Asian Indices:

- Australia's ASX 200 index fell by -43.2 points (-0.63%) to close at 6,783.90

- Japan's Nikkei 225 index has risen by 31.67 points (0.1%) and currently trades at 29,747.54

- Hong Kong's Hang Seng index has fallen by -98.71 points (-0.32%) and currently trades at 29,000.18

UK and Europe:

- UK's FTSE 100 futures are currently down -8 points (-0.12%), the cash market is currently estimated to open at 6,795.61

- Euro STOXX 50 futures are currently down -6 points (-0.16%), the cash market is currently estimated to open at 3,844.96

- Germany's DAX futures are currently down -26 points (-0.18%), the cash market is currently estimated to open at 14,531.58

Tuesday US Close:

- The Dow Jones Industrial fell -127.51 points (-0.39%) to close at 32,825.95

- The S&P 500 index fell -6.23 points (-0.16%) to close at 3,962.71

- The Nasdaq 100 index rose 69.74 points (0.53%) to close at 13,152.28

Index futures point lower

We expect to see stock market indices open slightly lower with futures from Europe and US ticking into the red. Traders are likely squaring up positions ahead of today’s Fed meeting, and we expect volatility to remain on the tame side leading up to it.

It’s sightly mixed in Asia with the ASX 200 and KOSPI 200 in the red whilst shares from Japan and China are slightly higher, but not by a large enough degree to take comfort in. Japan’s exports contracted by -4.5% in February as demand from China and the US fell more than expected. Down from 6.4% in January, they were only expected to contract by -0.8%.

The FTSE 100 closed above 6800 for the first time since the January high. It was also a bullish opening Marabuzo, meaning it opened at the low of the day and traded notably higher. Given prices are now accelerating away form its 10-day eMA, we think it is considering a retest of its YTD high around 6,900.

The Russell 2,000 sent a warning signal when it fell from its highs yesterday, declining -1.7% and being the weakest performer among US major indices. The Dow Jones and S&P 500 also closed lower, whilst the Nasdaq notched up a 0.5% gain despite the 10 and 30-year yields inching their way back to their recent highs.

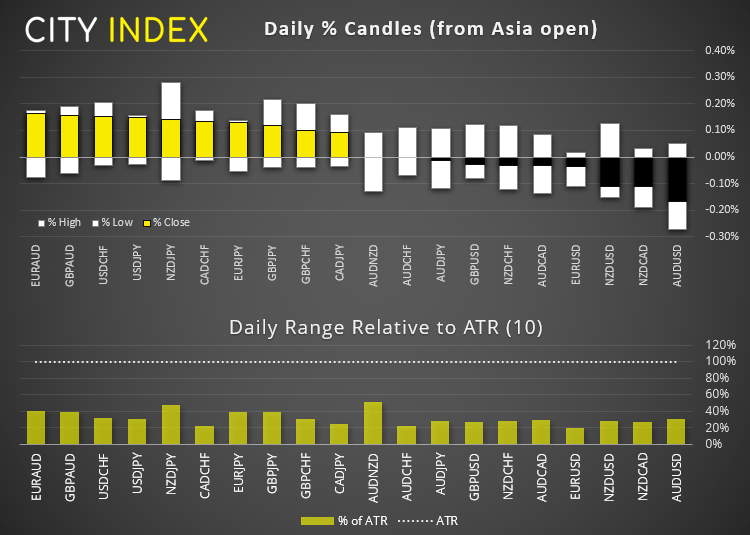

Forex markets in need of a wake-up call

As we can see on the forex dashboard, trading range were razor thin. But at least this leaves plenty of meat on the bone for bursts of volatility near the end of the US session. With any luck, we’ll see some action as the US markets open.

- EUR/USD remains glued to 1.1900 after trading lower for three consecutive sessions. We very much doubt it will still be there this time tomorrow. A stronger dollar could push this to (and potentially beneath) the 1.1836 low after the meeting. Next major resistance for euro remains at 1.2000, which leaves a little more upside potential should the dollar weaken.

- GBP/USD produced a bullish pinbar yesterday, and its low failed to touch 1.3780 support to suggest demand is building. So the pound may be one of the better pairs to take bullish bets against a weaker dollar as, so far, it has held up quite well to dollar strength this week.

- EUR/JPY is retracing from its high after stalling around 130.00. With its daily trend remaining intact, the bias remains bullish overall but will seek for evidence of a swing low to form above 129.00 and for it to eventually hit our 131.00 target.

