FOMC Statement Comparison 8211 Oct 30 vs Sep 18

Today’s FOMC announcement to keep total asset purchases unchanged at $85 bn was no surprise, but the fact that the Fed sees improvement in the […]

Today’s FOMC announcement to keep total asset purchases unchanged at $85 bn was no surprise, but the fact that the Fed sees improvement in the […]

Today’s FOMC announcement to keep total asset purchases unchanged at $85 bn was no surprise, but the fact that the Fed sees improvement in the economy despite “fiscal retrenchment” has somewhat boosted the US dollar.

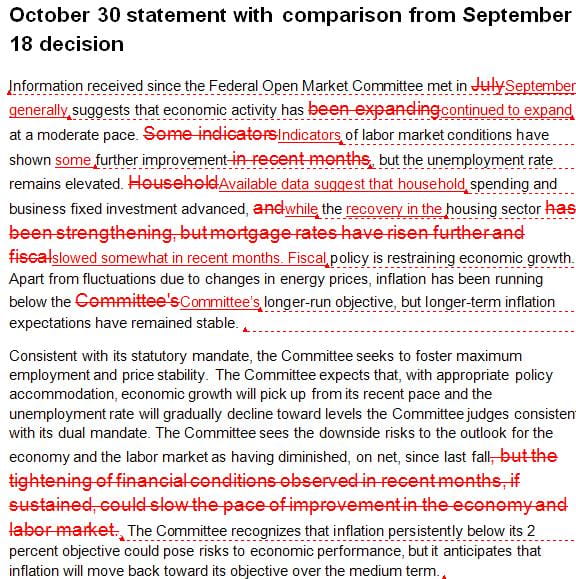

As we can be seen in the red-line comparison to the September 18 FOMC statement, the Fed removed the reference to the “tightening of financial conditions observed in recent months”, which was effectively diminished by last month’s unexpected decision to not taper asset purchases.

The Fed could not have managed today’s statement without one aspect of improvement as that would have triggered renewed acceleration in the USD’s decline. Rather than focusing on the Fed’s editorial skills, the fact remains that the US economy lost 0.6% of output in Q4 from the partial government shutdown and the only constant from the Fed over the last 3 years has been downward economic revisions after previously overestimating growth.

Despite continued declines in the unemployment rate nearing 7%, the fiscal reality remains that the US economy flirted with a 16-day government shutdown, a last minute hike of the federal debt ceiling and the postponement of these impasses to no later than the first quarter of next year.

The next deadline to watch is December 13, when the budgetary negotiations are set to resume.

Next Trick is the “Inflation Floor”

One of the constant remaining in the FOMC statements is that “inflation has been running below the [Fed’s] longer run objectives”, which has been a durable supporting point for the hawks. Policy guidance has primarily focused on a threshold for the unemployment rate, but last month’s comments from Chairman Bernanke suggested setting an “inflation floor” as a “sensible modification to the guidance”. If Fed chairwoman to be Janet Yellen implements an inflation floor, then this could be a successful means of slowing down rising yields as long as falling unemployment is not accompanied by a recovery in inflation. The Fed’s preferred inflation figure, core PCE price index, is near 2 ½ year lows of 1.2%. Further declines nearing 1.1% could render the inflation forward guidance to become a carte blanche for further awaiting that 6.5% unemployment rate without fretting about the need for higher interest rates.

October 30 statement with comparison from September 18 decision