Asian Indices:

- Australia's ASX 200 index rose by 8.8 points (0.12%) and currently trades at 7,473.40

- Japan's Nikkei 225 index has fallen by -66.57 points (-0.19%) and currently trades at 34,894.12

- Hong Kong's Hang Seng index has fallen by -671.64 points (-2.65%) and currently trades at 24,644.69

UK and Europe:

- UK's FTSE 100 futures are currently up 20 points (0.28%), the cash market is currently estimated to open at 7,078.86

- Euro STOXX 50 futures are currently up 1 points (0.02%), the cash market is currently estimated to open at 4,125.71

- Germany's DAX futures are currently down -7 points (-0.04%), the cash market is currently estimated to open at 15,758.81

US Futures:

- DJI futures are currently down -282.12 points (-0.79%)

- S&P 500 futures are currently down -10.25 points (-0.07%)

- Nasdaq 100 futures are currently down -7.25 points (-0.16%)

Learn how to trade indices

Asian indices lower, futures mixed

In a retaliatory move, the US has limited Chinese passenger planes to 40% capacity after the Chinese government imposed similar limits to four United Airline flight. The China A50 is the weakest index overnight, falling -3% and is currently -5.5% lower this week. The Hang Seng and CSI300 also fell -2.9% and -2.4% respectively. Japan’s share markets also remained under selling pressure as economically sensitive companies dragged the broader markets lower. The Nikkei us down -0.7% and the TOPCI has fallen -0.4%. The ASX 200 is effectively flat at 0.08% and the STI has outperformed with a 0.7% gain. US futures have opened lower led by the Russell 2000 small cap index. FTSE futures are a touch higher whilst DAX futures are flat.

It was the FTSE’s most bearish session in a month yesterday, falling -1.5% to a 2-week by the close, after hefty gap lower at the open. Futures markets suggests I could open higher, around 7083 but bears may be tempted to fade into minor rallies below the 7100 area and re-target the 7,000 low.

FTSE 350: Market Internals

FTSE 350: 4138.53 (-0.16%) 17 August 2021

- 214 (60.97%) stocks advanced and 120 (34.19%) declined

- 37 stocks rose to a new 52-week high, 4 fell to new lows

- 75.5% of stocks closed above their 200-day average

- 75.5% of stocks closed above their 50-day average

- 25.36% of stocks closed above their 20-day average

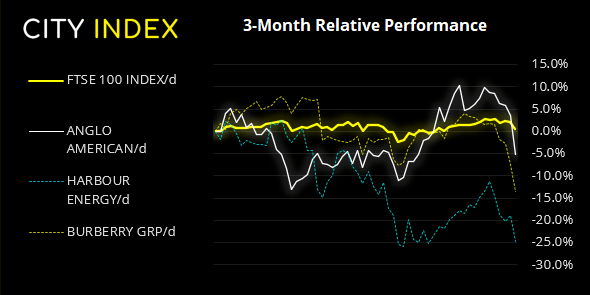

Outperformers:

- + 11.2% - Network International Holdings PLC (NETW.L)

- + 7.11% - Redrow PLC (RDW.L)

- + 5.94% - Ibstock PLC (IBST.L)

Underperformers:

- -7.02% - Balfour Beatty PLC (BALF.L)

- -5.94% - BHP Group PLC (BHPB.L)

- -4.85% - Burberry Group PLC (BRBY.L)

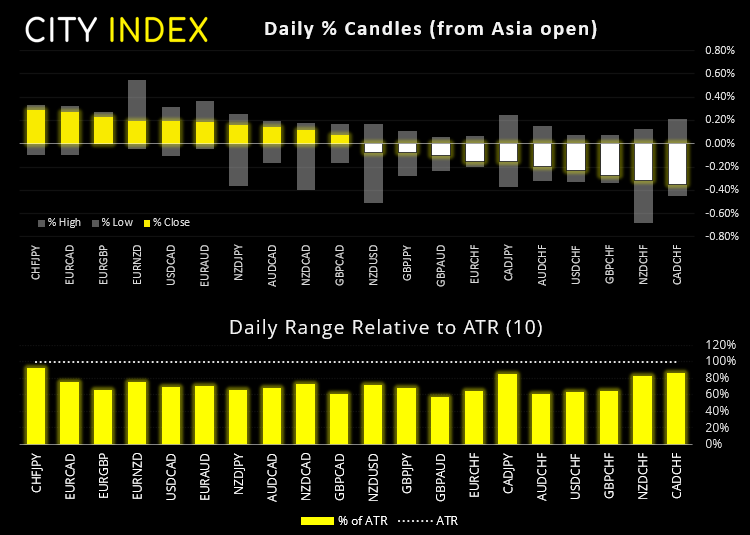

Forex: USD holds onto gains

Overnight moves were corrective in nature (against the prior day’s trends) which allowed the heavily sold New Zealand dollar to lift itself ever so slightly from its lows over the last couple of hours. However, not helping a bullish case whatsoever is news that the outbreak has spread beyond Auckland and entered Wellington, and that new cases has risen to 31. The next days are critical for New Zealand (and therefore NZD) as we’ll find how long lockdowns will inevitably be extended.

