FOMC Instant Reaction Nearly There but Further Improvement Needed

Analysts and traders were unanimous in their expectation that the central bank would leave interest rates unchanged in the 0.00-0.25% range, and the Fed provided […]

Analysts and traders were unanimous in their expectation that the central bank would leave interest rates unchanged in the 0.00-0.25% range, and the Fed provided […]

Analysts and traders were unanimous in their expectation that the central bank would leave interest rates unchanged in the 0.00-0.25% range, and the Fed provided no surprises on that front. That said, the world’s most important central bank still gave traders plenty to chew over in its first monetary policy statement of Q3.

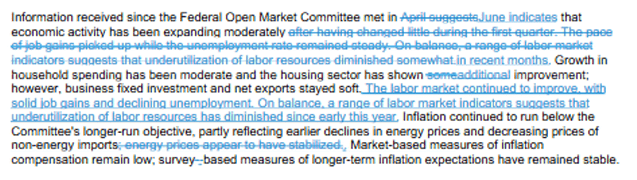

First, the headlines from this month’s statement [emphasis mine]:

Earlier today, analysts coalesced around watching for one word in the statement, mirroring the intense focus on the phrase “considerable time” from earlier this year. In this case, the word was “nearly,” as in “The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced,” with some commentators suggest that the central bank could remove this word as a nod toward a possible rate hike in September. As the above headlines show, the FOMC left that word in the statement, marking a potential negative sign for the prospects of a September rate hike.

Beyond that one word, there were a few other seemingly dovish tidbits in today’s statement. For one, the committee declared it still wanted to see “some further” improvement in the labor market before raising rates, despite the stellar growth over the last several months. More to the point, the decision to leave interest rates unchanged was unanimous, disappointing hawks who were hoping that at least one member could dissent in favor of hiking interest rates immediately.

As ever, the central bank remains “data dependent,” and with the highly-anticipated September meeting a mere seven weeks away, markets could turn more volatile as traders update their expectations for Fed liftoff and (over)react to every headline.

Market Reaction

In our view, the most important market to watch in the wake of key economic data for the next few months will be the Fed Funds Futures market, which shows the probability that traders assign to an interest rate hike. In the lead up to the release, these traders were pricing in just a 19% chance of a rate hike in September, 36% odds of an increase in October, and a 55% probability of a hike in December; as of writing, these odds have shifted to 17%, 35% and 54%, respectively. In other words, traders were rather nonplussed by today’s statement, only marginally pushing back their expectations for a rate hike.

There was hardly more volatility in other markets, with the US dollar ticking higher in a possible “sell the rumor, buy the news” reaction, US equities spiking before pulling back to essentially unchanged, and the yield on the benchmark 10-year treasury bond falling 3bps from the day’s high to trade back at 2.27%.

Source: City Index

Source: City Index