European stocks in wait and see mode ahead of ECB

European stocks are trading mixed today. The UK’s FTSE is higher, boosted by relief that all seven UK lenders have passed the Bank of England’s […]

European stocks are trading mixed today. The UK’s FTSE is higher, boosted by relief that all seven UK lenders have passed the Bank of England’s […]

European stocks are trading mixed today. The UK’s FTSE is higher, boosted by relief that all seven UK lenders have passed the Bank of England’s latest stress tests. But the markets in the Eurozone are held back slightly, in part due to profit-taking ahead of the ECB meeting on Thursday. The stronger economic numbers from the single currency bloc, which have helped to underpin the euro, have also undermined some export-oriented stocks. As well as the slightly stronger November manufacturing PMIs from Spain, Italy and Germany, the latter also saw its unemployment total fall more than expected in October, by 13,000 compared to 4,000 expected. In addition, the Eurozone unemployment rate unexpectedly fell to 10.7% in October from 10.8% previously. Though today’s US economic numbers are unlikely to cause any major shockwaves, the employment component of the ISM manufacturing PMI, which can be among the leading indicators for Friday’s monthly employment report, could cause a bit of volatility in the markets. Lots of Federal Reserve members are also scheduled to speak this week, starting with Charles Evans this evening. Their comments may provide further hints about the upcoming US monetary policy decision.

So far, US investors don’t seem to be too bothered about a rate rise there, partly because the Fed has been so good at preparing the market for a lift off. But November was a sluggish month for US stocks where the major indices ended the month pretty much flat despite volatile intra-month swings. In contrast, the major European indices rose for a second straight month, suggesting investors are growing more bullish on European market and less so in the US. This is most likely due to the growing disparity between actual and expected interest rates in the two regions. If the ECB decides to further cement its zero interest rate policy on Thursday by expanding QE in some way, shape, or form then the outperformance of European stocks should gather pace, especially if Friday’s US jobs data increases the odds of a Fed lift off later on this month.

But the scope for disappointment is there now and if the ECB fails to deliver what the markets demand then we could see a sharp drop in European stocks. A cut in interest rates without altering QE is a scenario which is unlikely to be enough to satisfy the bulls either.

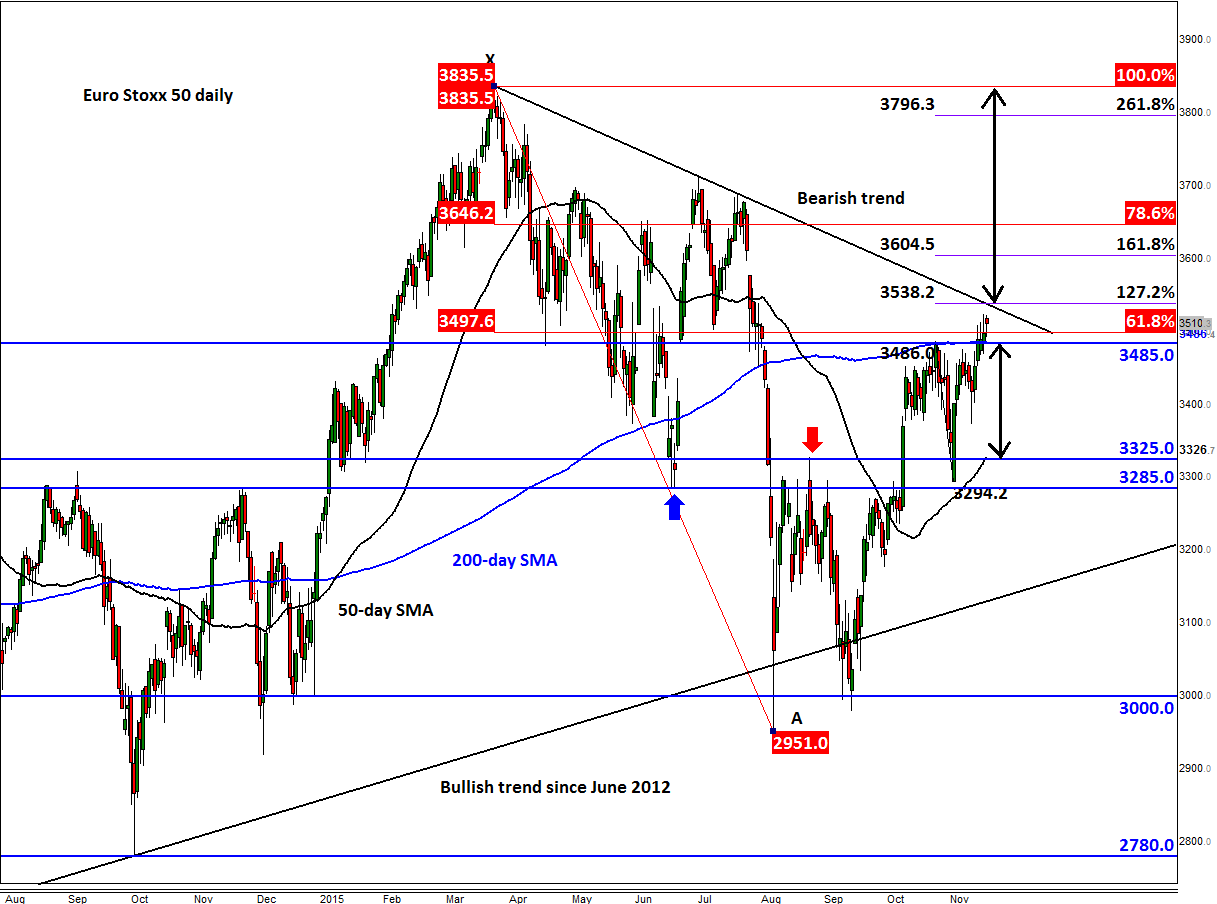

Ahead of the ECB decision, the major European indices look bullish pretty much across the board, if a little overbought. The Euro Stoxx 50, for example, has broken above old resistance and the 200-day moving average at 3485 already and the index was trading above this level at the time of this writing. For as long as it remains above here on a closing basis, the path of least resistance would remain to the upside. That being said, it is yet to break its bearish trend line in order to confirm the breakout. This comes in around the 127.2% Fibonacci extension level of the most recent downswing at just shy of 3540. Above here, there is little further resistance apart from the Fibonacci levels shown on the chart. So, potentially, a break above the trend could open the way for another visit of the multi-year high of 3835 that was achieved in April.

If, however, the Euro Stoxx 50 falls back below the key 3485 support and hold there for a few days then it could head back lower towards old supports at 3325 or 3285 before deciding on its next move. For the index to get there, it would probably require the ECB to disappoint on Thursday.

.