The US dollar index traded slightly lower overnight but remains just off of its 9-month high. There’s no major economic data scheduled today for the US, although the Fed’s Kaplan is participating in a Q+A session on “Economic Developments and Implications for Monetary Policy” at 16:00 BST. And that could be a mover for EUR/USD (and the US dollar in general) if more details for tapering are dropped.

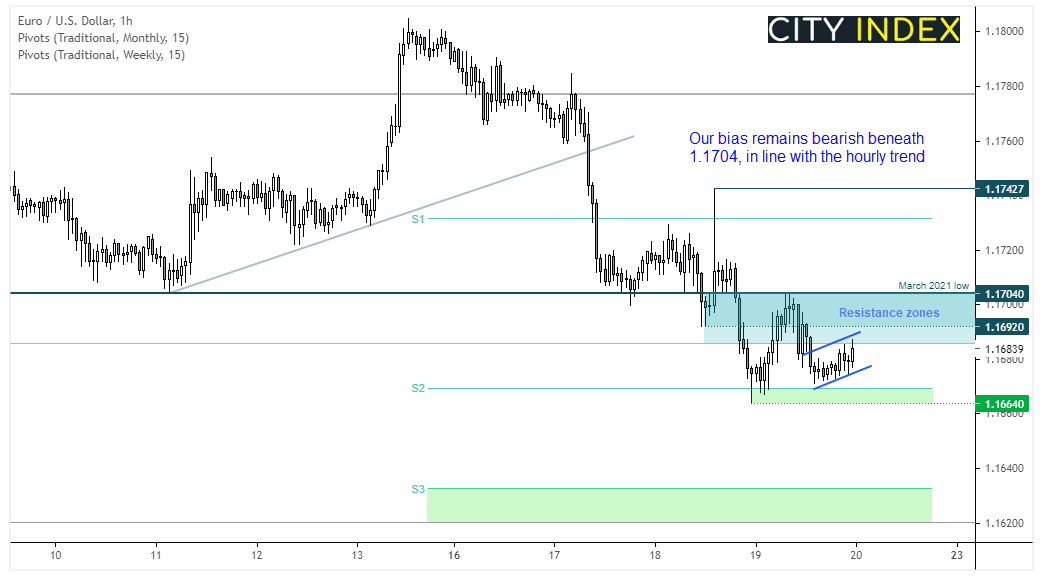

EUR/USD bounced higher from the weekly S2 pivot in line with yesterday’s bias, as part of a countertrend move. Prices then found resistance at the March 2021 low before rolling over once more. The hourly trend remains bearish and prices have been consolidating in a potential bear flag overnight. But from here, our bias remains bearish beneath 1.1704 and for a break to new lows.

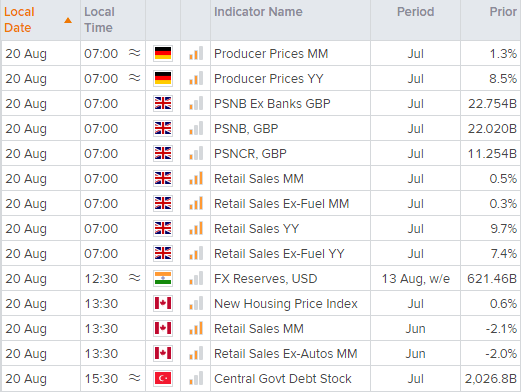

German producer prices are expected to have risen 0.8% in July, down from 1.2% in June, and they are released at 07:00 BST alongside UK retail sales. Given last month’s sales data covered the period where the UK had just re-emerged from lockdown, it’ plausible to expect softer retail sales today. They are forecast to have risen 0.5% m/m compared with 0.5% previously.

Learn how to trade forex

Commodities: Metals bears take a breather

Copper futures have retraced and sits around 3.5c from yesterday’s high. A retracement is likely needed but our bias remains bearish beneath the 4.16 - 4.20 resistance zone.

Gold is holding up to dollar strength quite well and trades in a potential bull flag. Obviously, we’d need to see a weaker dollar for it to stand any chance of breaking higher towards 1800 – 1805 (200-day eMA).

Silver has gapped lower at the open which reinforces our view the corrective high has been seen at 23.95. Our bias remains bearish beneath 24.0.

WTI has seen a minor rebound from its 62.36 low but our bias remains bearish beneath 65.0.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM