Asian Indices:

- Australia's ASX 200 index rose by 2.8 points (0.04%) and currently trades at 7,494.00

- Japan's Nikkei 225 index has fallen by -154.08 points (-0.56%) and currently trades at 27,588.21

- Hong Kong's Hang Seng index has risen by 130.68 points (0.51%) and currently trades at 25,546.37

UK and Europe:

- UK's FTSE 100 futures are currently up 3.5 points (0.05%), the cash market is currently estimated to open at 7,128.48

- Euro STOXX 50 futures are currently down -2.5 points (-0.06%), the cash market is currently estimated to open at 4,167.37

- Germany's DAX futures are currently down -26 points (-0.16%), the cash market is currently estimated to open at 15,767.62

US Futures:

- DJI futures are currently down -192.38 points (-0.54%)

- S&P 500 futures are currently up 49 points (0.32%)

- Nasdaq 100 futures are currently up 8.75 points (0.2%)

Learn how to trade indices

Stock market indices mixed overnight

Asian equity markets were mixed overnight, although Chinese share markets were leader of the pack on reports that PBOC will provide financial support for rural development and likely lower the RRR to help banks. The CSI300 is up 0.76%, the China A50 index rose 0.9% and the Hang Sang rose around 1%. Japan’s equity indices were lower however, on reports that 1.4 million vaccine doses had to be binned due to contamination. The Nikkei 225 and TOPIX 500 are around -0.3% down for the day.

The DAX remained under pressure yesterday after Wednesday’s weak IFO business sentiment data. Whilst it mostly recouped early losses it remains beneath the gap resistance zone of 15,835 - 15,853, so bears may be tempted to fade into minor rallies beneath this level over the near-term. Although we’d need to see prices break beneath 15,600 (swing low and weekly S1) to suggest another leg lower. German trade data is released at 07:00 BST.

The FTSE 100 closed lower yesterday after failing to break above 7150 resistance and breaking a 3-day countertrend streak. A break beneath 7080 assumes bearish trend continuation.

FTSE 350: Market Internals

FTSE 350: 4121.23 (-0.35%) 26 August 2021

- 102 (20.20%) stocks advanced and 249 (49.31%) declined

- 27 stocks rose to a new 52-week high, 2 fell to new lows

- 60.4% of stocks closed above their 200-day average

- 50.5% of stocks closed above their 50-day average

- 14.46% of stocks closed above their 20-day average

Outperformers:

- + 4.08% - Hays PLC (HAYS.L)

- + 3.92% - CRH PLC (CRH.I)

- + 3.31% - Clarkson PLC (CKN.L)

Underperformers:

- -4.50% - Syncona Ltd (SYNCS.L)

- -3.96% - Ferrexpo PLC (FXPO.L)

- -3.79% - Wizz Air Holdings PLC (WIZZ.L)

Forex: USD/CAD rallies from support

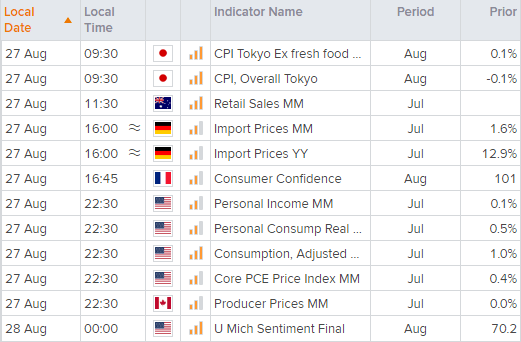

Australian retail sales fell -2.7% in July, more than the -2.3% expected and down from -1.8% previously. And as NSW and VIC remain in lockdowns then there’s a decent chance sales will fall further next month.

Jerome Powell’s keynote speech at 15:00 is of course the main calendar event, but the University of Michigan Consumer Survey released at the same time is worth a look. The preliminary estimate suggested consumer sentiment had fallen to a 10-year low with its month-on-month drop being historically large. So today’s final read should clarify whether it was merely a blip, or confirm that negative sentiment is indeed apparent.

With the US dollar rising yesterday and DXY forming a swing low, we’re now looking for pairs that may continue to weaken against the greenback. Our bias remains bearish on AUD/USD beneath the 0.7300 resistance zone we highlighted yesterday. However, USD/CAD has seen a decent upside since reaction at the support zone and mentioned on Wednesday.

USD/CAD has touched a 4-day high overnight after printing a strong bullish engulfing candle yesterday. Given it was the strongest pair we track yesterday, and confirmed the upper range of the support zone, we retain a bullish bias above this week’s low. And we would welcome any pullbacks into yesterday’s range to (hopefully) increase the potential reward to risk ratio for bulls.

Learn how to trade forex

Commodities tread water ahead of Powell speech

Copper sits at a crossroads. Whilst its recent rebound from 4.0 is meandering around the previously broken trendline, the rally has also paused at trend resistance projected from the July high. A break above this week’s high assumes a revisit of the 4.435 whilst a break back below 4.200 (alongside dollar strength) suggests the swing high was seen earlier this week.

Gold continues to coil up and trades just below 1800 and trend resistance on the daily chart. Should the US dollar strengthen then it may not be the best short among metals, as gold has previously stood up to dollar strength. But should it weaken then gold remains our preferred bullish bias.

Silver however has failed to materialise much on a weaker dollar in recent times. And as it remains below 24.0 resistance, we prefer silver for a short bias should the dollar strengthen today.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 01:15 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM