European shares show more pragmatism than panic for now

Updated 1620 BST (Adds main points on trading in UK 100) Trading in European markets a day after Greece voted against ‘cash for austerity’, shows […]

Updated 1620 BST (Adds main points on trading in UK 100) Trading in European markets a day after Greece voted against ‘cash for austerity’, shows […]

Updated 1620 BST

(Adds main points on trading in UK 100)

Trading in European markets a day after Greece voted against ‘cash for austerity’, shows more pragmatism than panic.

In Germany, Greece’s largest and most influential creditor, the benchmark DAX30 stock index commenced around 1.5% lower and still showed a similar loss in the late afternoon.

FTSE Eurofirst 300, the Europe-wide list of the bloc’s largest firms, was also similarly undented, trading little more than 1% lower, despite more than 61% of Greeks voting “no” in Sunday’s referendum.

The UK’s FTSE 100 benchmark lost 1% earlier, but had pared that loss back to a 0.7% fall.

That’s despite a nosedive by shares of aerospace and defence blue-chip Rolls Royce Holdings Plc., after the firm announced its third profits warning in the space of nine months and its relatively new CEO said he would stop a share buyback programme announced by his predecessor last year.

Amid market mutterings about potential action ‘in concert’ by central banks, aside from Switzerland’s, the sole monetary authority that last week openly acknowledged it was intervening, trading of the single currency was also eerily calm.

The euro slipped a relatively contained 0.6% to $1.10390 at the time of writing, but maintained its grip on the psychological $1.10 handle having dipped below it during early morning-trade.

Greece’s membership of the currency union might well be in greater question than it was on Friday evening, but for whatever reason, there is no extreme market volatility in the wake of this fact.

Trading in EUR/USD options, one of the more liquid ‘implied volatility’ markets was almost exclusively cheaper across ‘the curve’, as premiums fell.

Make no mistake there is anxiety in European financial markets, a ludicrously obvious statement perhaps, but one which bears repeating amid placid European trading.

The STOXX 600, an even larger regional equity gauge, was down a measured 1.2%, despite calls last week, by global investment banks for falls as deep as 10% in the region’s major stock indices.

But there remains a backlog of flotations and takeovers and other capital activities across Europe and beyond.

One known example was a bond deal worth up to $1bn, enabling Kurdistan to make its international capital markets debut.

It had been due to launch today, but was reportedly delayed until further notice.

There were also some concerns in The City that some delayed deals might be scrapped entirely.

In wider-European M&A, data provider Dealogic said last month that Europe’s share of the global total was just 25% at the half-way point of the year, the lowest proportion since 1998.

If nothing else, Monday’s calm demonstrated that the market had been reassured by measures taken by monetary authorities since the beginning of Europe’s sovereign debt crisis in 2010.

The European Central Bank’s bond-buying program, launched in March this year, represents the most visible part of the programme to buttress Europe against a ‘catastrophe’ from its periphery.

The official action of the central bank might also have been evident in the one area where the weekend’s historic schism was represented—‘peripheral’ Eurozone bonds.

Greece’s highly-sensitive two-year yield—climbed nearly 15 percentage points to 35% on Monday.

But whilst yields in Italy, Spain and Portugal followed suit, they were nowhere near what had been regarded as ‘red alert’ levels seen in 2012.

The spell of uncertainty (or perhaps ‘unreality’) over Europe’s markets might well lift as the week progresses, amid a swirl of rumours, on top of those about intervention.

It was obviously difficult to corroborate talk that the world’s largest investors like global banks and wealth funds were standing aside from trade on Monday.

But trading volumes were sharply lower, with 104 billion FTSE Eurofirst 300 deals seen by just after 2pm in the afternoon compared with a 90-day average that was almost double that at 202 billion trades.

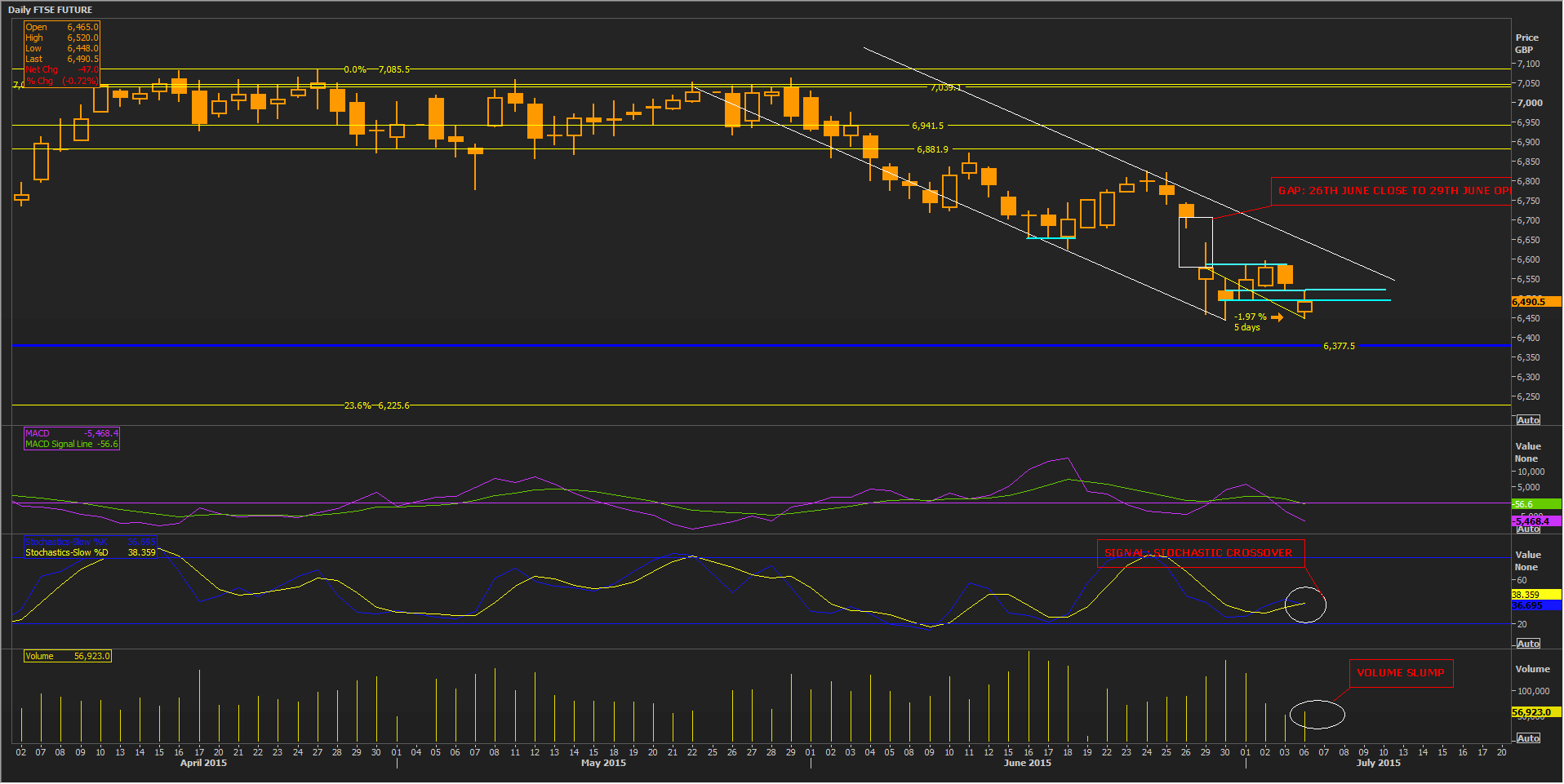

Activity in Intercontinental Exchange’s FTSE 100 Futures, one of the most liquid derivatives of the underlying FTSE 100 gauge, was also visibly subdued.

By online time, the contract had retreated about 9% from all-time contract highs between 7046 and 7085 in mid-April, closing the distance to mid-January lows at 6377.

Below there, a relatively weak 23% retracement of the advance to the contract record was all that protected the asset from deeper lows.

Nevertheless, it’s worth noting the FTSE 100 futures market had still only moved about 2% in the space of five sessions.

A major watch point was the market’s ability to resolve a gap between low volume trade on 26th June and Monday 29th, between which Greece’s PM Tsipras made the shock announcement of a referendum on the EU’s latest conditions for continued aid.

Please click for larger image

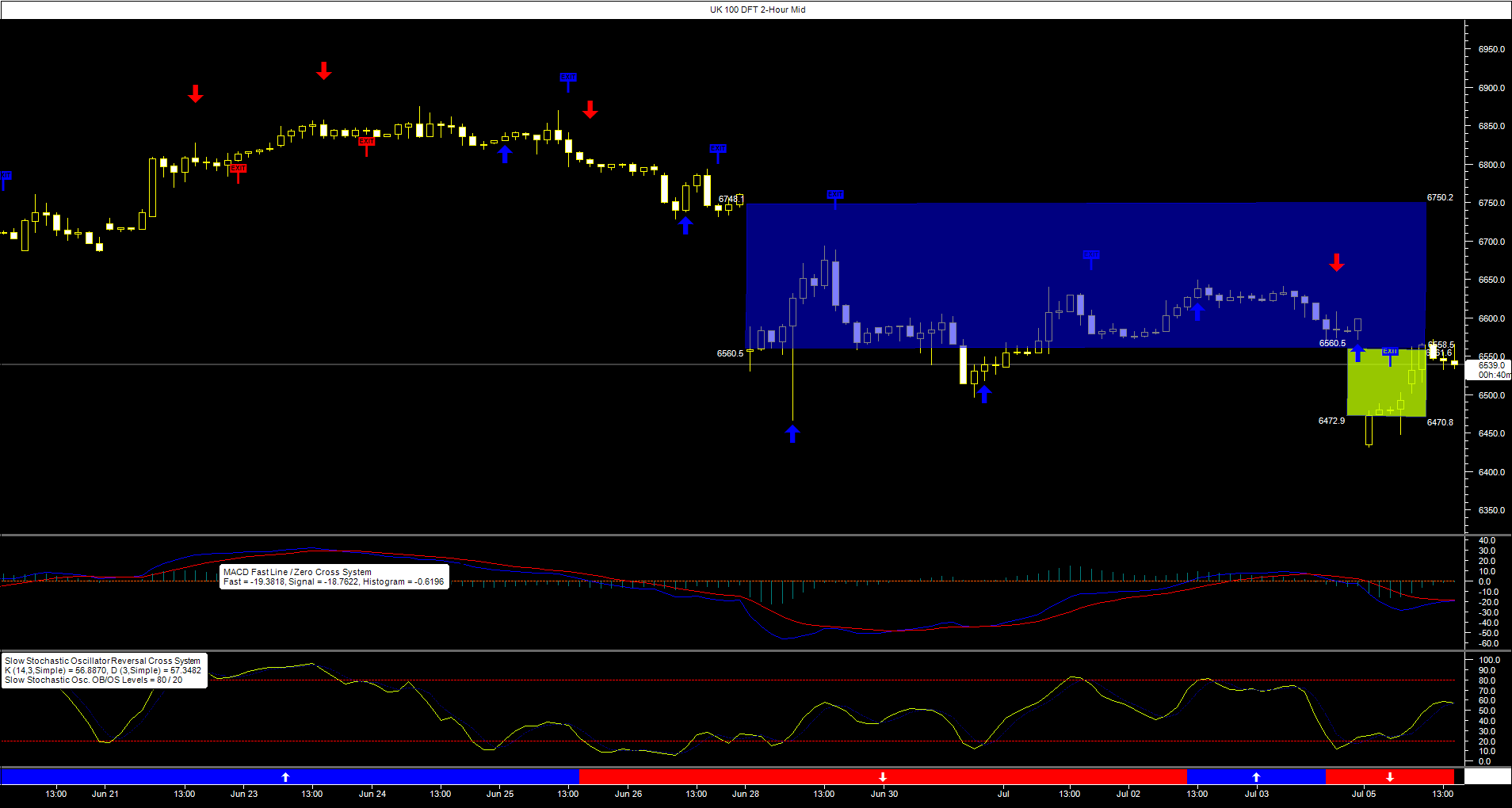

Two-hourly trading in City Index’s FTSE 100 analogue, UK 100 Daily Funded Trade, had also singularly failed, at the time this article was being updated, to close a similar gap that opened at the same time as that of the futures market.

The UK 100 could not surmount the divide, despite three visible attempts during the intervening period, backed by favourable momentum (viewed within the same two-hour interval series.)

A build up of sellers was implied within the gap, with logical but not absolute evidence from a ‘go short’ signal emitted by a MACD-based trading system during the afternoon of late Friday.

No further attempt has been made on the larger gap, since last Friday, a day which brought a shorter-lived gap, that closed on Monday.

In keeping with the main unresolved macroeconomic question that Greece essentially asked itself at the beginning of last week, about long-term membership of the Eurozone, the FTSE’s (and the UK 100′s) larger trading divide will remain its main focus until it closes.

Please click for larger image