Asian Indices:

- Australia's ASX 200 index rose by 13.9 points (0.19%) and currently trades at 7,516.90

- Japan's Nikkei 225 index has fallen by -33.39 points (-0.12%) and currently trades at 27,701.57

- Hong Kong's Hang Seng index has fallen by -93.54 points (-0.36%) and currently trades at 25,634.38

UK and Europe:

- UK's FTSE 100 futures are currently down -2 points (-0.03%), the cash market is currently estimated to open at 7,123.78

- Euro STOXX 50 futures are currently down -2 points (-0.05%), the cash market is currently estimated to open at 4,176.08

- Germany's DAX futures are currently down -23 points (-0.14%), the cash market is currently estimated to open at 15,882.85

US Futures:

- DJI futures are currently up 30.55 points (0.09%)

- S&P 500 futures are currently down -5.5 points (-0.04%)

- Nasdaq 100 futures are currently down -3.75 points (-0.08%)

Learn how to trade indices

Indices mixed during Asian trade

Shares were mixed overnight, with Japan’s equity markets initially taking Wall Street’s lead yet gave back earlier gains and currently trade flat. The ASX 200 is currently 0.2% higher amidst its third bullish day, yet also on track to form its second consecutive bearish hammer on the daily chart. Hong Kong shares underperformed with the Hang Seng and Enterprise index down around -0.36% and -0.56% respectively. Futures markets in US and Europe have opened slightly lower, with the Dow Jones E-mini down -0.13% and S&P contract down -1.1%. FTSE 100 futures are also -0.05% lower.

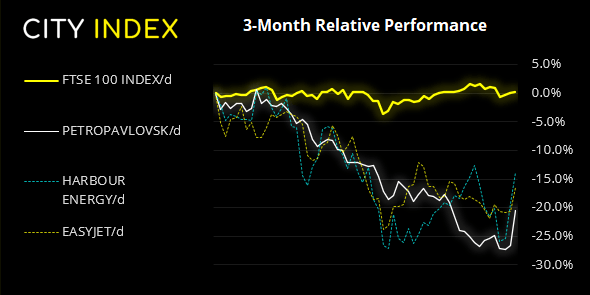

FTSE 350: Market Internals

FTSE 350: 4119.52 (0.24%) 24 August 2021

- 224 (63.82%) stocks advanced and 115 (32.76%) declined

- 32 stocks rose to a new 52-week high, 1 fell to new lows

- 74.36% of stocks closed above their 200-day average

- 100% of stocks closed above their 50-day average

- 20.23% of stocks closed above their 20-day average

Outperformers:

- + 8.36% - Petropavlovsk PLC (POG.L)

- + 6.70% - Harbour Energy PLC (HBR.L)

- + 5.32% - Easyjet PLC (EZJ.L)

Underperformers:

- - 4.85% - J Sainsbury PLC (SBRY.L)

- - 4.00% - Volution Group PLC (FAN.L)

- - 3.33% - NCC Group PLC (NCCG.L)

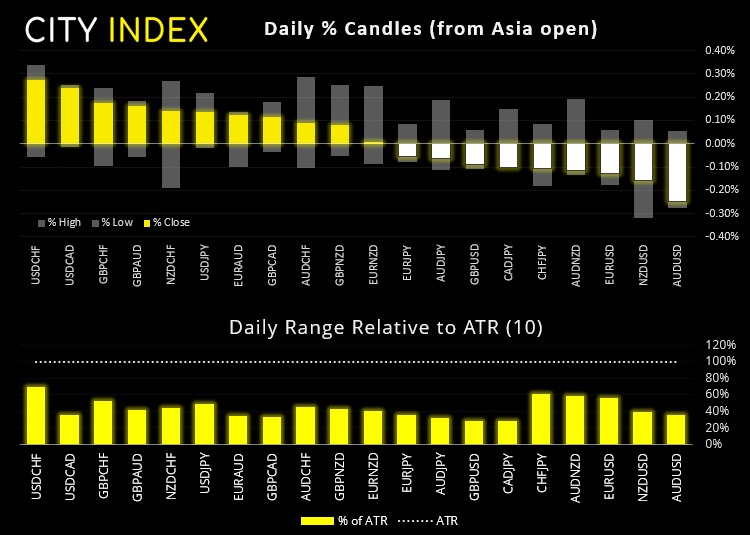

Forex volumes remain low overnight

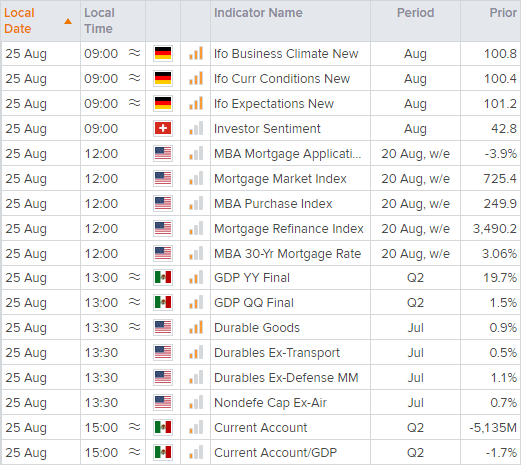

It’s a relatively quiet calendar in today’s European session, although Germany’s IFO business sentiment report is always worth a look. The report for July fell from its highest level since April 2019 as morale took a dent from supply shortages and virus concerns. Should we see it dip lower today then it could instil fears that the economy has topped and likely weigh on the euro as a consequence. As it stands, IFO business expectations are forecast to rise to 102.6 from 102.2, the business situation is expected to soften to 100.1 from 100.4 and the business climate rise to 101.2 from 100.8.

The US dollar index (DXY) is 0.13% higher and back above 0.9300, and we suspect moves may be limited leading into Jackson Hole, unless we see some extreme prints out of today’s durable goods report.

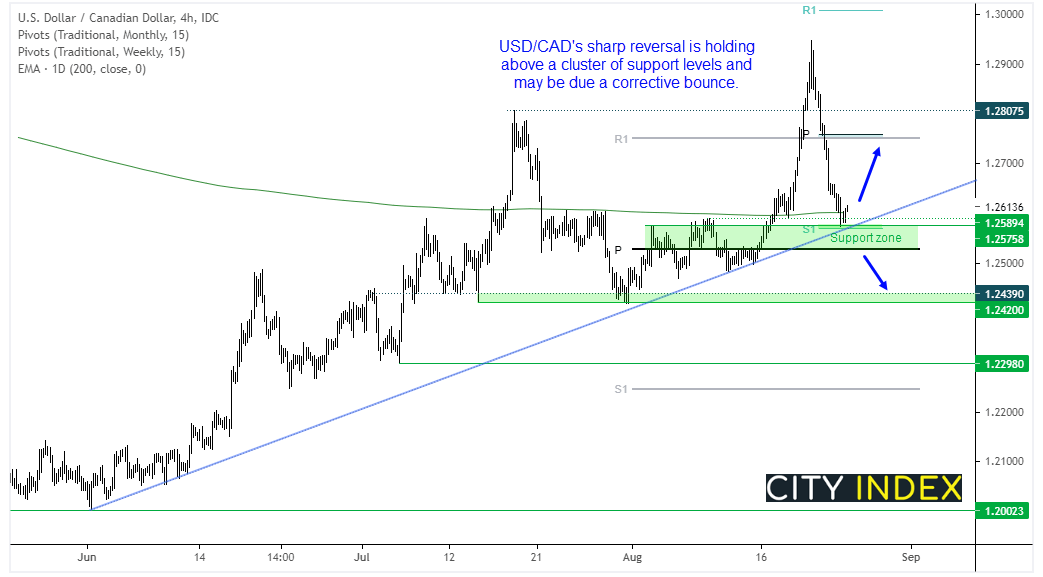

USD/CAD could be set for a corrective bounce, given the plethora of support levels nearby after a relatively deep pullback against the bullish trend on the four-hour chart. Prices are holding above trend support and meandering around the 200-day eMA and the weekly S1 pivot, and just below these level sits the monthly pivot point. If we see a trendline break we’d want to see prices break beneath the monthly pivot before considering a short bias. And, until then we’re looking for prices to rebound from the support zone / trendline and move towards 1.2700 (with the monthly R1 and weekly pivot also making a viable target at 1.7250.

Learn how to trade forex

Commodities slightly softer, but no major concern

Commodities are slightly lower as the US dollar recouped a bit of strength, although moves lack any meaningful conviction to be taken as anything other than holding patterns. WTI has retraced to the monthly S1 pivot at 67.0, and the weekly S1 level sits at 66.31.

Gold prices were around -0.4% lower overnight as the dollar regained strength, scuppering hopes of another bull Flag breakout. In fact, today’s move lower also means the breakout we saw on Monday cannot be part of a larger bull flag breakout, although if prices stabilise above the 1790 area then perhaps we’ll see a swing higher form (should dollar bears return).

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 05:00 PM

Today 07:55 AM

Today 04:47 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM