Fed whistling past the graveyard? Median member still expects 0% interest rates until 2024

As we anticipated in our FOMC meeting preview report, the Federal Reserve did not make any immediate changes to monetary policy at today’s meeting, but that doesn’t mean it was a non-event. Below, we break down all the key developments (and non-developments) from what Bank of America called “one of the most critical events for the Fed in some time”:

Monetary policy statement

The central bank made only minimal changes to its monetary policy statement, noting that economic activity and employment have “turned up recently” though “the sectors most adversely affected by the pandemic remain weak.” The vote to leave policy unchanged was unanimous.

Summary of Economic Projections

This is where it gets more interesting.

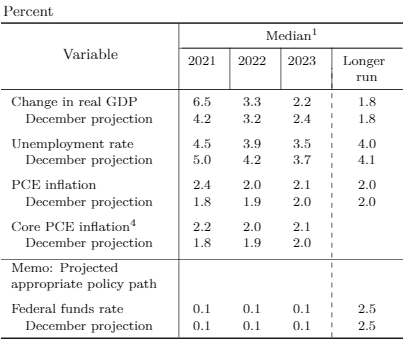

As the table below shows, the central bank meaningfully upgraded its 2021 forecasts for economic growth (from 4.2% to 6.5%) and inflation (from 1.8% to 2.2%) while revising down its end-2021 unemployment forecast (from 5.0% to 4.5%):

Source: Federal Reserve Summary of Economic Projections

While some of these changes merely reflect the central bank “marking to market” its forecasts to acknowledge the strong vaccine rollout and easing lockdowns over the last couple of months, it is noteworthy that these upgrades were NOT “pulled forward” from 2022 or 2023 forecasts. In other words, the Fed has materially upgraded its assessment of the US economy’s potential over the next several years, rather than merely reshuffling improvements from one year to another.

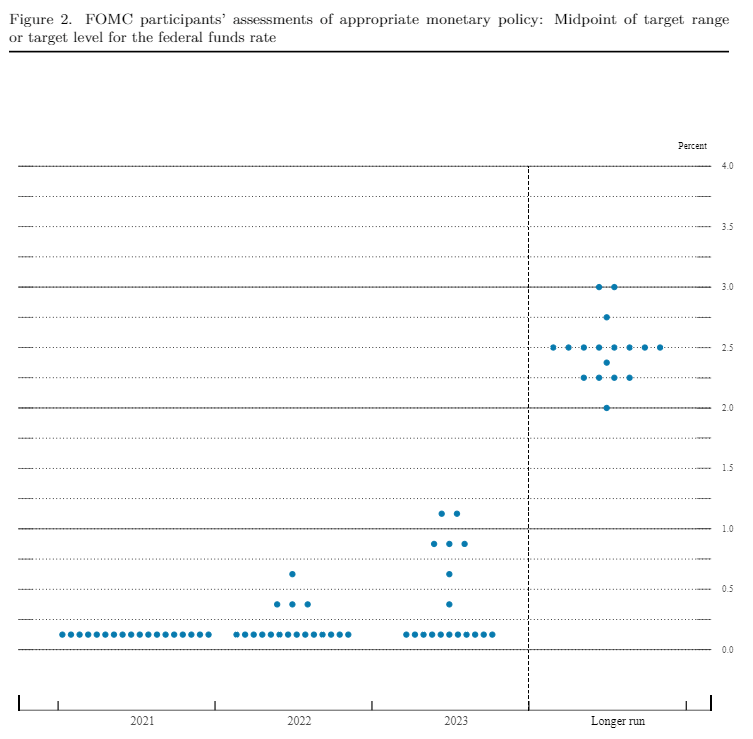

The “dot plot”

As always, the infamous “dot plot” of interest rate expectations was the most important aspect of the release. Though policymakers did start to price in earlier interest rate hikes, the shift was less hawkish than many traders had feared. Per the latest dot plot, only four (of eighteen) policymakers currently see an interest rate increase in 2022, with seven expecting a hike by the end of 2023. Nonetheless, the median Fed member still expects interest rates to remain near 0% until at least 2024!

Source: Federal Reserve Summary of Economic Projections

Press conference

Fed Chairman Jerome Powell is taking the stage to deliver his comments on the decision and the state of the US economy as we go to press. Expect reporters to grill him on the probability that any pick up in inflation will be short-lived and the stark split between market-derived measures of interest rate hikes (more likely than not in 2022) and the Fed’s own forecasts (median member expecting to remain on hold until 2024.

Market reaction

With the world’s most important central bank showing no signs of taking away the proverbial punch bowl of easy money any time soon, the market has seen a clear “risk-on” reaction to today’s release. US indices have caught a bid, though the S&P 500 and the Nasdaq Composite remain barely in negative territory as of writing. Yields are ticking lower across the curve, with the benchmark 10-year Treasury now yielding 1.66%. In FX, the US dollar has dumped a quick 40 pips against most of her major rivals, boosting gold back above $1740.

Moving forward, data on inflation and consumer spending will be critical; if those high-frequency measures of economic activity show signs of heating up, the Fed may be forced to acknowledge that interest rates may have to rise in 2022 (or at least 2023), but as long as price pressures remain tame, “lower for longer” remains the name of the game.

Learn more about forex trading opportunities.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Fed articles

April 22, 2024 04:33 PM

April 10, 2024 01:40 PM

April 4, 2024 02:13 PM

April 3, 2024 07:56 PM