Asian Indices:

- Australia's ASX 200 index rose by 68.4 points (0.93%) and currently trades at 7,392.70

- Japan's Nikkei 225 index has risen by 126.18 points (0.43%) and currently trades at 29,520.90

- Hong Kong's Hang Seng index has fallen by -242.63 points (-0.97%) and currently trades at 24,857.04

- China's A50 Index has fallen by -102.59 points (-0.66%) and currently trades at 15,443.87

UK and Europe:

- UK's FTSE 100 futures are currently down -7 points (-0.1%), the cash market is currently estimated to open at 7,267.81

- Euro STOXX 50 futures are currently down -2 points (-0.05%), the cash market is currently estimated to open at 4,294.22

- Germany's DAX futures are currently down -3 points (-0.02%), the cash market is currently estimated to open at 15,951.45

US Futures:

- DJI futures are currently up 138.79 points (0.39%)

- S&P 500 futures are currently down -3.75 points (-0.02%)

- Nasdaq 100 futures are currently down -5.25 points (-0.11%)

Indices

Asian equity markets were mixed despite the strong lead from Wall Street as traders appear cautious ahead of today’s FOMC meeting.

Futures markets are a touch lower pointing to a marginally softer open, although not by a wide enough margin to cause concern. The FTSE 100 extend Monday’s rally, instead printing a bearish hammer candle which almost spanned Monday’s range. The lower close on high volume suggests all is not well at these highs. The STOXX 50 however has risen to a fresh 13-year high, and our bias remains bullish above gap support around 4250.

FTSE 350: Market Internals

FTSE 350: 4166.17 (-0.19%) 02 November 2021

- 150 (42.74%) stocks advanced and 184 (52.42%) declined

- 18 stocks rose to a new 52-week high, 8 fell to new lows

- 60.68% of stocks closed above their 200-day average

- 46.44% of stocks closed above their 50-day average

- 24.79% of stocks closed above their 20-day average

Outperformers:

- + 3.16%-AstraZeneca PLC(AZN.L)

- + 2.94%-Bridgepoint Group PLC(BPTB.L)

- + 2.94%-Volution Group PLC(FAN.L)

Underperformers:

- ·-10.92%-TP ICAP Group PLC(TCAPI.L)

- ·-9.25%-Diversified Energy Company PLC(DEC.L)

- ·-7.85%-Standard Chartered PLC(STAN.L)

Forex:

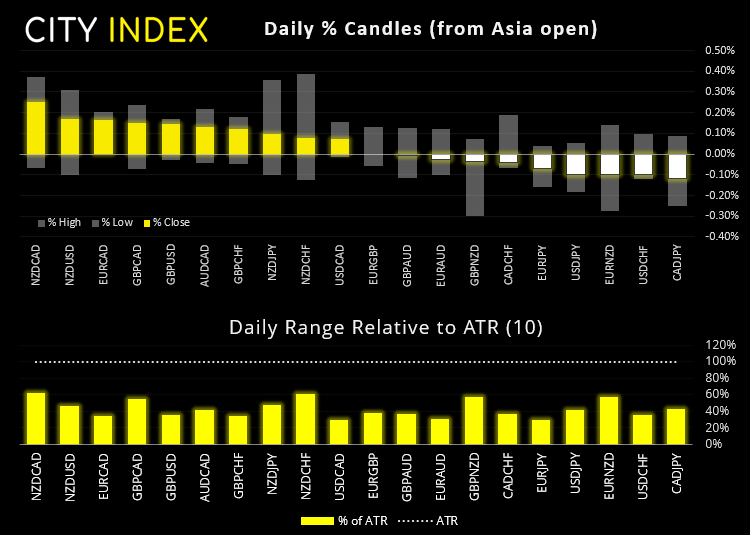

NZD was the strongest major, but not by much considering its stonking employment report. Unemployment fell to a record low of 3.4%, down from 4% and far exceeding the 3.9% expected. Jobs grew by 2% in Q3, up from Q1 previously. Which is not bad considering NZ were in lockdown. Yet the Kiwi dollar could only muster a 0.17% rise as traders are already expecting a 50 bps hike this month and traders are seemingly reluctant to commit to risk ahead of today’s FOMC meeting.

NZD/USD is trading just below 0.7130 resistance. Should it be deemed a hawkish meeting (firm tapering plan, perhaps even hints of a rate rise sooner than later) then NZD/USD could get comfortably below 0.7100. Yet a ‘lame taper’ plan with no hiking clues could see traders embrace NZ’s employment report and send it towards 0.7200.

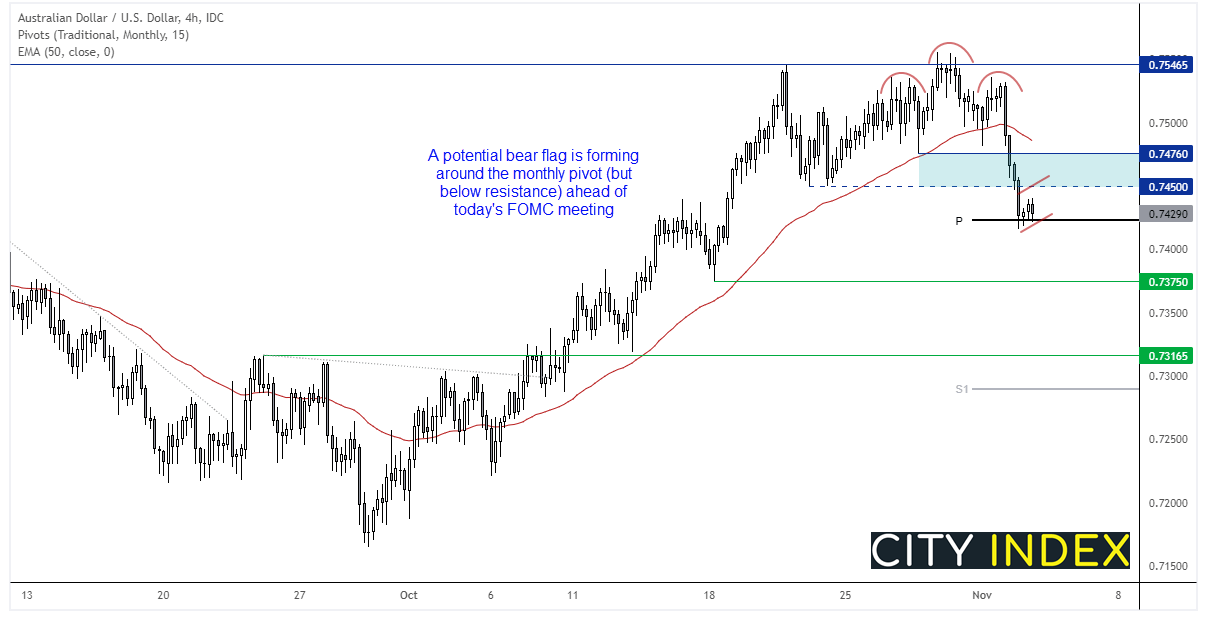

As we’re leaning towards a hawkish meeting, we think AUD/USD may make the better short given RBA’s dovish meeting yesterday. Bearish momentum accelerated from the RS (right shoulder) of its head and shoulders top. It closed the day beneath 0.7450 support and we’re hoping it will cap as resistance. A potential bear flag is forming at the lows, but support has been found at the monthly pivot. So from here we’re hoping a hawkish Fed and provide the catalyst required for AUD to head below 0.7400.

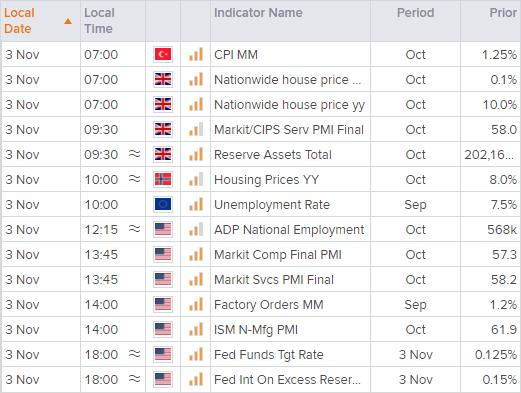

The ISM services PMI is released at 14:00 BST. Like the manufacturing PMI, it remains historically high yet down from its record high printed earlier this year. Being a gauge for inflation, the prices paid component will be closely watched. It sits at 77.5, down from its peak at 83.5 but above its long-term average of 59.

BOE Governor Andrew Bailey speaks at the COP26 Summit at 16:00 GMT, in a speech titled ‘Laying The Foundations for a Net Zero Financial System”.

And we should probably discuss today’s FOMC meeting. They are fully expected to announce tapering, so the focus is on by how much and when. Consensus is for a December start and, as Powell has already indicated they could be fully unwound by mid-2022, estimates are for tapering to sit around $15 billion per month across their securities.

Commodities:

Platinum appears to be one of the stronger metals (no pun intended), and prices are holding above Thursday’s high. Should we see a weak USD scenario today it remains our favoured long for any metals trade, given its strong rally on Monday.

Up Next (Times in BST)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM