Asian Indices:

- Australia's ASX 200 index fell by -16.3 points (-0.22%) and currently trades at 7,421.00

- Japan's Nikkei 225 index has fallen by -166.58 points (-0.54%) and currently trades at 30,503.52

- Hong Kong's Hang Seng index has fallen by -258.06 points (-1.01%) and currently trades at 25,244.17

UK and Europe:

- UK's FTSE 100 futures are currently up 1 points (0.01%), the cash market is currently estimated to open at 7,035.06

- Euro STOXX 50 futures are currently up 4.5 points (0.11%), the cash market is currently estimated to open at 4,196.17

- Germany's DAX futures are currently up 10 points (0.06%), the cash market is currently estimated to open at 15,732.99

US Futures:

- DJI futures are currently down -292.06 points (-0.84%)

- S&P 500 futures are currently up 18.75 points (0.12%)

- Nasdaq 100 futures are currently up 6 points (0.13%)

Learn how to trade indices

Indices

Asian equity markets were lower overnight as weak economic data from China weighed on sentiment across the region. Retail sales rose just 2.5% compared with 10.5% expected, and down from 8.5% prior, making it the weakest print this year. Industrial output fell to its lowest level since July 2020 with motor vehicles and steel products weighing the headline number as COVID restrictions continued to take a bite out of the economy. Fixed asset investments also disappointed, falling to 8.9% down from 10.3%, missing 11.3% estimates. The Hang Seng fell around -1%, the China A50 traded -0.76% lower and the CSI300 was down -0.35%.

The FTSE 100 gave back most of Monday’s gains yesterday although has found support at the 100-day eMA. Yet the 50-day eMA and 7090 resistance level continued to cap any upside and volumes were their highest yesterday since Thursday’s bearish candle, so perhaps bears are preparing to drive it back down to 7,000 (and maybe even beyond).

FTSE 350: Market Internals

FTSE 350: 4069.91 (-0.49%) 14 September 2021

- 102 (29.06%) stocks advanced and 226 (64.39%) declined

- 5 stocks rose to a new 52-week high, 9 fell to new lows

- 69.23% of stocks closed above their 200-day average

- 57.26% of stocks closed above their 50-day average

- 17.38% of stocks closed above their 20-day average

Outperformers:

- + 9.72% - JD Sports Fashion PLC (JD.L)

- + 4.88% - 888 Holdings PLC (888.L)

- + 4.09% - WH Smith PLC (SMWH.L)

Underperformers:

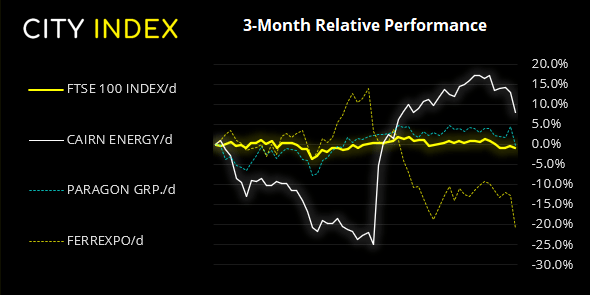

- -9.44% - Ferrexpo PLC (FXPO.L)

- -4.48% - Paragon Banking Group PLC (PAGPA.L)

- -4.29% - Cairn Energy PLC (CNE.L)

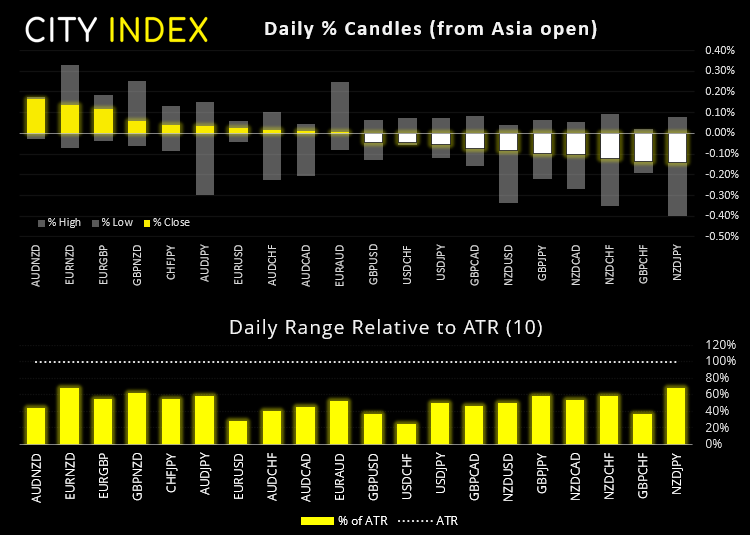

Forex: Yen catches a bid

The Japanese yen caught a bid against NZD and GBP pairs following weak China data. Should The Japanese yen caught a bid against NZD and GBP pairs following weak China data. Should sentiment remain fragile today then JYP could continue to remain bid, making GBP/JPY an ideal short candidate if this data misses the mark.

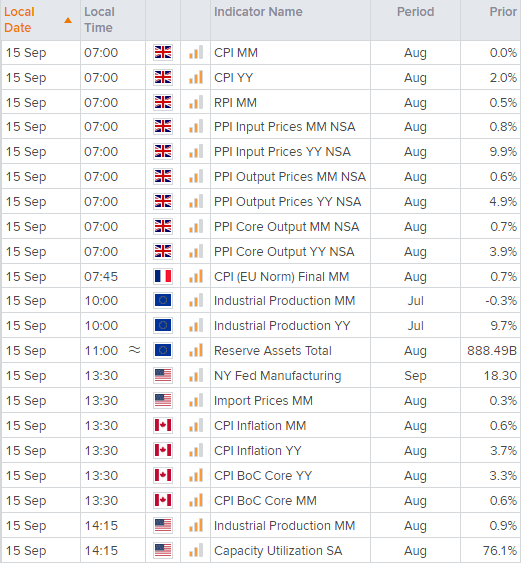

UK inflation data is released at 07:00 BST, and it could be of greater significance given bullish comments from some BOE members of late. Last week Governor Bailey said the MPC were 4-4 split on whether the minimum requirement to raise rates has been met, which is a huge jump from 8 voting against a hike. And data shows that wage pressures have risen considerably, which is something that BOE will continue to monitor. Should we see stronger inflation (both at the consumer and producer level) then it brings forward expectations for a hike from Q4 2020 as the polls currently suggest.

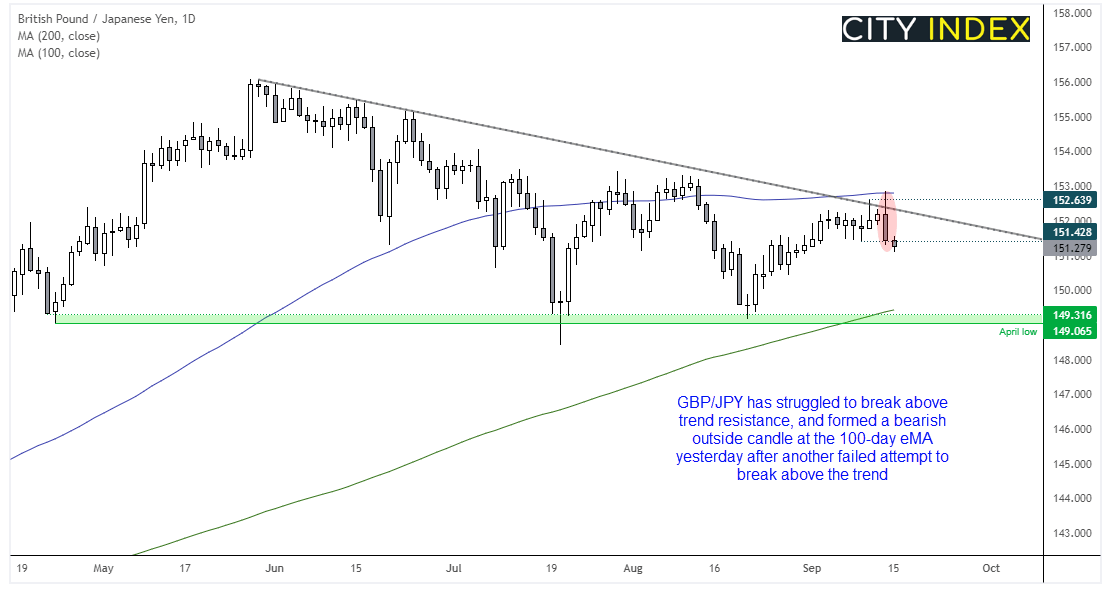

GBP/JPY is of interest should we see a disappointing inflation report. Prices have so far struggled to break above trend resistance, with its latest failed attempt resulting in a large bearish engulfing/outside bar closing to 2-week low and testing the monthly pivot point. Due to the size of yesterday’s bearish candle at resistance we maintain a bearish bias below 153 on the daily chart, with the potential to run for 150 or even the low around 149.06/30.

Learn how to trade forex

Commodities: Gold rises against all major currencies

Gold is trying to make its mark against the US dollar having closed above 1800 yesterday, but it’s worth noting it was broadly higher against all major currencies following yesterday’s CPI report in the US. However, gold looks particularly appealing to the bull camp against the Australian dollar, looking at the range expansion candle at the 200-day eMA on XAU/AUD yesterday. And if gold begins to rally, then it could even provide a pillar of support for silver which has now printed a bullish pinbar and bullish hammer over the past two days.

The CRB commodity index hit a new 6-year high yesterday after breaking out of a flag pattern on Monday. We’ll see if it can hold onto these gains despite weak China data, although structurally the minor daily trend remains bullish above 216.84.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM