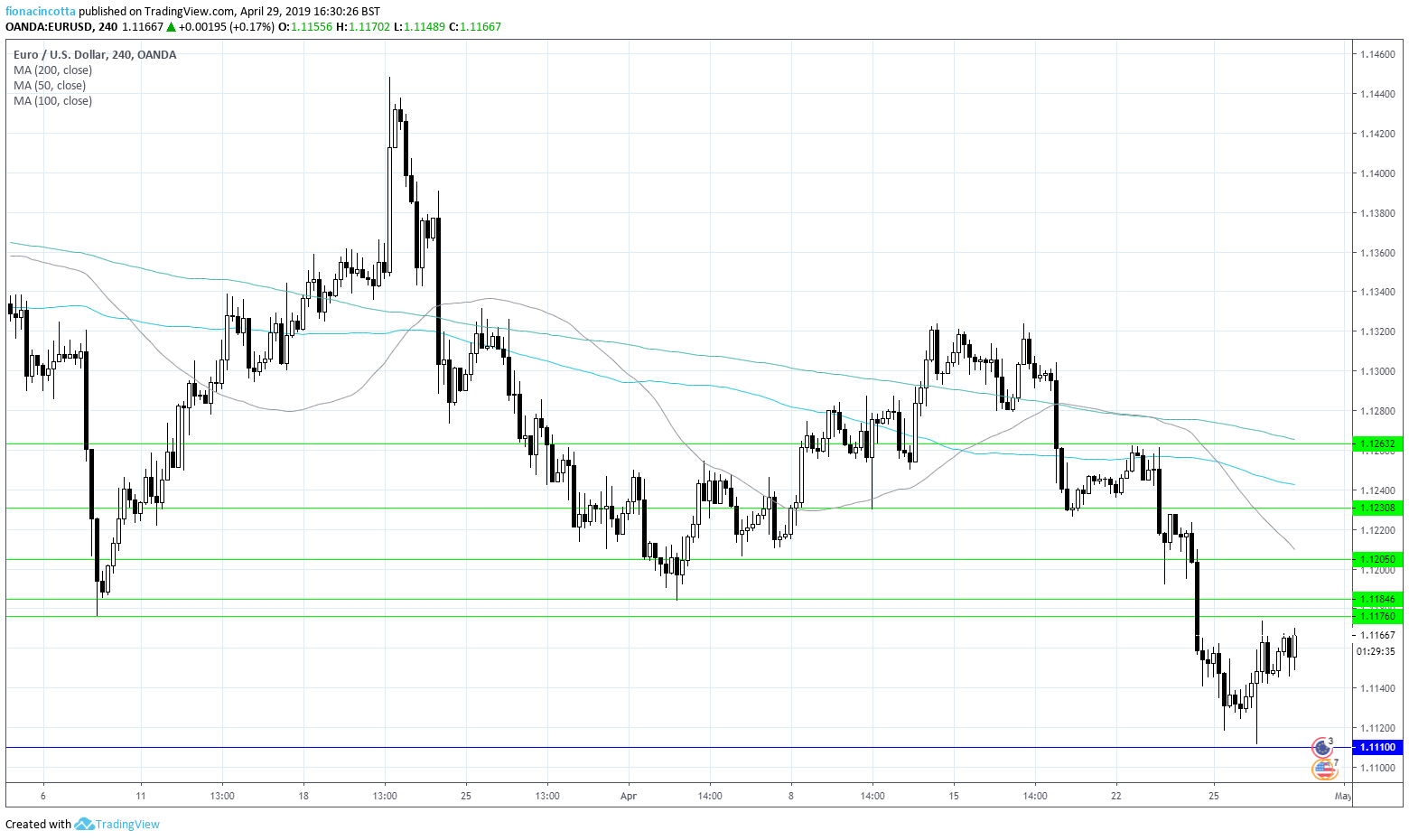

Euro data points to continued weakness

Eurozone confidence data came in mostly weaker than forecast with economic sentiment at the lowest level since 2016, showing that the bloc’s economy is still bogged down.

Eurozone confidence data came in mostly weaker than forecast with economic sentiment at the lowest level since 2016, showing that the bloc’s economy is still bogged down.

The euro will remain in focus as investors look ahead to a barrage of data due be released from the bloc tomorrow. Expectations are for 1.1% growth yoy and 0.3% growth qoq, up from 0.2% amid fewer global headwinds and upbeat services activity. However, these figures could be overly optimistic given that the German manufacturing pmi was down at 44.1.

A strong GDP reading could see the EUR/USD climb back towards $1.12. A miss could see the euro retest year to date lows.

Dollar dips post PCE reading

The dollar put its recent rally on hold following US inflation data. PCE, the Fed’s preferred measure of inflation showed that prices declined to 1.6% in April, down from a downwardly revised 1.7% in March and below the 1.7% forecast. The data comes following Friday’s mixed GDP data. A GDP release that saw the headline figure demonstrating impressive growth of 3.2%. However, this was driven principally by a large accumulation of unsold merchandise, as the inventory component of the report was high and consumer spending noticeably weak.

Weak inflation and “the not quite as impressive as the headline figures suggest” GDP report are unlikely to encourage the Fed to take their finger off the pause button, even though other data across the month, such as retail sales, home sales and manufacturing have all seen improvements. According the CME Fed funds, the market is still pricing in a 65% probability of a rate cut before the end of the year. This is keeping the dollar under pressure ahead of the US Federal Reserve rate announcement on Wednesday.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM