Formal Removal of BoJ Rule Key to Yen Weakness

As the yen rises back to its old ways, the Bank of Japan is pressured to step up its dovish talk ahead of this week’s […]

As the yen rises back to its old ways, the Bank of Japan is pressured to step up its dovish talk ahead of this week’s […]

As the yen rises back to its old ways, the Bank of Japan is pressured to step up its dovish talk ahead of this week’s two-day policy meeting. It’s interesting that the central bank first won its independence in the mid 1970s as part of its fight against double digit inflation, before losing it to bureaucrats to combat nearly two decades of disinflation.

Going into Thursday’s decision, there is chatter that the BoJ will begin open-ended asset purchases immediately rather then wait until 2014, and may also consider a new target to buy longer-dated bonds.

The BoJ’s asset purchases are currently composed of two programs:

i) Asset purchase program (APP), under which it aims to buy ¥101 trillion yen by end of 2013 via assets of no more than three years;

ii) Outright purchases of JGBs (21.6 trillion yen) known as “rinban” purchase program, targeting durations up to 30 years, but the majority of which have maturities of 10 years or less.

Under consideration, is an increase in the amount of assets buys and extending the duration of APP bonds to five years or longer, from the current three years.

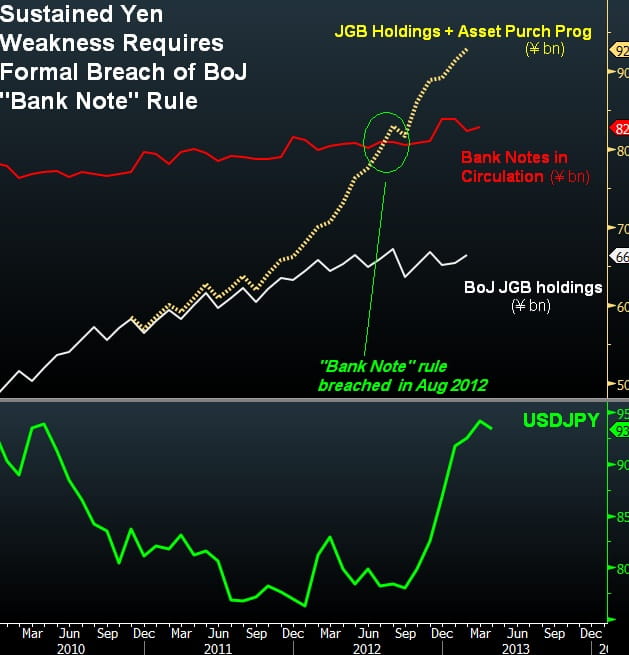

Will bank note rule be removed?

There is also the contentious “bank note rule”, which stipulates that total asset purchases by the central bank may not exceed total bank notes in circulation so as to avoid monetizing of the debt. Yet, the rule has been breached since last summer, when the aggregate amount of asset purchases (operations under asset purchase program combined with BoJ’s regular holdings of JGBs) exceeded the notes in circulation for the first time since the APP began in 2010.

As of February, the combined purchases of APP operations and regular JGB purchases amounted to ¥92 trillion as of March, further exceeding bank notes’ circulation of ¥82.8 trillion. Although increased purchases have breached the “bank note” rule seven months ago, the BoJ may have to formally announce the removal of the rule as a policy signal to further expand its balance sheet.

JPY bulls will wish for a split vote within the nine-member Policy Board, or an expansion in purchases that is less than demanded by Governor Kuroda. USD/JPY breached its three-month trendline support as part of a broader yen recovery, which emerged partly on signs of possible obstacles to broader BoJ activism. Weekly momentum indicators suggest a worrying convergence to the downside, which is likely to spell out 91 by mid-April. In order for USD/JPY to avoid a weekly breach of the said trendline, USD/JPY must close Friday at or above 93.70. This is unlikely to be the case for now, with any recovery seen capped near 94.40-50 for now.