Fed and BOJ Keep the Central Bank Party Rolling

Last week featured two relatively important central bank meetings, with both the Bank of Canada and the European Central bank coming off as relatively dovish […]

Last week featured two relatively important central bank meetings, with both the Bank of Canada and the European Central bank coming off as relatively dovish […]

Last week featured two relatively important central bank meetings, with both the Bank of Canada and the European Central bank coming off as relatively dovish relative to the market’s expectations. As we look ahead to central bank action in the coming week, the Federal Reserve and Bank of Japan are looking increasingly likely to sing a similar tune.

Focusing in the Federal Reserve’s Wednesday monetary policy meeting first, traders have low expectations of any earth-shattering revelations. Despite Fed Chair Janet Yellen’s protestations to the contrary, the meeting will likely not be “live,” as the Fed prefers to act at its quarterly meetings that feature a press conference and updated economic forecasts (e.g. the upcoming December 15-16 meeting). Indeed, futures traders pricing in only a 6% probability of a rate hike, according to the CME group’s FedWatch tool.

US economic data has been anything but encouraging since the Fed met last month. The headline non-farm payroll report showed a disappointing 142k rise in jobs (as well as flat wage growth month-over-month) and the other top-tier reports have been equally downbeat with both PMI surveys and retail sales also missing expectations this month. Indeed, the only bright spot has been the initial jobless claims figures, which continue to show 40+ year lows in new unemployed Americans, but that will hardly be enough for the Fed to act. Traders will closely scrutinize the Fed’s statement for any changes, but there’s a risk that the lack of substance will lead to a disappointingly small market reaction.

Pivoting to the BOJ, traders are split over whether the bank will look to increase its ongoing quantitative easing program. Policymakers, including Finance Minister Taro Aso, have recently downplayed the likelihood of a larger QE program, but we still believe such an action remains on the table. In the past, the BOJ has argued that “surprise” is a critical element of effective monetary policy and from that perspective, Aso’s comments could be seen as an intentional attempt to eliminate speculation about further easing, therefore increasing its impact if the bank does opt to expand QE.

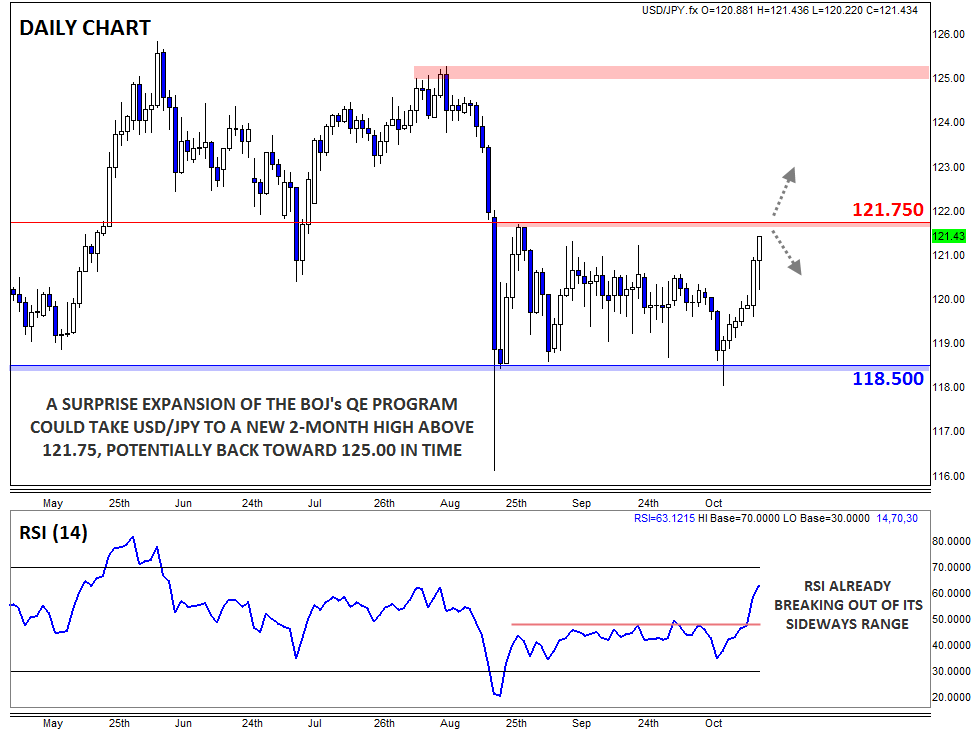

Recent economic figures present a compelling case for more easing from the BOJ. Industrial Production fell to a two-year low in August, and it looks likely that the Japanese economy contracted in Q3, meaning that it is in a technical recession (two consecutive quarters of falling GDP). Meanwhile, the yen has actually strengthened over the last four months, with USD/JPY falling from above 125.00 down to a low near 118.00 last week (rates have since bounced back to 120 as of writing).

If the BOJ does surprise traders by expanding QE, USD/JPY could surge to a new 2-month high above 1.2200 and potentially retest its multi-year low around 125.00 in time. That said, if the central bank opts to keep its powder dry once again, we could see a move back toward the bottom of the recent range around 118.50.