FOMC Instant Reaction A Not So Dovish Hike

Yesterday, we published our preview for today’s Federal Reserve meeting, highlighting five things for traders to evaluate in their “Fed-mas lists.” For consistency, we’ll recap […]

Yesterday, we published our preview for today’s Federal Reserve meeting, highlighting five things for traders to evaluate in their “Fed-mas lists.” For consistency, we’ll recap […]

Yesterday, we published our preview for today’s Federal Reserve meeting, highlighting five things for traders to evaluate in their “Fed-mas lists.” For consistency, we’ll recap each of those five factors in turn, as well as what they may mean for traders:

1) The interest rate decision (14:00 ET, 19:00 GMT)

There were no surprises whatsoever on this front: the Federal Reserve raised interest rates 25bps to a range of 0.25%-0.50%, as almost every analyst and trader expected. There were a few dovish holdouts, but by and large, this as-anticipated decision had minimal impact on the markets.

2) The monetary policy statement (14:00 ET, 19:00 GMT)

Here’s where we started to have at least a little ambiguity about the world’s most important central bank would do. With the historic change in policy from the Fed, the statement was changed more than usual from the last meeting, but most of the changes were procedural in nature. In terms of meaningful updates, the central bank noted that the labor market “shows further improvement” and “continues to strengthen,” while also highlighting that the risks to economic activity were “balanced.”

The biggest update to the statement was the addition of one phrase: “gradual adjustments in the stance of monetary policy.” This is the Fed’s way of stating that it won’t start raising interest rates at every single meeting next year, though the accompanying economic projections still lay out a relatively aggressive normalization path – see below. It’s also worth noting that the decision to raise interest rates was unanimous. Overall, the Fed accomplished its goal of telegraphing its decision and statement, leading to minimal disruption in the market.

3) The summary of economic projections (14:00 ET, 19:00 GMT)

In our view, this was potentially the most important element of today’s entire Fed festivities. Starting with the economic forecasts, the FOMC slightly revised up its forecasts for GDP growth in 2016, while revising down its forecasts for the unemployment and inflation rates next year. Overall though, these minor tweaks to what are, at their core, guesses anyway, had little impact on the market.

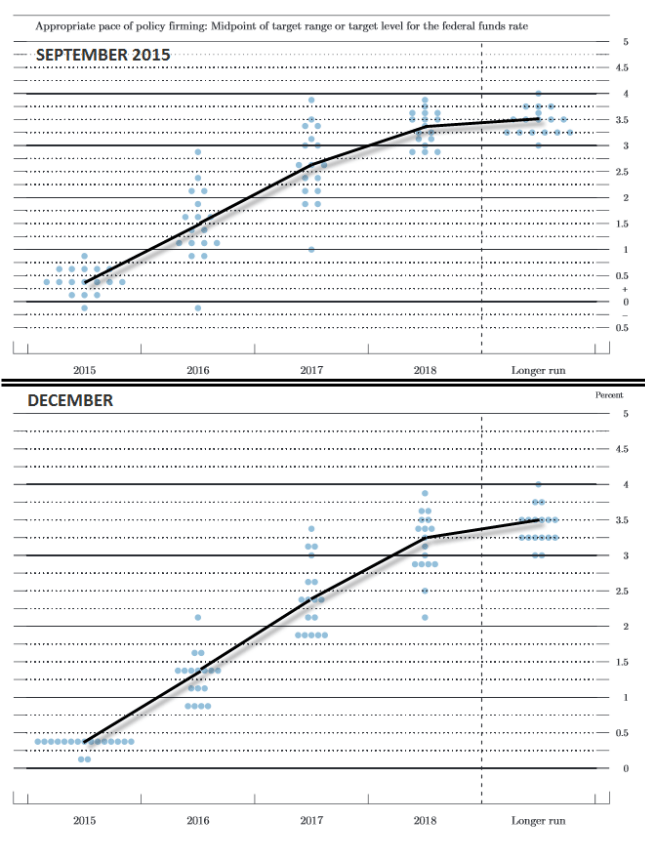

Maybe the most surprising (non-)development came from the now-infamous “dot chart” of expected interest rate levels. As the chart below shows, the median FOMC participant did NOT revise down his or her expectation for interest rates at end-2016, and only slightly revised down expectations for end-2017 (by 0.2%) and end-2018 (by 0.1%). This is where traders expected to see evidence of the so-called “dovish hike,” but in truth, the dot chart paints a relatively hawkish or aggressive picture for interest rates, with the median Fed member anticipating an interest rate hike at every other meeting next year. Finally, it’s worth noting that the dots “tightened up” over the last three months, reaffirming the increasing consensus within the venerable central bank.

4) The press conference (14:30 ET, 19:30 GMT)

Dr. Yellen’s press conference is still ongoing (though starting to wind down) as we go to press, so we’ll assume that there won’t be any more epiphanies – watch us on twitter for analysis on any late-breaking updates if they occur. So far, she’s mostly toed the party line, noting that the US economy is doing well and good progress has been made on jobs, though the participation rate remains below trend. She went on to state that the committee expects inflation to rise toward the Fed’s 2% target over time and that the pace of policy normalization could change depending on the performance of the labor market and inflation.

5) The market reaction

The market reaction to today’s Fed decision was most satisfying to one “market participant” in particular: the Fed itself. Despite the low liquidity conditions, volatility has been relatively subdued in the wake of the festivities thus far, showing that the Fed’s communication policy was successful in telegraphing the decision.

After an initial drop, US equities are breaking out to new daily highs whereas the US dollar is fading in a classic “buy the rumor, sell the news” dynamic. Both gold and oil have seen a modicum of weakness in the wake of the Fed, with WTI trading off nearly 5%, though that’s more attributable to today’s inventory build than the Fed. The benchmark 10-year US treasury bond yield has ticked back down to essentially unchanged on the day at 2.27% after moving up earlier today.

Once the market finishes digesting the implications of the Fed’s decision and outlook, attention should turn to end-of-month/quarter/year rebalancing, another factor which could weigh on the greenback after this year’s big rally.