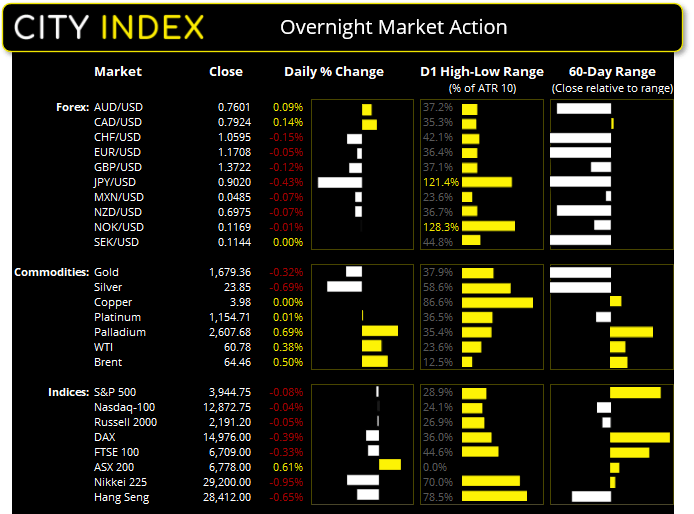

Asian Indices:

- Australia's ASX 200 index rose by 52.3 points (0.78%) to close at 6,790.70

- Japan's Nikkei 225 index has fallen by -239.47 points (-0.81%) and currently trades at 29,195.43

- Hong Kong's Hang Seng index has fallen by -118 points (-0.41%) and currently trades at 28,459.50

UK and Europe:

- UK's FTSE 100 futures are currently down -22.5 points (-0.33%), the cash market is currently estimated to open at 6,749.62

- Euro STOXX 50 futures are currently down -13 points (-0.34%), the cash market is currently estimated to open at 3,913.20

- Germany's DAX futures are currently down -59 points (-0.39%), the cash market is currently estimated to open at 14,949.61

Tuesday US Close:

- The Dow Jones Industrial fell -104.41 points (-0.31%) to close at 33,066.96

- The S&P 500 index fell -12.54 points (-0.32%) to close at 3,958.55

- The Nasdaq 100 index fell -69.21 points (-0.53%) to close at 12,896.53

The FTSE 100 closed to an 8-day high and rebounded from its 10-day eMA. Closing the session at 6772.12 and not quite testing the 6800 target, upside potential from current levels appears limited until we break to new cycle highs. At the stock level, International Consolidate Airlines (ICAG) and Barclays (BARC) were the top performers, rising 5.1% and 4.9% respectively, whilst Fresnillo (FRES) and Ocado (OCDO) were the worst performers, falling -4.1% and -2.3% respectively.

- US yields were a touch higher overnight with the US 10 year now yielding 1.74% and the 30-year at 2.4%.

- The CSI300 and TOPIX index gave back most of yesterday’s gains, falling -1.1% and -0.8% respectively.

- Futures markets and trade in Asia points towards a weaker open today.

China PMI’s expand at a faster rate

China’s manufacturing sector continued to rebound, with the main PMI read rising to 51.9, up from 50.6 previously. The headline service PMI also rose to a 4-month high to 56.3 compared with 51.4 previously. Given that both manufacturing have expanded at a faster pace and the service sector added 4.9 points then it should quell fears of a China slowdown.

Forex: USD/JPY hits fresh 1-year high

The Japanese yen was the weakest major overnight, trading broadly lower against majors and the only pairs with any notable volatility. USD/JPY is the only pair to exceed its 10-day ATR and hit fresh highs, rising just shy of 111.00. However, bulls may want to be caution simply entering long at these highs and question upside potential from current levels, for the remainder of the day.

- EUR/USD fell to a 4-month low yesterday and now trades just above the 1.1700 handle. Momentum currently favours further downside and the next major support level is near the November lows, jut above 1.1600.

- USD/CHF is tracking USD/JPY higher and nudged its way to its highest level since July overnight. The bias remains bullish for intraday traders with the next major resistance zone residing around 0.9450/67.

- EUR/GBP closed to a 13-month low yesterday, yet still remains above Monday’s bullish pinbar low. This still leaves the potential for a mean-reversion pop higher, although further downside risks prevail from current levels going into the European open.

- GBP/CHF’s upside potential remains capped by 1.3000 resistance, and prices printed a second consecutive bearish pinbar below this key resistance level. It was also an inside candle to show prices are compressing at their highs.

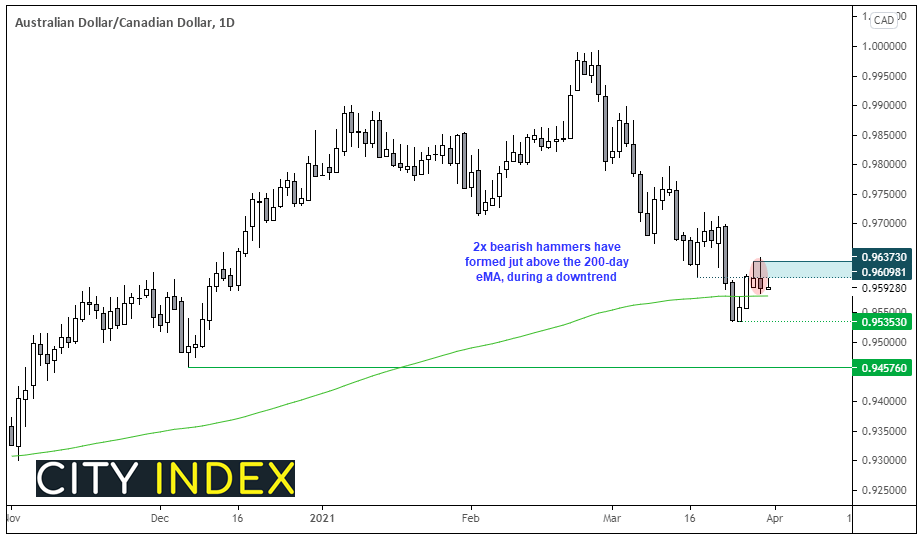

AUD/CAD probes its 200-day eMA

The Canadian dollar ha outperformed the antipodeans these past few weeks which has allowed AUD/CAD to form a downtrend on the daily chart. More recently we saw two large bearish candles form and close beneath the 200-day eMA before retracing higher. Given two bearish hammers have formed, with yesterday’s being a bearish outside day as well, we are monitoring for a break below the 200-day eMA.

- The bias remains bearish below Yesterday’s high.

- A break beneath yesterday’s low / 200-day eMA bearish continuation.

- The initial target is near the 0.9535 low, a break beneath them brings the 0.9457 low into focus.

Commodities: Gold probes key lows

Gold retested 1680 support overnight and the recent pickup of bearish momentum suggests we may see a test (and dare I say, downside break) of 1760 support. A break beneath here would be a significant victory for the bear camp and also call for a revision of its bearish channel as prices accelerate southwards at a faster rate.

Silver prices tested their lowest price of the year overnight after closing beneath $24 yesterday and, if gold breaks lower, we expect silver to follow.

Palladium briefly touched a 2-day high after rebounding above the 2514 support level it crashed towards on Monday. It’s still early days but it is at lest showing the potential to form a higher low above the original breakout level and perhaps resume its longer-term bullish trend.

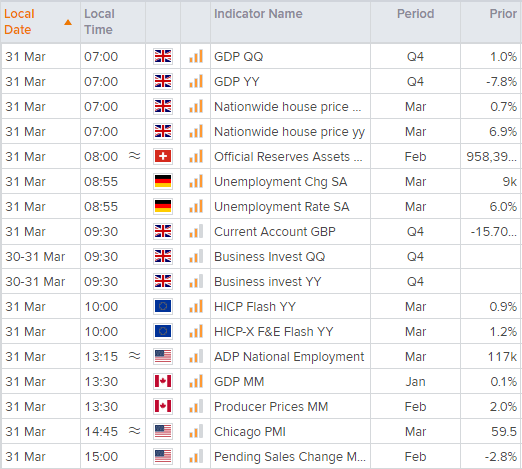

Up Next (Times in GMT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- UK GDP is the main event in the European session, although Q4 growth is expected to remain unrevised at 1.0%. SO, in the event it gets revised markedly lower (especially if it prints a negative) then we could expect some bearish follow-through on GBP pairs.

- President Biden is scheduled to speak on infrastructure near the end of the US session.

Latest market news

Today 05:45 AM

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM