FOMC watch 1 month to go until the next Fed meeting

September 17th is a date to circle in your diary, it is the next FOMC meeting, when there is a chance that the Fed may […]

September 17th is a date to circle in your diary, it is the next FOMC meeting, when there is a chance that the Fed may […]

September 17th is a date to circle in your diary, it is the next FOMC meeting, when there is a chance that the Fed may raise interest rates for the first time in 9 years. This is causing flutters of excitement throughout the market, but what is the real chance of a rate rise from the Fed in the coming weeks?

There are two answers to this: one from economists and one from the market. Looking at economists first, 87% expect the Fed to raise rates to 0.5% on 17th Sept, only 6 out of 27 polled by Bloomberg thought rates would remain at 0.25%. Although economist estimates may change between now and then, this seems to be a ringing endorsement that the Fed will hike rates next month.

However, economists may not be putting their money where their mouth is, as the market is only pricing in a 50% chance of a rate hike from the Fed next month, according to Fed Funds futures. This rises to a 75% chance of a hike by December, and a 90% chance of a hike by April 2016.

How do we interpret this disparity between economists and the market?

What does this mean for the market?

One could argue that the Fed Funds futures’ lack of faith in the prospect of a rate rise has stymied the dollar’s progress, as you can see below, and the dollar index remains trapped in a range. However, if the economists are correct then we could see a big bounce in the buck as the market rushes to adjust its future interest rate expectations.

For now, we expect the dollar to be 1, relatively range bound and any rallies could be capped by key resistance levels, and 2, the dollar could be super sensitive to economic data and speeches by Fed members in the coming weeks, which could increase volatility in the key dollar pairs.

In contrast, uncertainty about a rate hike is likely to be good news for the stock markets, and we could see European and US indices drift higher into the meeting.

The technical view:

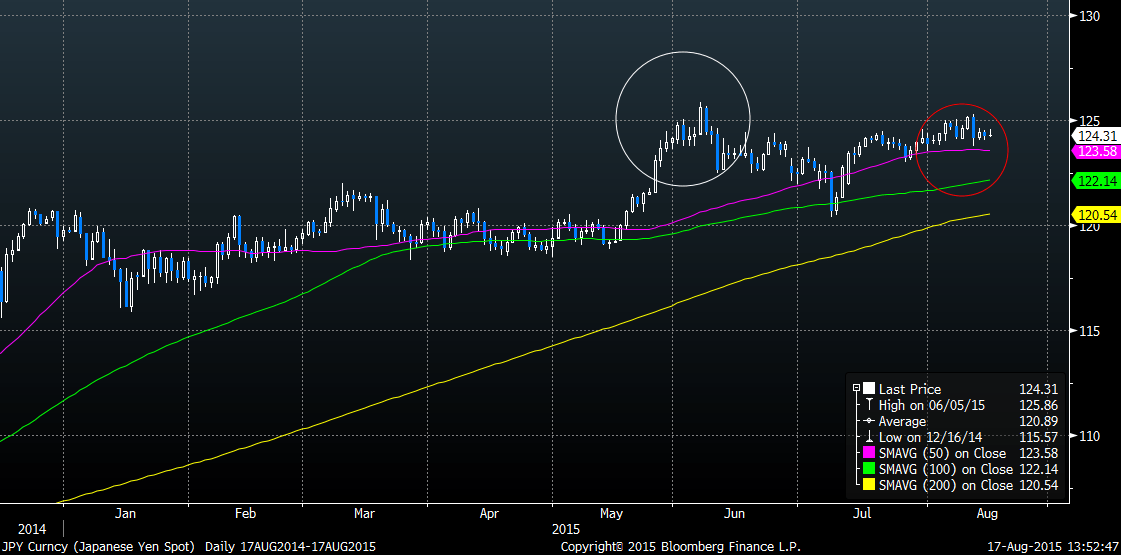

USDJPY has been unable to break above 125.00 resistance even on the back of this morning’s weak Japanese GDP report. Interest in this pair has started to dwindle and the daily range has shrunk, possibly on the back of mixed messages around the prospect of a Fed rate hike.

In the short-term, below 124.60 resistance opens the way to 124.00 and potentially 123.75. As long as 124.60 is not breached to the upside, then a break below 124.00 in the next few days may be likely, especially if we see weak US CPI or a dovish hint to this week’s FOMC minutes then 124.00 support could be vulnerable.

In the longer term, we think that the market could be cautious about pushing this pair above the 6th June high at 125.86 until we get a clear signal from the Fed (or the market) that a rate rise is coming.

Figure 1: USDJPY gains could be capped as we wait for clearer signals from the Fed.

Source: Gain Capital: Data: Bloomberg