- Stock market recovery appears to have staying power

- A revival of earnings, valuations and M&A interest

- Political volatility vs. stock market calm

European shares bounce bigly

Despite a softer end to the week, European shares have started the month with solid gains setting the region’s benchmark on course for a sixth weekly gain out of 9, with only three down weeks since the start of the year. The STOXX Europe 600’s rise reflects multi-month highs this week for Germany’s DAX, France’s CAC-40 and other major indices.

Donald Trump’s closely watched speech to Congress this week was the obvious trigger for European markets, like their global peers, to extend the tear they’ve been on since early November.

It barely seems to matter that the president’s address offered few fresh details on tax and healthcare reform, infrastructure spending and other kites the administration has flown for weeks. U.S. indices are tilting at a near-parabolic angle nonetheless, largely on momentum, though also pricing Trump’s more measured, optimistic and conciliatory tone, this week.

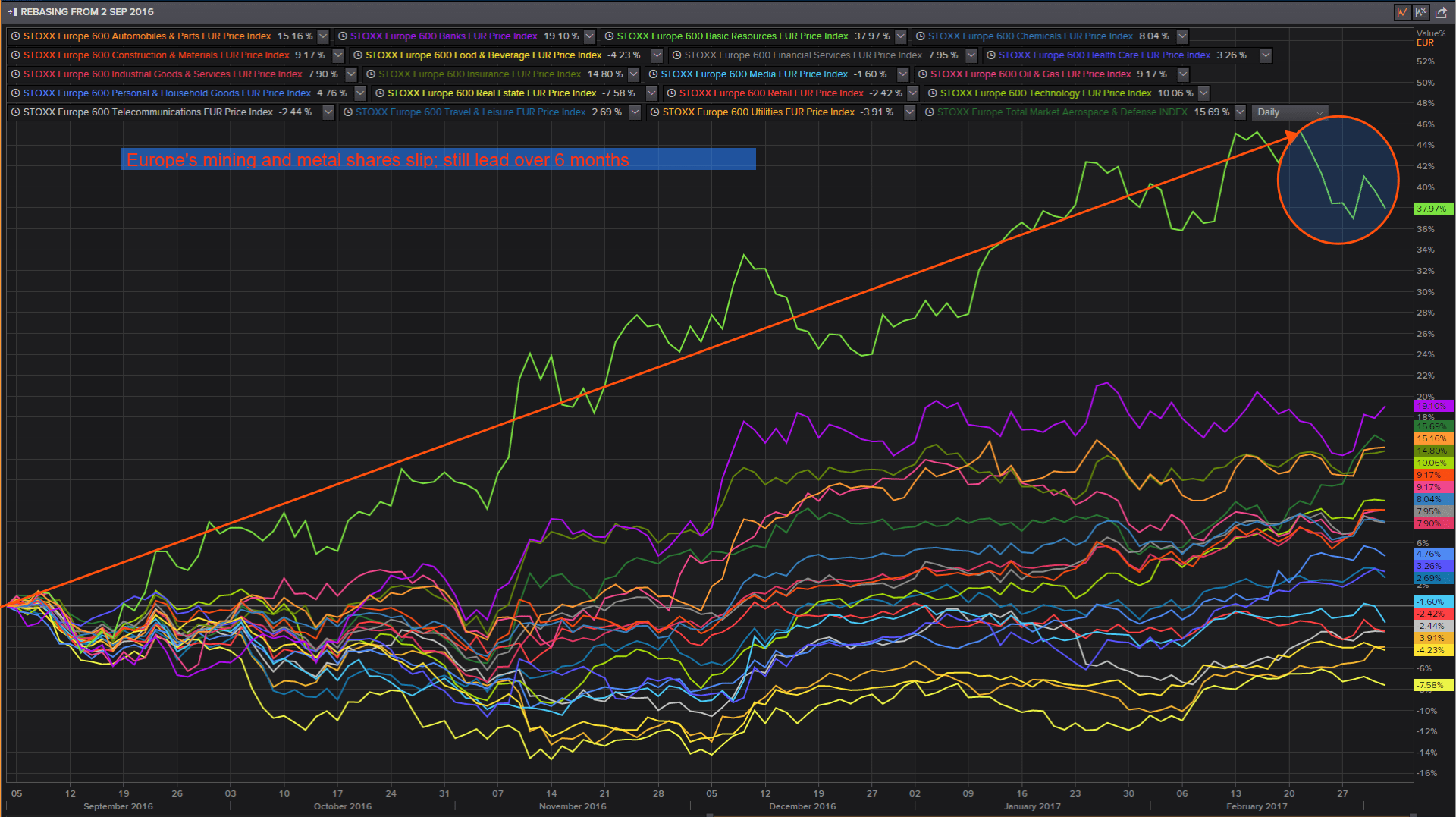

Together with signs of an upturn in demand in China for key metals like iron ore and copper, a key premise of the ‘Trump trade’ is an increased need for construction materials. This is clearly demonstrated by the exaggerated outperformance of Europe’s basic resources shares over six months, shown in a rebased chart of STOXX’s European sub-indices below.

Sub-indices rebased

Source: Thomson Reuters and City Index

The long, cold winter ends

Sketchy U.S. policy projections potentially set the stage for a significant near-term global setback when exuberance wears off, and, assuming investors’ normal tendency to rotate towards more defensive sectors under such circumstances, a correction may hit hardest amongst the continent’s mining and metals shares.

Europe’s performance, however, does differ from the states in that the rise of continental equities in the first two months of 2017 confirms a recovery from a longer malaise, in line with Europe’s persistent economic slump. It’s one which placed four Eurozone indices among the world’s 10 worst performers as recently as 2016. That sharpens the contrast with where EU equities stood around the same time last year.

Late in February 2016, the STOXX 600 index had just handed back the last of the gains made since September 2013, on rising trepidation ahead of Britain’s referendum and persistently sluggish earnings. Fast forward to now, and valuations are rising at a moderate pace whilst earnings show signs of stabilisation. The STOXX 600’s forward P/E is a level-headed 19.1 times 2017 earnings, according to Thomson Reuters, against 22.3 in 2016.

Eurozone large-caps are growing into those expectations. Fourth quarter earnings are up 3.7% on the year, so far. Including a resurgent energy sector, they’re 11.5% better. Whilst income among the largest European companies fell about 2% in 2016 overall, the final quarter showed an upturn from the 5% decline in Q3, a 14% fall in Q2, amid referendum-fuelled currency volatility, and a 3% slip in Q1.

A renewed appetite for deal-making is another positive sign for Europe’s blue chips. Whilst a blow-out 2015 for global M&A was always going to be tough to beat, Western Europe’s contribution halved from 33% in 2015 to 16% in 2016, a sharp slowdown which may be difficult to bounce back from this year. However a 16% rise on the year in deals above $500m announced in Q4 2016 and a 31% jump in the first six weeks of 2017 are promising.

The view is backed by several recent high profile deals in Europe within the first two months of the year, including Cinven’s offer to Germany’s Stada, J&J’s acquisition of Actelion and Peugeot’s planned acquisition of GM’s Opel. The activity points to an unusual sweet spot for M&A with benefits from a currency discount and expectations of economic and corporate growth. It’s no coincidence that recent inflation data have built on Europe’s green shoots of growth last year, as business surveys (PMI) approach six-year highs.

European fund flows are tracking this optimism. EPFR data shows institutional investors bought $1.1bn in European equities in the 7 days to 22nd February, almost matching the entire inflow of the four weeks before. Interest is underlined by evidence that investors are opting to maintain exposure to equities whilst circumventing political risks. Redemptions from funds invested only in French shares were the largest since October, while Dutch stock funds posted their 13th weekly outflow out of 14.

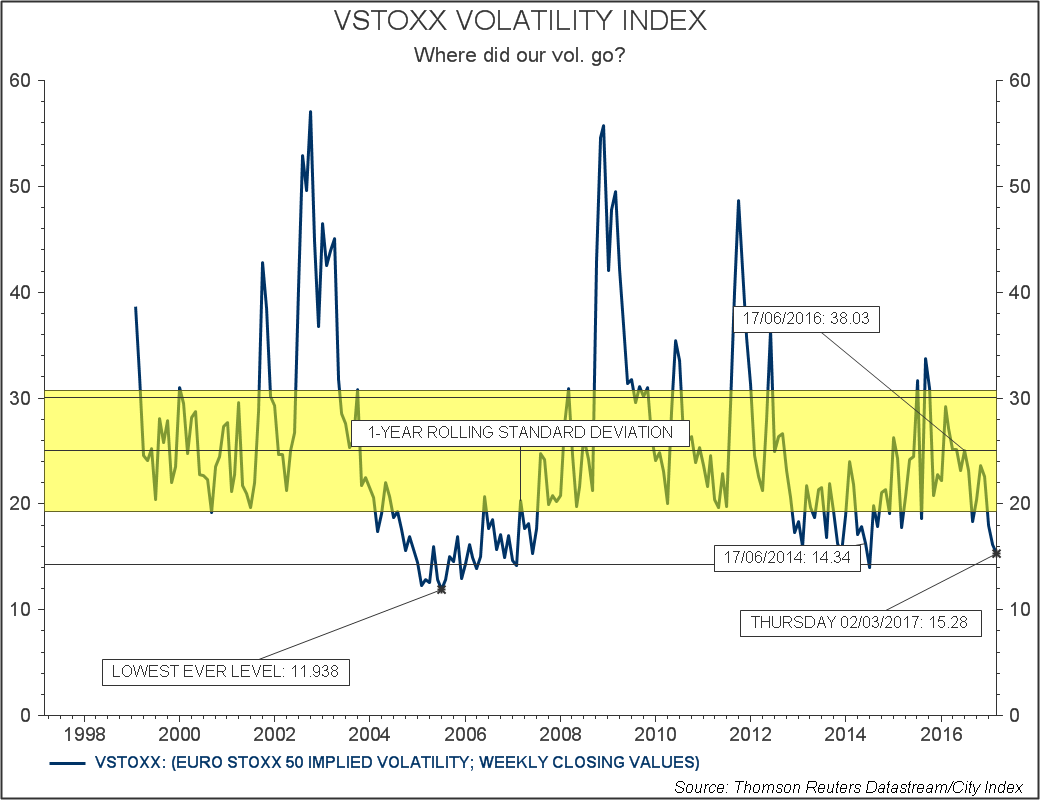

Whither volatility

For the market, then, the timing of elections across Europe after last year’s anti-establishment upsets could be taxing, but a higher exponent of anxieties than is currently evident or the worst possible outcomes, from the market’s point of view, would seem to be necessary to stop the equity market recovery in its tracks.

To nerves surrounding French, Dutch, German and perhaps Italian elections, we should add Greece’s ‘hard deadline’ in July to agree a new bail out agreement, or else see repayments balloon to €8bn a month. Markets do, however, seem to be habituating to such anxieties, even if investors are having to become accustomed to galloping bond yields and currency volatility too. Still, the most significant recent upsets have barely moved the dial of traditional volatility gauges and markets recovered quickly from all three of last year’s unwanted ballot results.

As such, Europe’s volatility index is trading near historic lows, just like its more closely followed U.S. counterpart, the VIX. Eurex exchange’s VSTOXX Volatility Index (which measures implied volatility of the Euro Stoxx 50 index) recently notched its lowest reading since mid-June 2014, around 2½ points from its lowest-ever close.

The appearance of relative global calm might well be deceptive on both sides of the Atlantic given that the Federal Reserve is still the only G7 central bank in a hiking cycle. At, the same time, a cursory examination of the chart below also reminds us that the VSTOXX, like the VIX, has a notable tendency to rally after falling out of its long-term standard deviation. The pattern is known as ‘mean reversion’ and it reminds us that market calm can be followed by storms.

Still, even though the Fed has ended its easing phase (with an encouraging kick from the ‘Trump-trade’) a VIX barely up from all life-time lows coincided with a string of U.S. stock market records. It shows that benefits for U.S. equities can continue despite the Fed’s newly assertive tightening stance, so long as tightening itself is tortuously slow.

For euro-denominated stock markets, where the weak currency’s inverse correlation with equities is clear, and the European Central Bank insists it will make no changes to easy-money before December, sustained and measurable stock turbulence looks set to remain at least as scarce as in the U.S. for the foreseeable future. It’s another cautious tick for prospects of continued gains.

Source Thomson Reuters Datastream and City Index