European stocks extend drop after China s Black Monday

It is Black Monday today and not just in the financial markets, but the gloomy weather here in London makes for an even more depressing […]

It is Black Monday today and not just in the financial markets, but the gloomy weather here in London makes for an even more depressing […]

It is Black Monday today and not just in the financial markets, but the gloomy weather here in London makes for an even more depressing mood. Stocks have been hammered once again in overnight trading in Asia after the Chinese authorities and other central banks have disappointed those who were hoping for some sort of intervention over the weekend to help support the markets following last week’s big sell-off. At midday, the major European indices are showing losses of about 2.5 to 3.5 per cent and US index futures point to a sharply lower open on Wall Street. As well as mounting concerns over the health of the Chinese economy, the collapsing commodity prices – in particular crude oil, which hit a fresh 6.5 year low today – are helping to fuel rising deflationary expectations. The lack of further significant ammunition from the major central banks is also a concern as after all interest rates are at zero and QE is at full throttle in the case of the ECB. Thus, there is a risk that stocks could fall a lot further from these levels before a bottom is found.

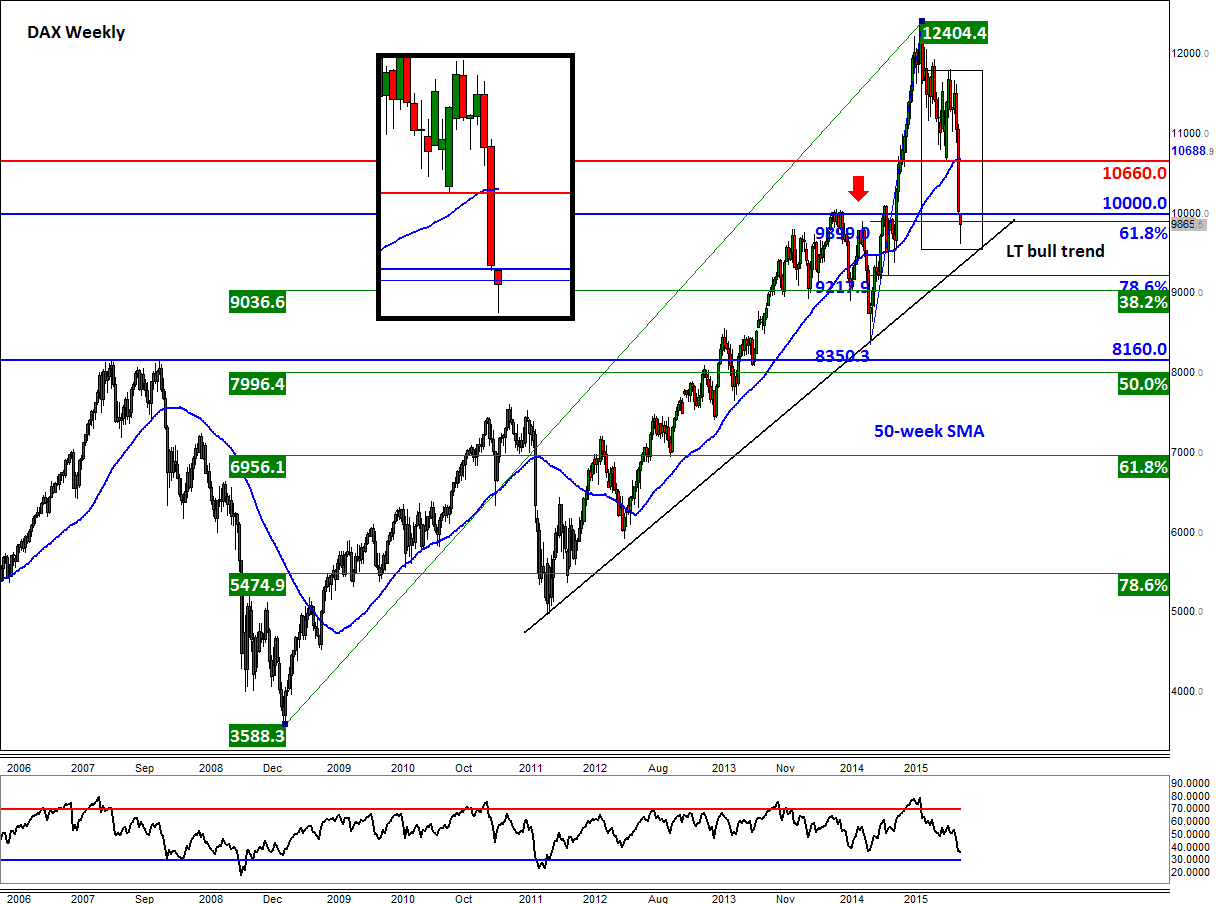

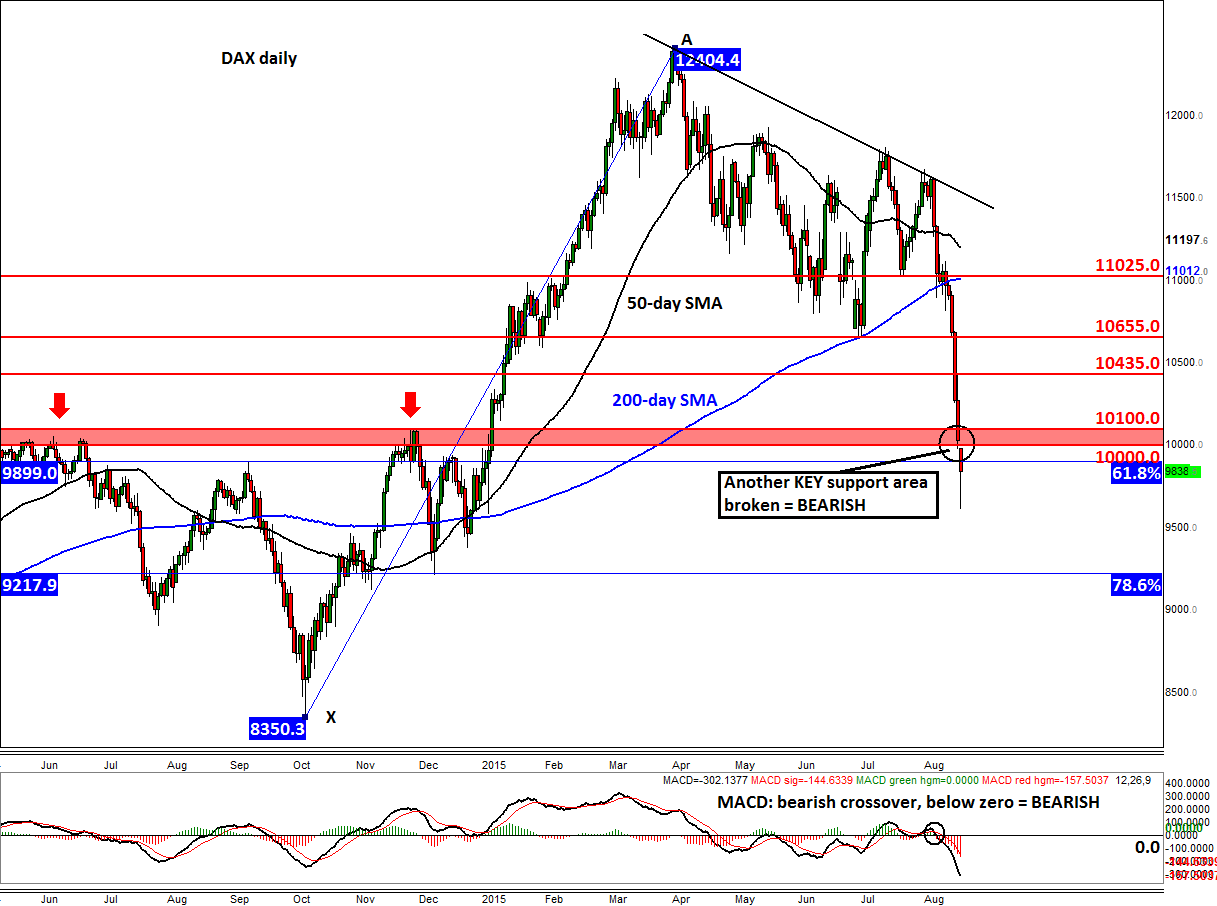

It has been a long time since I last looked at the weekly chart of the German DAX index, but following this recent turmoil, we do need to look at the long term technical levels in order to find potential turning points. One key potential turning point was the area around the 10,000 handle. The rationale for expecting a bounce around this psychologically important level was that this was previously a strong resistance area throughout 2014, so this year it could have turned into support. There was also the 61.8% Fibonacci level of the upswing from the last significant low hit in October converging there. But no such bounce has been realised here, which is obviously another disappointment for the bullish investors and so even less of a reason to try and “buy the dip” for the time being.

That being said, the closing levels will be more important, as the break below 10,000 could just be a false one. Indeed, if the DAX does manage to recover and end today’s session higher – preferably above 10,000 – then we may see a potential rally over the coming days. As a result, the index could recover all the way to the previous support around 10660 before potentially turning lower once more.

But the odds are stacked against the bulls for now and there may be further momentum left in this sell-off. As such, the DAX may be unable to stage a short-covering bounce at all today and instead drop towards its long-term bullish trend around 9300 before deciding on its next move. Beyond the trend line, the next potential support could be around the next psychological hurdle of 9,000 which also corresponds with the 38.2% Fibonacci retracement of the upswing from the post financial crisis low. We certainly wouldn’t be surprised if we got there at some stage this week.