Asian Indices:

- Australia's ASX 200 index fell by -37.7 points (-0.56%) to close at 6,708.20

- Japan's Nikkei 225 index has fallen by -433.47 points (-1.43%) and currently trades at 297,832.28

- Hong Kong's Hang Seng index has fallen by -548.08 points (-1.86%) and currently trades at 28,857.64

UK and Europe:

- UK's FTSE 100 futures are currently down -54.5 points (-0.8%), the cash market is currently estimated to open at 6,725.18

- Euro STOXX 50 futures are currently down -31 points (-0.8%), the cash market is currently estimated to open at 3,836.54

- Germany's DAX futures are currently down -104 points (-0.7%), the cash market is currently estimated to open at 14,671.52

Thursday US Close:

- The Dow Jones Industrial fell -153.07 points (-0.46%) to close at 32,825.95

- The S&P 500 index fell -58.66 points (-1.48%) to close at 3,915.46

- The Nasdaq 100 index fell -413.23 points (-3.13%) to close at 12,789.14

Indices in the red overnight

Equity markets in China and Hong Kong led the way lower in Asia overnight, falling -2.6% and -1.9% respectively. The ASX 200 was also -0.5% lower but pared earlier losses later in the session. Futures markets across Europe are also following this trend, as investors brace themselves for the potential of that higher yields will again weigh on equities.

The FTE 100 held above its 10-day eMA yesterday and produced a small bullish hammer on the daily chart. Today’s bias remains bullish above 6,740 (yesterday’s low and 10-day eMA) and the next major resistance level is the 6800/13 zone. Intraday support sits at 6762 and 6773.

Learn how to trade indices

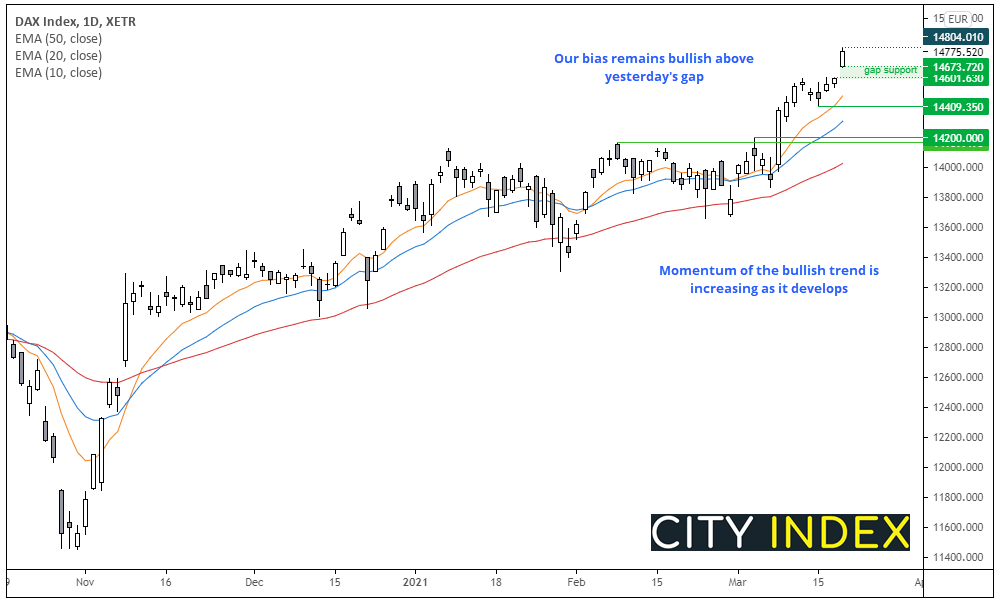

The DAX to mind the gap?

The DAX enjoyed a close to a fresh record high yesterday after gapping higher and closing above 14,700. However, early futures pricing suggests it could open near yesterday’s low and try and close that gap.

The daily chart clearly remains within a strong bullish trend. And whilst some measures could suggest it may be ‘overbought’ we feel inclined to ignore such signals until price action confirms. We should get an indication of what sort of day it faces after the open, because if it trades directly higher then we’d have more confidence yesterday’s gap remains unchallenged. Yet, if price action is choppy or moves swiftly lower, we will be waiting to see if yesterday’s gap holds as resistance.

- A break above yesterday’s high assumes the trend is continuing to pick up speed. Bulls could use an open upside target if trading from the daily chart.

- If prices move lower, bulls could wait to see if yesterday’s gap holds as support for a potential swing trade long.

- A break beneath 114,600 assumes a counter-trend move is underway.

US and China spar in first high-level talks

Well, verbally at least. The first talks between China and the US under Biden’s new administration got off to a tough and confrontational start. With US accusing China of “grandstanding” and listing problems with China ranging from cyberattacks to threats against Taiwan, China responded with a 15-minute prepared speech and labelled the US a “struggling democracy” whilst criticising its trade policies.

