Fed on deck after ECB hits a ground rule double

As everyone expected, the European Central Bank’s monetary policy meeting was the marquee market event of last week, even if the market’s interpretation of its […]

As everyone expected, the European Central Bank’s monetary policy meeting was the marquee market event of last week, even if the market’s interpretation of its […]

As everyone expected, the European Central Bank’s monetary policy meeting was the marquee market event of last week, even if the market’s interpretation of its meaning repeatedly flip-flopped over the last 36 hours of trade. To use a baseball analogy, the ECB meeting was like a ground rule double, where the batter hits the ball deep into the outfield, only to see it hit the ground before bouncing over the fence; the ECB swung with all its might and it initially looked like it had hit a home run for the bears, but later in the session, the market momentum ended up reversing course, leading to a disappointing result (euro strength) for the ECB.

This week, the Federal Reserve will step into the batter’s box and thankfully, a much clearer market outcome is likely. While some optimistic economists are still holding out hope that the US central bank will increase interest rates this week, the market has essentially priced out that possibility. Though no change to monetary policy is likely, the Fed will release its usual monetary policy statement, the always- critical Summary of Economic Projections (SEP), and Fed Chairwoman Janet Yellen will hold her quarterly press conference on the economy.

Given the recent run of decent economic data and improving stock market performance, the Fed is likely to sound much more hawkish this time around. In the monetary policy statement, traders will look for any nods toward the improving economy, specifically on wages and price pressures, which have long been the Fed’s bugaboo, to imply that a June rate hike is more likely. Investors will likewise flip immediately to the notorious “dot chart” in the accompanying SEP to see whether Fed officials have revised down their expectations for interest rates, as well as their numerical expectations for short- and long-run economic growth, unemployment, and inflation. As always, Dr. Yellen’s tone during the press conference will be closely scrutinized, though she’s become much more steady and noncommittal after her initial “couple of months” faux pas a few years ago.

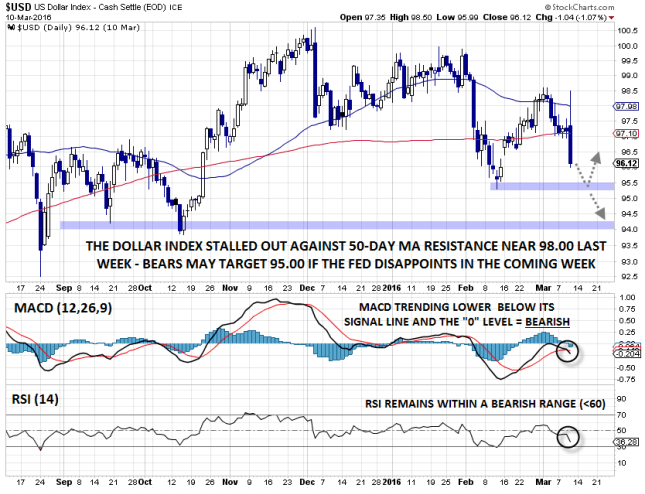

Technical view: Dollar Index

The dollar index, which represents the greenback’s performance against six of its major trading partners, took one on the chin last week. From an extremely basic technical perspective, the index has been in a medium-term downtrend (lower lows and lower highs) since forming a high near 100.00 last December.

February’s bounce appears to have stalled out against resistance near the 50-day MA and the secondary indicators have turned negative as well, with the MACD crossing below its signal line and the RSI enshrined in a bearish range below 60. Especially if the Fed falls short of the markets’ hawkish expectations, bears may start to train their eyes on the 5-month low around 95.00-50 next, with a deeper retracement possible if that level gives way. Only a recovery back above the 50-day MA near 98.00 would shift the near-term bias to the topside for a possible move back toward 100.00.