Eyes on Apple shares after mega earnings

Never bet against Apple’s ability to beat expectations. That might not be a truism worthy of an investing ‘sage’. But on balance, it’s probably proved […]

Never bet against Apple’s ability to beat expectations. That might not be a truism worthy of an investing ‘sage’. But on balance, it’s probably proved […]

That might not be a truism worthy of an investing ‘sage’.

But on balance, it’s probably proved correct more often than not.

By one means or another, Apple posted fourth-quarter results overnight that knocked the ball out of the park.

Wall Street was expecting earnings per share between $1.28 and $1.31.

The result was a ‘clear beat’, to use Wall Street parlance, with EPS at $1.42, compared to $1.18 in the same quarter a year ago.

Net income was $8.47bn for the quarter ending on 27th September. Net income was $7.51bn in the corresponding quarter a year ago.

Just as important as the earnings, Apple’s iPhone sales were a major watch-point.

Apple sold 39.27 million iPhones in Q4, compared with 33.79 million sold at the same time last year.

iPhone sales were above the widely expected level of 37 million–plus.

My view before the results was that Apple needed a stronger beat on handset sales to impress the market—closer to 40m,

Still, it would be tardy not to recognize the acceleration of iPhone sales in Q4 as a major achievement.

Despite the huge iPhone shipments though, the first major and material surprise in the earnings report was Apple saying it already resumed its share buyback, following recent ‘encouragement’ from activist investor Carl Icahn.

The twist was that Apple said it began re-purchasing stock before Icahn sent one of his infamous open letters to Apple CEO, Tim Cook, on 9th October.

Apple said it bought back $17 billion worth of stock during the September quarter.

This brings Apple cash payouts to shareholders, including dividends to $45bn this year.

In a statement on Monday evening, Tim Cook said: “We saw an opportunity to be very aggressive in the market and really put our foot on the gas for our stock buyback.”

The open-ended, retrospective nature of Apple’s comments on the share re-purchase, plus the all but oblique reference to the obvious catalyst for the buyback–pressure from Icahn, strongly suggest share re-purchases will continue in the medium term.

However, Apple is also signalling it may continue to conduct share buybacks under its own volition and on its own terms (at least it would like to give the impression of buybacks on its own terms) and it may continue to only disclose the share re-purchases after the fact.

Apple’s cash pile as of the end of September was around $165bn.

Even if we assume it did not add to its free cash flow during the last quarter (we know it did) Apple could still comfortably absorb at least 5 more buybacks of similar size to the one just conducted.

It’s quite likely the share buyback news will please investors more than any other element of the earnings report.

It’s also worth noting Apple did not make much attempt to dampen concern about the potential impact of the historical dollar advance during the last several weeks, although the dollar has since paused.

Whilst Apple said its current guidance accounts for likely impact of the strong dollar, it was careful not to suggest a resumption of the greenback’s rise was already factored in.

In other words, a continuing dollar rise, could introduce a new element of uncertainty about Apple’s revenues going forward, even if just a moderate one.

Whilst Apple explicitly mentioned ‘hedging’ (a means of offsetting negative currency effects) there is a possibility that Apple’s net income margin could see erosion in case of a further sizeable dollar advance.

News that Apple resumed buying back shares certainly seems to be the main reason for its stock’s 1.5% rise in ‘after hours’ trading, taking the shares above the psychological $100 marker, to $101.12.

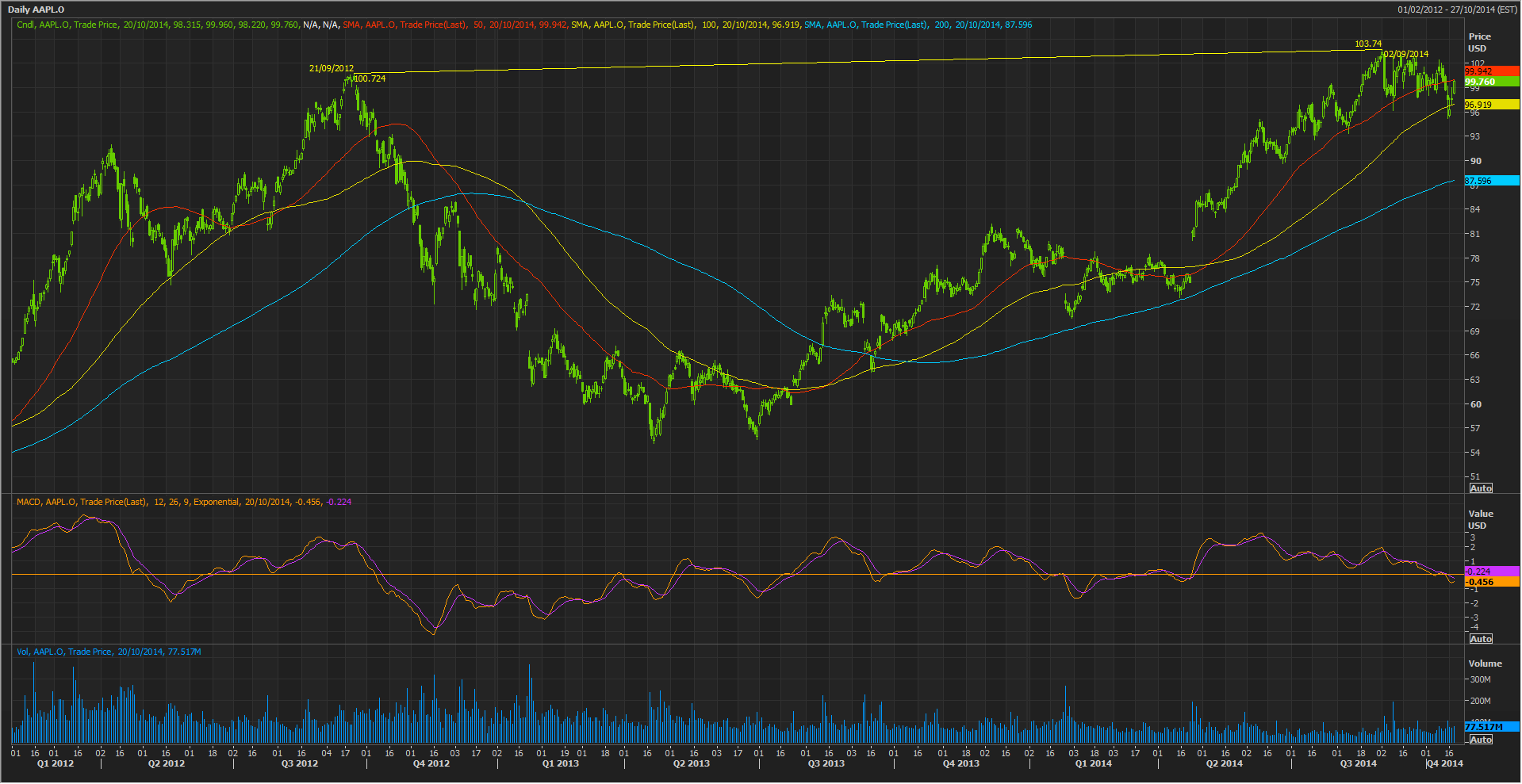

The $100 level has capped the stock for months (or years, if we adjust for June’s stock split, as per the chart below).

The stock even failed to breach the level after Apple’s blow-out new product events in September.

Will yesterday’s earnings be strong enough for Apple shares to close above $100 per share?

(A stock’s closing price is generally regarded as more sustainable than an intraday trading price.)

That’s obviously a difficult question to answer.

Plus, the answer also depends on a number of key operational points for Apple, some of which are outlined below.

An even more important barrier is what we can call ‘The Apple Premium’.

This is a psychological dimension which Apple itself no doubt played a large part in creating.

Basically, investors have been conditioned to always expect Apple to beat its own forecasts.

In some ways, of course, working hard to create a reputation for such excellence is a noble goal for any company to pursue.

The major problem with it is that investor expectations of a firm’s capabilities can be constantly recalibrating higher.

Under those circumstances, even unequivocally solid results like Apple Inc. posted last night, may reap only a moderate-to-lacklustre response from investors.

I think Apple shares may reflect this dynamic today.

The shares could trend up towards the $100 level.

But the mild test of $101.27 after hours seems to argue against the stock holding above the psychological marker.

Again, more disclosure and assurances of further share buybacks are what the market may require to see the stock as worth more than $100 sustainably.