What this means for trade relations (or any kind of relation, for that matter), time will only tell. But anyone who expected smooth sailing now Trump is out of the Whitehouse may be left disappointed.

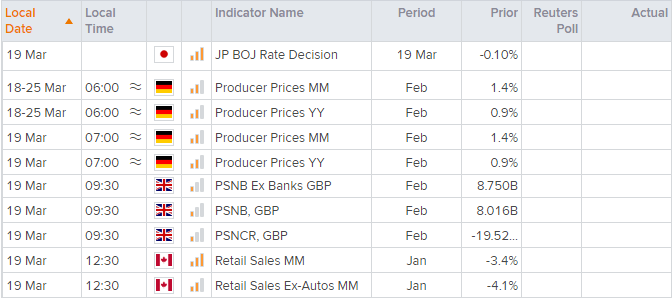

Little room for any surprise from today’s BOJ meeting

The Bank of Japan held interest rates at -0.1% and widened the band used to allow JGB’s (Japanese Government Bonds) to move around their target to +/- 0.25% from +/- 0.2% previously. They also revised their asset purchase programme to only purchase ETF’s when absolutely necessary. This is all well and good yet came as no surprise to traders who read reports over the past two days. There was little reaction from traders in Tokyo as they seemingly already knew what to expect.

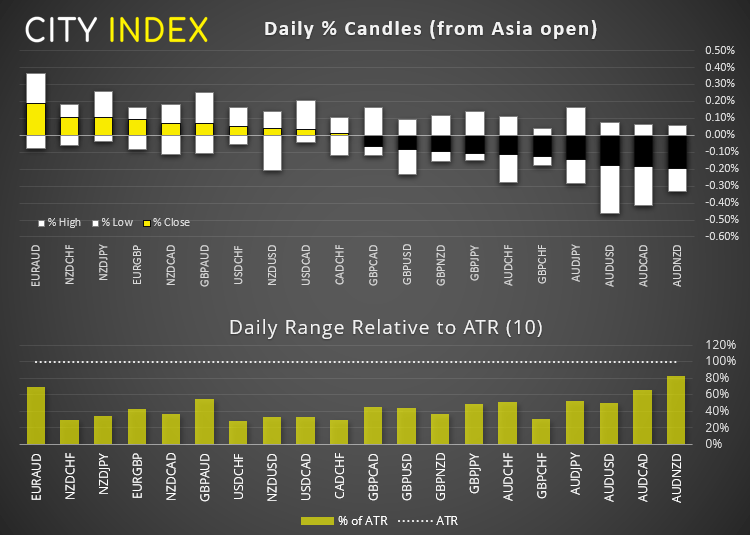

Forex markets have had their nap, now it’s time to wake-up

The US dollar index trades near yesterday’s bullish engulfing high but capped by 92.03 resistance. A break above it brings the 92.50 high into focus.

It was smalls ranges overnight but, for what its worth, NZD is the strongest major and AUD is the weakest. AUD/NZD remains within the supply zone around 1.0800 after earlier showing the potential to break above 1.0843 resistance. If we see yields higher and stocks lower today then we suspect AUD/NZD may finally break higher.

- GBP/USD rolled over again from 1.4000 yesterday following the BOE meeting and a strong US dollar. But whilst it is down it is not necessarily out. Given the bullish trend on the daily chart and respect of the 50-day eMA, we will continue to monitor its potential to break that 1.4000 barrier.

- GBP/CAD closed at a four-day high, although remains beneath the 10-day eMA and the bearish trendline projected from the February high. Assuming they continue to hold as resistance, we may find bearish interest return around yesterday’s highs for swing trade shorts.

- EUR/GBP produced a bearish engulfing candle yesterday. There was a minor attempt at breaking to new lows, but that it was a bearish close just above key support suggests bears may attempt t break lower one again. A break beneath yesterday’s low assumes bearish continuation.

Learn how to trade Forex

Commodities: Gold to turn lower?

Gold is -0.3% lower after forming a bearish outside candle below 1760 resistance. Our near-term bias is for another dip lower towards 1700.

Palladium trades around 2655 after two strong closes above its multi-month breakout level. We will wait for a retracement or period of consolidation before considering a new bullish bias.

WTI has gained 0.43% in overnight trade and holds above 59.24 support, but has done little to ease the pain of yesterday’s -7% sell-off. We expect 59.24 to be a pivotal level today and possibly next week.

Up Next (Times in GMT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- It’s a relatively quiet end to a busy week in today’s calendar.

- German producer prices are up at 06:00. With yesterday’s stronger ZEW report citing rising inflation expectations, then it would be constructive to see it start in producer prices today, and potential further support an already stronger euro in a weaker dollar environment.

- Canadian retail sales are the main event int the US session. Whilst they’re expected to contract they are also expected to do so at a slower rate of -3.0% MoM (versus -3.4% prior) and -2.8% YoY (versus -4.1% YoY).

Latest market news

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM