EURUSD View Post ECB

ECB press conferences are growing in explicit and forward nature as the ECB president is pressured to rein in rising bond yields and contain shrinking […]

ECB press conferences are growing in explicit and forward nature as the ECB president is pressured to rein in rising bond yields and contain shrinking […]

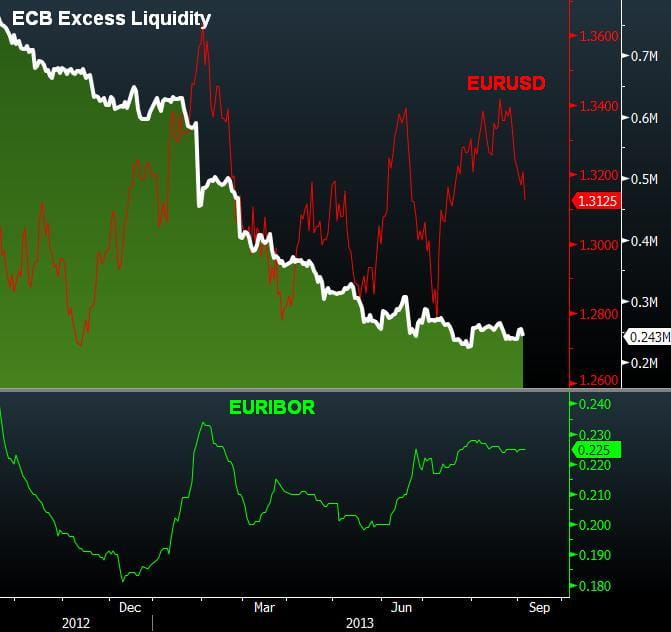

ECB press conferences are growing in explicit and forward nature as the ECB president is pressured to rein in rising bond yields and contain shrinking liquidity. Facing a notable data improvement in the Eurozone and a 60% decline in ECB excess liquidity, ECB president Draghi reiterated the importance of maintaining a downward bias on rates and reiterating that discussion on interest rate cuts was ongoing.

The ECB couldn’t avoid upgrading its 2013 GDP forecast to -0.4% from the initial -0.6% but lowered its 2014 GDP forecast marginally to 1.0% from 1.1%. The ECB also upgraded its CPI forecast to 1.5% from 1.4%, while keeping its 2014 CPI view unchanged at 1.3%.

At a time when the Fed is set to taper its $85 bn, the Bank of England is approaching the unavoidable point of having to scale down its £375 bn in monthly asset purchases, the ECB will have to decide whether to limit such tightening via slashing rates below zero or via another dosage of liquidity injection.

Chatter of a 3rd LTRO with a 5-year maturity is doing the rounds as the ECB must act on rates now that the likelihood for any nation to opt for the Outright Monetary Transactions has become minimal. Any immediate impact from escalating talk of LTRO-3 should be a negative for EURUSD from a relative policy stance, but if the operation is seen as part of a coordinated global easing (as in autumn 2012), then it would be deemed EUR-positive. Finally, the ECB has an easier task of talking down rates than is the Bank of England due to the resumption in falling Eurozone inflation, reaching 1.3% y/y.

EURUSD posts its 2nd weekly decline after a prominent failure to break above its 200-week moving average led to a descent near the 55-WMA—coinciding with 1.3100. Since the start of the euro, there has been 4 failed attempts to break above the 200-WMAs, which were followed by declines towards the 55 and 100 WMAs; Oct 1998, Oct 2010, Oct 2011, Feb 2013 and Aug 2013. A pullback towards the 100-WMA implies a decline to 1.3045.

Aside from the Fed’s anticipated taper announcement (-$10 bn from MBS), we must watch the growing reports indicating that President Obama will appoint former treasury secretary Lawrence Summers to become new chairman of the Federal Reserve next year, This is seen generally as a positive for the US dollar as Summers is seen against prolonging quantitative easing, a stance strongly supported by his opposing candidate Fed vice chairwoman Janet Yellen.