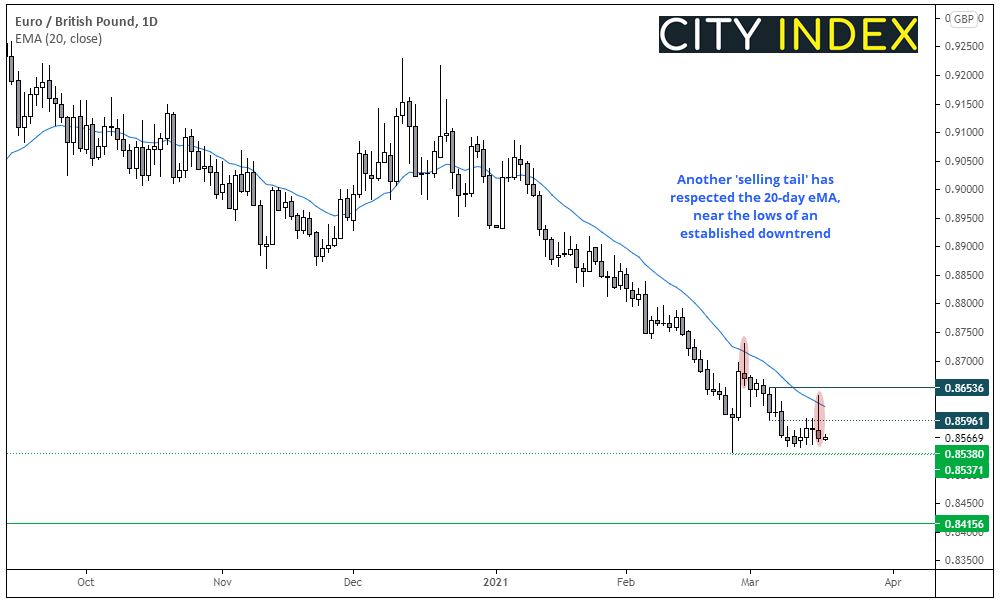

EUR/GBP: Selling tails point to a bearish breakout

The pound has held up quite well against the dollar and the euro, so we suspect EUR/GBP may break to new lows after the FOMC meeting. Although a stronger dollar post-meeting could help EUR/GBP break a lot sooner. Alternatively, a much weaker dollar could see EUR/GBP cycle higher without necessarily breaking its bearish trend.

The daily chart remains within an established downtrend and we suspect its retracement from recent lows is now complete. Yesterday ‘selling tail’ (bearish hammer) found resistance at the 20-day eMA then fell promptly lower. And as this is the second such spike to the 20-day eMA in over two weeks, so we are on guard for a bearish break.

- A break beneath the 0.8537 low assumes bearish continuation.

- The bias remains bearish below 0.8640, although the 0.8560 high can be used to fine-tune risk management.

- The next major support level sits at 0.8415 although bears can also target the 0.8500 and 0.8450 handles.

Commodities: WTI coils at its highs, gold holds below 1740

Gold found resistance at 1740 yesterday, and this level remains pivotal going forward. A break above here brings 1760 resistance into focus, yet we cannot discount the potential for another dip lower as the 20-day average and 1740 cap as resistance, ahead of a USD focussed event tonight. 1700 is the next major support level.

WTI is coiling up within a small symmetrical triangle on the daily chart. The trend suggests an upside break is on the cards, whilst a break below $63 warns of a deeper retracement.

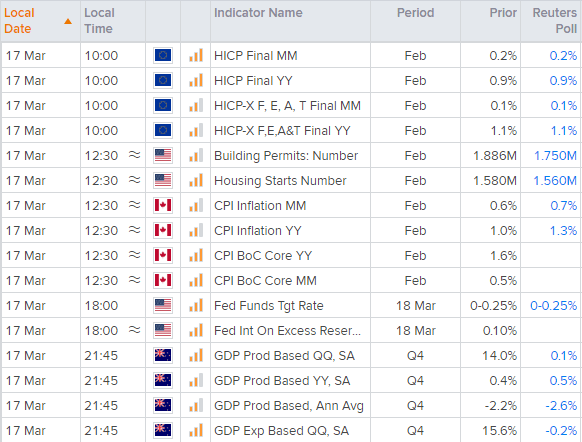

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- As European CPI figures are the final release, they’re unlikely to provide much of a reaction unless they deviate far from expectations (which is unlikely).

- Canadian CPI remains in the lower half of the BOC’s 1-3% band, although they expect it to rise temporarily towards the upper band over the coming months. So, any weakness today could see expectations for this transient inflation pushed further back and weaken CAD, whilst a stronger than expected print could strengthen a (relatively strong) Canadian dollar. Still, the FOMC meeting will be the main event to keep an eye on.

- Naturally, the Fed meeting is the main event. If the Fed raise forecasts and do not mention any concerns over rising bond yields, it could be a strong bullish reaction from the US dollar.

- Q4 GDP puts NZP pairs into focus. What we would like to see (from a trader’s perspective) is for a divergent theme between the FOMC meeting and NZ GDP (such as weak GDP coupled with bullish dollar following the meeting, or visa-versa).

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM