Asian Indices:

- Australia's ASX 200 index rose by 10.5 points (0.14%) and currently trades at 7,369.50

- Japan's Nikkei 225 index has risen by 34.15 points (0.1%) and currently trades at 29,047.07

- Hong Kong's Hang Seng index has risen by 170.43 points (0.6%) and currently trades at 28,729.02

UK and Europe:

- UK's FTSE 100 futures are currently up 8 points (0.11%), the cash market is currently estimated to open at 7,161.43

- Euro STOXX 50 futures are currently up 2 points (0.05%), the cash market is currently estimated to open at 4,160.14

- Germany's DAX futures are currently up 9 points (0.06%), the cash market is currently estimated to open at 15,736.67

US Futures:

- DJI futures are currently down -210.22 points (-0.62%)

- S&P 500 futures are currently up 33 points (0.23%)

- Nasdaq 100 futures are currently up 5 points (0.12%)

Learn how to trade indices

Indices

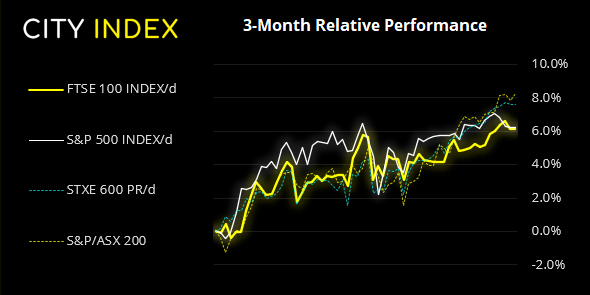

The Nikkei 225 was a touch higher on Friday as tech stocks tracked the Nasdaq 100, which itself closed to a record high overnight. The ASX 200 was just a few points from its record high (despite a soft start) and is currently on track for a bullish outside day to close the week. The Hang Seng was the strongest performer, rising 0.55% Whilst China’s CSI300 is trading -0.64% lower. Ultimately, equities have avoided the levels of relative volatility seen across commodity and forex markets and, overall, can say that equity bulls have taken the hawkish FOMC meeting in their stride and could indeed be looking for fresh highs. And this makes sense as any potential rate hike is still year/s away and there is no actual talk of tapering just yet.

European futures have opened a touch higher with the STOXX 50 currently up by 0.7%, the DAX rising 0.03% and the FTSE up 011%. The FTSE 100 fell to a three-day low yesterday but found support at its 20-day eMA before paring losses. The weekly candle is on track for a bearish pinbar.

FTSE 100 S/R Levels

- R3: 7200 - 7204

- R2: 7198

- R1: 7169 – 7172.21

- Pivotal: 7157

- S1: 7143

- S2: 7132 - 7138

- S3: 7118 - 7122

FTSE 350: Market Internals

FTSE 350: 4089.67 (0.07%) Week to Date:

- 256 (72.93%) stocks advanced and 77 (21.94%) declined

- 20 stocks rose to a new 52-week high, 2 fell to new lows

- 85.75% of stocks closed above their 200-day average

- 19.94% of stocks closed above their 20-day average

Outperformers:

- + 7.86% - Ultra Electronics (ULE.L)

- + 7.20% - BT Group (BT.L)

- + 5.71% - Volution Group (FAN.L)

Underperformers:

- -12.6% - Dr Martens (DOCS.L)

- -9.40% - Hammerson (HMSO.L)

- -9.04% - Anglo American (AAL.L)

Forex:

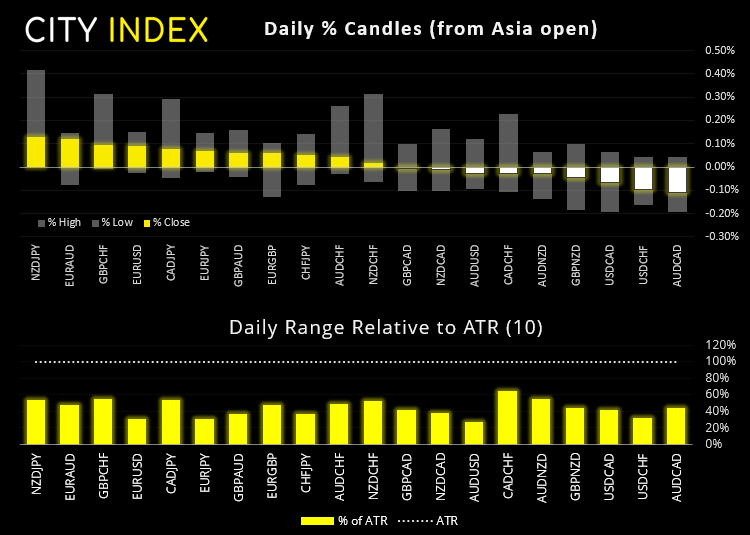

The US dollar index (DXY) also retraced overnight by a marginal 0.02%, but it looks like it wants to turn higher for another attempt at new highs. There’s not a lot of market driving news scheduled after retail sales, so it’s likely to be down to how much short covering there is left as to how higher the dollar could travel before the week’s close. Famous last words, but we do not expect the same kind of volatility across FX markets like we’ve seen the past two days, especially if bulls and bears are closing out ahead of the weekend.

Barring a miraculous recovery, EUR/USD is on track for its worst week since October. Now trading beneath its 200-day eMA we suspect bears could seek to fade into minor rallies below 1.1950, although a key level of support today is clearly going to be 1.1900 (which it sits just 15 pips above at the time of writing).

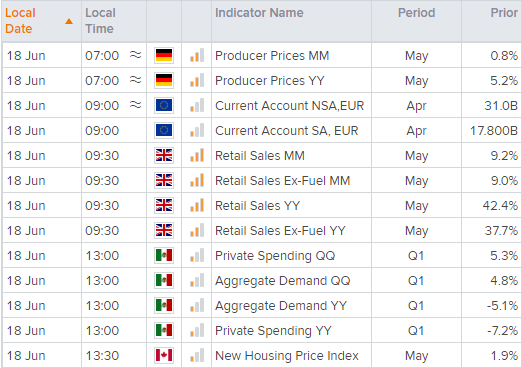

UK retail sales is up at 09:30 BST, although we doubt it will maintain the momentum of a 42.4% annual rise seen in May. Although given the strength of the US dollar then a weaker than expected report could send cable lower still.

GBP/USD closed below 1.3900 yesterday although retraced through parts of the overnight session, et momentum is now turning lower ahead of today’s retail sales. A swing high has formed at 1.3945, so a break above it warns of a deeper correction. Until then, the bias remains for a retest of 1.3900 and potentially yesterday’s low.

Learn how to trade forex

Commodities: 72.0 could be pivotal for Brent futures

Metals retraced overnight against their overtly bearish moves seen the prior session, although the relatively light retracements are more likely to be traders squaring their positions up ahead of the weekend than anything more meaningful. Palladium rose 1.84%, platinum rose 1.5% whilst silver and gold rose 1.08% and 0.65% respectively.

Oil prices were lower for a third day as WTI retested yesterday’s low yet remains above 70.0 ahead of the European open. Brent futures are also lower, although it has printed a bullish pinbar on the four-hour chart to show demand at 72.00.

If we switch to the hourly chart, we can see that the weekly pivot, 100-hour eMA and 72.00 are providing support. So we need to see prices recover from here to be confident the low is in place. However, bearish momentum from its 74.95 high is more aggressive than the bullish momentum that led prices to that high, so we are on guard for a break of yesterday’s low which could signal its next leg lower. And how the US dollar behaves today is likely to be a major part of which side of 72.00 brent closes on today.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM