Finally a glimmer of hope for crude oil prices

Perhaps the most compelling story in financial markets as of late has been the dramatic and enduring plunge in crude oil prices, as serious oversupply […]

Perhaps the most compelling story in financial markets as of late has been the dramatic and enduring plunge in crude oil prices, as serious oversupply […]

Perhaps the most compelling story in financial markets as of late has been the dramatic and enduring plunge in crude oil prices, as serious oversupply issues and concerns over potentially waning demand have placed tremendous pressure on both the Brent Crude and West Texas Intermediate (WTI) oil benchmarks.

This drop in prices has continued on since mid-2014, when both benchmarks were trading well above the $100 per barrel mark. Worries accelerated as the plummet persevered throughout 2015, bringing prices down to multi-year lows. This has culminated most recently in both Brent and WTI hitting 12-year lows around the $27 level just last week.

Since the latter part of last year, it seemed to have been virtually a hopeless cause for crude oil prices, as major oil-producing nations were reluctant to lose market share by restraining output. Further exacerbating this situation has been a post-sanction Iran that purportedly has plans to implement an aggressive production and export schedule in order to make up for lost time and oil revenue. To make matters even worse, an apparently slowing economy in China, which is the second largest oil consumer after the U.S., prompted concerns over potentially weakening demand for crude oil.

On Thursday, this very pessimistic situation was uplifted by a glimmer of hope. Major oil-producing countries, including Saudi Arabia and Russia, which were previously disinclined to agree upon a cut in production to support prices, have begun to feel enough pressure to at least talk about the possibility of limiting current output levels. According to Russian Energy Minister Alexander Novak, Saudi Arabia has proposed up to a 5% reduction in output by each oil-producing nation. Also proposed was a meeting among oil and energy ministers of both OPEC and non-OPEC nations to discuss the situation.

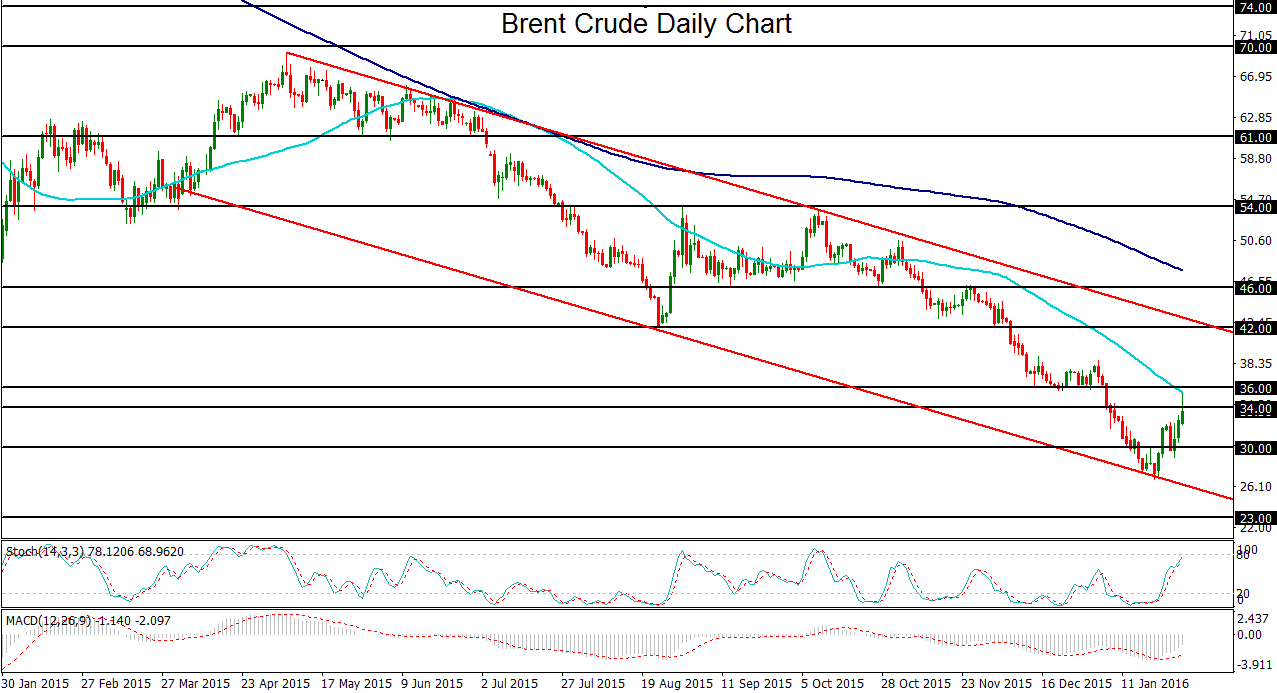

On this news of potential cooperation after so many months of non-cooperation, the initial knee-jerk reaction was swift and substantial. Brent crude surged briefly above $35, establishing a three-week high, before paring those gains as the news settled in. The high that was reached was right at the key 50-day moving average, and closely approached major resistance around the $36 level.

From a longer-term perspective, the Brent crude chart has been forming a large parallel downtrend channel since May of last year. The noted low around $27 last week touched the bottom of this channel before bouncing, which hinted that crude oil had been well oversold and over-extended to the downside, and should have been due for at least a limited relief rally.

Now that this relief rally is occurring, is a possible cooperation among oil-producing nations enough to sustain an actual recovery in oil prices? This will clearly depend on the extent and scope of participation in this potential agreement. A broad-based, substantive agreement that includes most of the largest oil producers would very likely have a substantially positive impact on oil prices.

From a technical perspective, the noted $36 resistance level is the key upside price area to watch. Any sustained breakout above $36 and the nearby 50-day moving average could open the way towards the next major resistance target at $42, followed by the key $46 resistance level.