EURUSD respite for Thanksgiving but parity still beckons

The single currency may be retracing some of Wednesday’s losses as the US celebrates Thanksgiving, but the bounce looks fairly tepid, even after the strongest […]

The single currency may be retracing some of Wednesday’s losses as the US celebrates Thanksgiving, but the bounce looks fairly tepid, even after the strongest […]

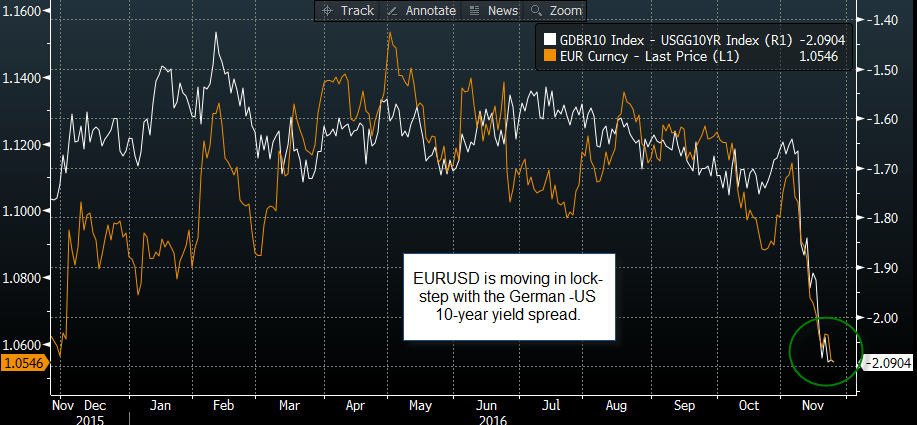

The single currency may be retracing some of Wednesday’s losses as the US celebrates Thanksgiving, but the bounce looks fairly tepid, even after the strongest German business confidence for 2 years. This suggests to us that the euro is still at the mercy of the German – US bond yields spread, which remains at its lowest level since the late 1980s.

Borrowing is back in fashion for FX

The euro appears to be suffering from the continued focus on austerity and reigning in debt levels across the currency bloc. This policy is now in stark contrast with the fiscal largesse in the US and the UK, which is a key driver of higher Treasury and Gilt yields. As the spread between German 10-year and US 10-year yields has fallen to more than -2%, the euro has dropped in lock-step. To put this into some context: the correlation between the euro and German 10-year bond yields has surged to nearly 80% in recent days.

But don’t rely on the yield spread in isolation when it comes to EUR. Over the long term the correlation between EUR/USD and the yield spread is not significant, which suggests that this period could be short lived. Also, the German –US yield spread is already at a multi-decade low, which makes us nervous about how much further it has to fall, especially since the Fed Fund Futures market is now pricing in a 100% expectation of a Fed rate hike next month.

Trump could be the biggest obstacle for EURUSD parity

The bond market and currency market appear to be taking Trump’s spending plans as fact, even though he isn’t even President yet. While we fully expect the President-elect to propose a large fiscal stimulus plan early next year, we don’t know if a Republican Congress, some of whom have been reluctant to support infrastructure plans in the past, will agree to a large increase in US government borrowing. Thus, if Trump’s plans have to be watered down at any stage, then expect a major readjustment in financial markets, especially the bond market, and a large decline in the USD.

We won’t know this until 2017, for now the market seems happy to ditch the euro in favour of higher yielding currencies like the USD and GBP. If you want to see whether EURUSD will reach parity, then watch the German – US yield spread (see chart 1). If it starts to recover then it could drag EURUSD up with it.

Figure 1:

Source: Bloomberg and City Index.

Technical view:

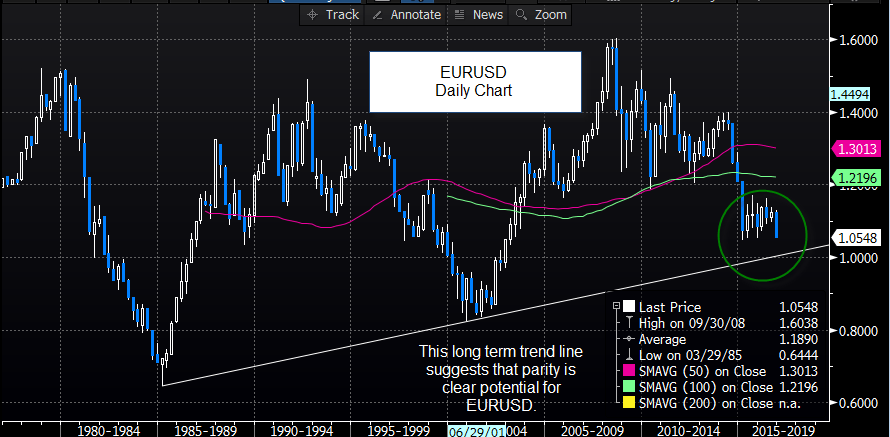

The technical picture is bleak for EUR. Figure 2 shows a long term trend line on EURUSD, with the next key support level at parity, and the yield spread at a multi-decade low, the prospect of parity in EURUSD is very real right now.

Figure 2:

Source: Bloomberg and City Index