Asian Indices:

- Australia's ASX 200 index rose by 39.8 points (0.54%) and currently trades at 7,434.10

- Japan's Nikkei 225 index has risen by 146.49 points (0.53%) and currently trades at 27,979.78

- Hong Kong's Hang Seng index has fallen by -269.49 points (-1.03%) and currently trades at 25,922.83

UK and Europe:

- UK's FTSE 100 futures are currently up 2 points (0.03%), the cash market is currently estimated to open at 7,027.43

- Euro STOXX 50 futures are currently up 0.5 points (0.01%), the cash market is currently estimated to open at 4,103.09

- Germany's DAX futures are currently down -5 points (-0.03%), the cash market is currently estimated to open at 15,613.98

US Futures:

- DJI futures are currently up 82.76 points (0.24%)

- S&P 500 futures are currently down -18.25 points (-0.12%)

- Nasdaq 100 futures are currently down -6.25 points (-0.14%)

Learn how to trade indices

Indices

It was another bearish session for China’s equity markets as Beijing’s crackdown weighed on corporate profit prospects and, therefore, sentiment. The CSI300 fell to a year-to-day low, China’s highly indebted property company Evergrande (3333) sank -11.9% to a 4.5-year low after saying they would cancel a special dividend proposal. Alibaba fell on the Hong Kong stock exchange as regulators improved delivery worker’s protection. The Hang Seng index is on track to close below 26k for the first time since November.

Higher commodity prices helped the ASX 200 rise to a new record high, led by mining and energy stocks. The Nikkei and TOPIX tracked Wall Street higher ahead of today’s earnings, with Visa (V) being one of the major releases today for the US, although nothing is scheduled for the FTSE 350 today.

US futures have opened lower, the FTSE 100 futures contract is 2 points higher to suggest a flat open. The FTSE 100 failed to break above the 50-day eMA yesterday and printed a gravestone Doji. Support remains around 6950 (June low, weekly pivot point) with intraday support around 7,000.

FTSE 350: Market Internals

FTSE 350: 4042.06 (-0.03%) 26 July 2021

- 176 (50.14%) stocks advanced and 151 (43.02%) declined

- 24 stocks rose to a new 52-week high, 3 fell to new lows

- 78.92% of stocks closed above their 200-day average

- 54.99% of stocks closed above their 50-day average

- 19.94% of stocks closed above their 20-day average

Outperformers:

- + 5.43% - Cineworld Group PLC (CINE.L)

- + 5.22% - Trainline PLC (TRNT.L)

- + 4.93% - Tullow Oil PLC (TLW.L)

Underperformers:

- -4.89% - Ultra Electronics Holdings PLC (ULE.L)

- -3.64% - Fidelity China Special Situations PLC (FCSS.L)

- -2.75% - Elementis PLC (ELM.L)

Forex:

Earnings and tomorrow’s FOMC meeting are the main drivers for markets at present. Whilst there are a few data points today (mainly form the US) none of them are likely to be top-tier stuff regarding volatile reactions. US consumer confidence rose to a 16-month high in June, and later today we get to see if the rise on Covid cases has dented its run when it is released at 14:00 BST.

However, another driver to focus on is daily Covid rate for the UK. The British pound has regained some strength after daily new cases of Covid have fallen for 5 consecutive days. Whilst it’s still early days, markets are forward looking and clearly view this small sample size with optimism as GBP was the strongest major yesterday. With data on the light side ahead of tomorrow’s FOMC meeting, then GBP may trade higher still should new cases fall for a sixth consecutive day (figures are released at 16:00 BST).

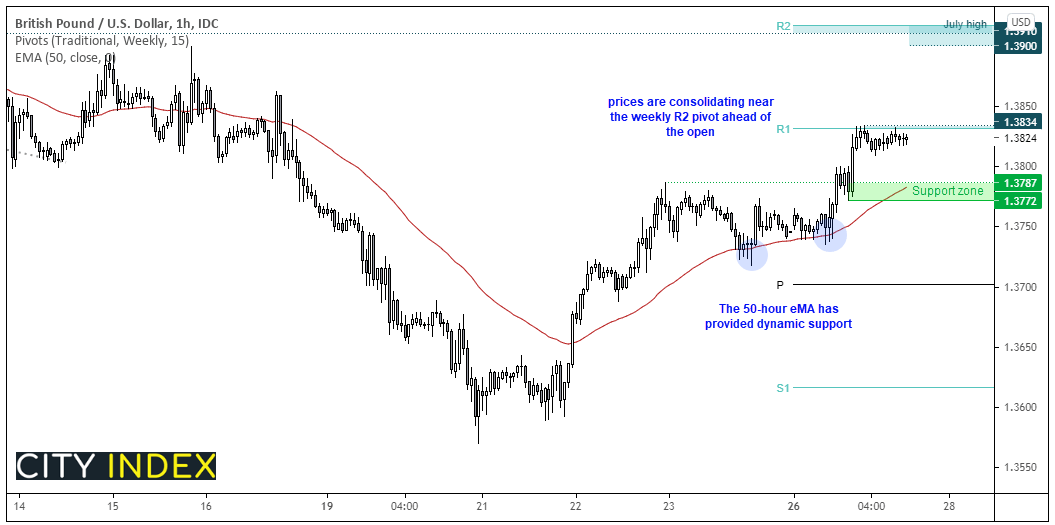

GBP/USD closed to a six-day high yesterday and back above its 10 and 20-day eMA’s. Given its false break below the 200-day eMA last week and subsequent rally, then perhaps we should be on guard for further upside. Especially since the last time it tested the 200-day eMA, its false break marked the beginning of a multi-month rally.

The hourly chart shows a strong bullish trend is developing. It broke above a retracement line yesterday and found resistance at the weekly R1 pivot where it now consolidates. Should prices initially move lower we’d like to see any retracement hold above the 1.3772 low, and a break above yesterday’s highs brings the 1.3900 handle into focus which is just below the weekly R2 pivot and July high.

Learn how to trade forex

Commodities:

Eyes remain firmly fixed on Copper futures after breaking to a 6-week high yesterday and extending gains overnight. As prices are nearing the weekly R2 pivot then perhaps a pullback (or pause) may be on the cards, although we’re looking for prices to hold above 4.4350 support.

WTI formed a bearish outside candle / hanging man yesterday. Whilst the daily trend remains bullish above the $65 low, a break beneath 70.0 warns of a countertrend move. But if prices can hold above 70.0 (where the 50-day eMA and weekly pivot reside) then a break above yesterday’s high assumes bullish continuation.

We’re still looking for silver to top out but suspect we may need to wait for the completion of the FOMC meeting until we get a directional move.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

10.1.1

Latest market news

Today 07:55 AM

Today 04:47 AM

Latest Indices articles

Yesterday 08:00 PM

Yesterday 04:54 PM

April 15, 2024 06:08 AM