Financials enjoy festive cheer but Lloyds spending spree raises eyebrows

Christmas cheer was in abundance in global stock markets on Tuesday, with the Dow Jones hitting another record high, and the Eurostoxx index reaching its […]

Christmas cheer was in abundance in global stock markets on Tuesday, with the Dow Jones hitting another record high, and the Eurostoxx index reaching its […]

Christmas cheer was in abundance in global stock markets on Tuesday, with the Dow Jones hitting another record high, and the Eurostoxx index reaching its highest level so far this year. The market is driven by the promise of Trump – more spending, higher growth, faster wage increases and, most importantly of all for some, a reduction in regulation for the US financial sector. The markets are pricing in for a sweet economic scenario from Trump, they will overshoot, they always do, but for now until year-end more record highs are expected.

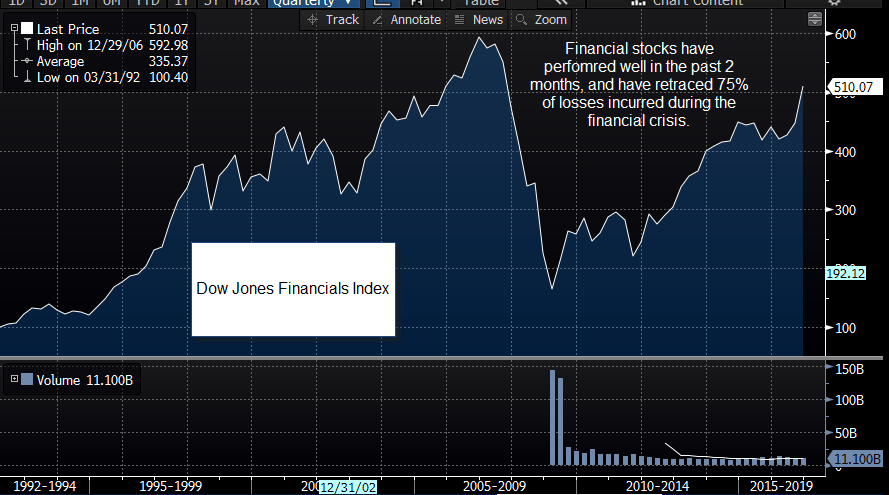

Financials are King of the Hill

The Dow Jones financial index is at its highest level since 2007 (see chart below), and has retraced more than 75% of its losses since the financial crisis. Under Trump, could we see bank shares return to their pre-crisis highs? The prospect of lower regulation under Trump and higher interest rates, which can boost a bank’s profitability, are driving this powerful rally in financial stocks. Investment banks are also benefitting from trading the financial markets as strong trends emerge in currency and bond markets. On Tuesday Jefferies, the US investment banking firm, announced a quadrupling of profit for Q4 on the back of trading revenue. Although not a top-tier investment bank, it is considered a bell-weather for others including Goldman Sachs and Morgan Stanley.

This is also good news for UK and European banks with IB arms including Deutsche Bank, Barclays and Soc Gen, where expectation is rising for a strong performance for Q4. Thus, we could see an extension of the banking rally in today’s session, which may be enough to take the Dow above the psychologically important 20,000 level for the first time. Although financials are likely to remain important for US indices next year, there are some risks to its continued strong performance: Firstly, can the banks deliver a strong set of results for full year in 2017? These will be released in Jan and Feb, and there is a lot of expectation, which increases the risk for a downside shock. Secondly, will the US Congress actually pass any reduction of regulation? This is a concern for Q2 and beyond. If Congress isn’t as de-regulation focused as Trump then banking stocks could be in trouble in the second half of next year.

Defence Stocks: Trump not a one-way bet

Now that the Animal Spirits have been unleashed on the markets, it is worth remembering that Trump isn’t universally good news for the markets. Remember his tweet about Boeing? Trump also wants to slash defence spending, which could be bad news for the 31 key defence contractors used by the government, including Lockheed Martin, which relies on government contracts for nearly 80% of its revenue. It’s share price has fallen this month, however, it’s is only down some 7%, so if Trump needs to balance the budget and boost spending by cutting defence costs, Lockheed Martin could be at risk. Also at risk is Northrop Grumann, which relies on the US government for 83% of its revenues. Thus, in these heady times, it is worth remembering that it may not always be a one way bet when it comes to Trump and share prices.

Lloyds’ ballsy call on the UK consumer

Elsewhere, Lloyds bank saw its share price rise nearly 3% on Tuesday, even though its GBP 2 bn acquisition of credit card company MBNA is a brave call on continued UK consumer strength and has raised some eyebrows. Firstly, some believe that the valuation was too high, secondly, although the consumer credit business has performed well in recent years and bad loan levels are close to record lows, the outlook for consumers is not as rosy going forward as rising inflation and Brexit fears could push up bad debt levels in the UK going forward. Lloyds may have bought at the high, which could also leave the bank on a collision course with its shareholders, as this purchase puts a potential special dividend in Jeopardy. Lloyds share price has risen strongly this month on the wave of optimism boosting the financial sector (see above). However, now that doubts have been raised about the MBNA purchase, we will be looking to see it knocks the shine off of Lloyds’ share price on Wednesday. But at this stage of the stock market rally, any pullback in financial stocks may be small and used as a buying opportunity.

Source: City Index and Bloomberg