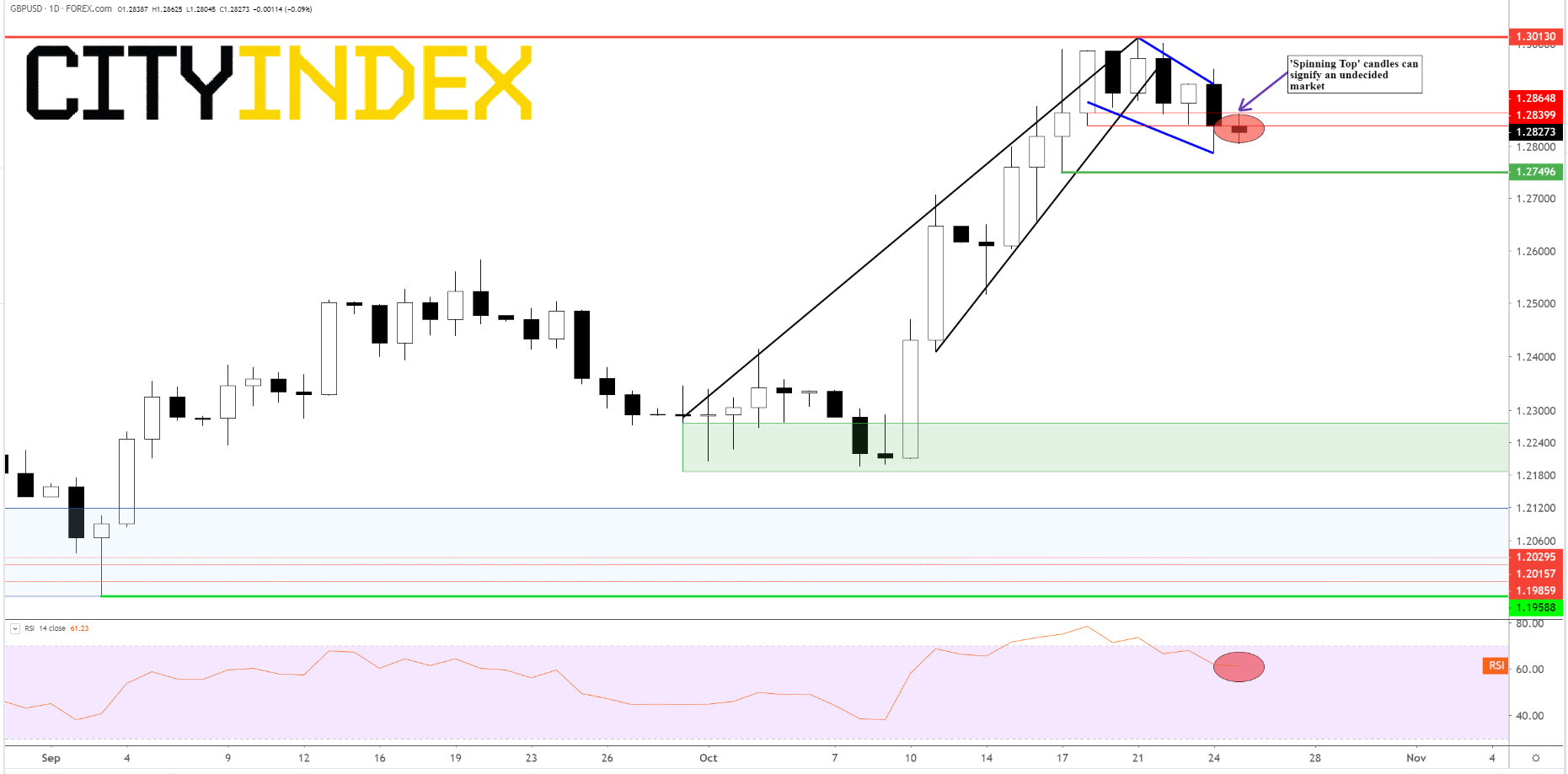

The possibility of a bullish continuation becomes clearer in somewhat wider focus, where the reversal since 21st October forms what could be deemed a bull flag, given appropriate corroboration. Friday’s ‘Spinning Top’ candle – upper/lower shadows that exceed the small body – can signify indecision to the extent of near stasis. Succeeding sessions must break its range to indicate the market’s ready to move.

Note the top nuzzles what’s now the intermediate resistance of $1.2865. With RSI turning lower, odds don’t appear to favour a sustained break higher sometime soon, suggesting a visit to $1.275 – confirmatory low on 17th October – should be expected sooner. A break of the latter could thereby bring final invalidation of October’s bull trend.

GBP/USD – Daily [2015 BST 25/10/2019]

Source: City Index

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Johnson articles

July 6, 2022 07:11 AM

June 6, 2022 10:24 PM

December 23, 2020 01:29 PM

December 14, 2020 03:00 AM