Four Years Later Still Shocking amp Awing

The barrage of bailouts & stimulus packages (fiscal & monetary) delivered since the Lehman collapse four years ago this week will not diminish the importance […]

The barrage of bailouts & stimulus packages (fiscal & monetary) delivered since the Lehman collapse four years ago this week will not diminish the importance […]

The barrage of bailouts & stimulus packages (fiscal & monetary) delivered since the Lehman collapse four years ago this week will not diminish the importance of the remarkable double-shot from Bernanke & Draghi this month.

Three rounds of quantitative easing from the Fed, four rounds of QE from the Bank of England, five bailouts from the eurozone, two waves of bond purchase programs and two rounds of Long Term Refinancing Operation from the ECB. Result: G7 policy rates are at or near zero and equity markets are 5-10% away from their record highs. Yet, as eventful as the four years have proven, the first two weeks of September 2012 rank high in relevance & lack of precedence.

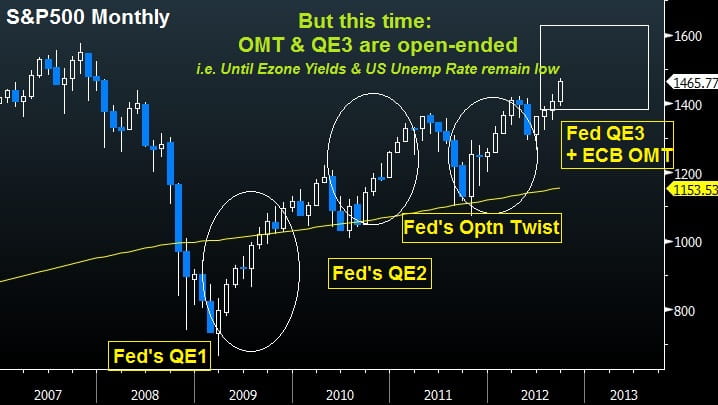

Draghi & Bernanke: Still Shocking & Awing

Draghi’s Outright Market Transaction programme stands out from prior bond purchase plans via its ability to combine conditionality (countries must abide by Troika rules rather than selecting bonds arbitrarily), sterilisation (counter inflationary concerns by later mopping up liquidity) and unlimited purchases (another way of capping bond yields without specifying it). Most of all, the OMT has integrated monetary policy into fiscal policy, i.e. requiring nations to abide by fiscal rules in order for their bonds to receive monetary stimulus. Draghi’s OMT may not be a direct solution to Europe’s high debt/low growth problem, but it buys invaluable time for national governments to pursue their austerity policies by keeping yields in check and markets supported.

The Fed’s QE3 differs from previous programs in its open-ended nature to target the labour market and its willingness to see higher inflation surpassing 2% with the aim of reducing unemployment below the stubborn 8% figure. The Fed did not mince its words when it stated: “…without further policy accommodation, economic growth might not be strong enough to generate sustained improvement in labor market conditions.”

Buying the Rumour and the Fact?

One remarkable aspect of Draghi/Bernanke policy action is that rarely have markets rallied ahead of anticipated events and continued to do so after their materialisation. So there we have it; Draghi vowing to spend unlimited amounts to drag down bond yields and Bernanke willing to extend monthly purchases indefinitely, until unemployment declines and remains below 7%. Such unprecedented policy-making may be just what the doctor ordered for equity bulls to revisit their 2007 record levels and metals to return to last year’s highs.