Asian Indices:

- Australia's ASX 200 index rose by 84.4 points (1.16%) and currently trades at 7,336.60

- Japan's Nikkei 225 index has fallen by -180.31 points (-0.65%) and currently trades at 27,472.43

- Hong Kong's Hang Seng index has fallen by -68.69 points (-0.25%) and currently trades at 27,190.56

UK and Europe:

- UK's FTSE 100 futures are currently up 11 points (0.16%), the cash market is currently estimated to open at 6,892.13

- Euro STOXX 50 futures are currently up 2.5 points (0.06%), the cash market is currently estimated to open at 3,958.84

- Germany's DAX futures are currently up 18 points (0.12%), the cash market is currently estimated to open at 15,234.27

US Futures:

- DJI futures are currently down -725.81 points (-2.09%)

- S&P 500 futures are currently down -23.5 points (-0.16%)

- Nasdaq 100 futures are currently down -2.5 points (-0.06%)

Learn how to trade indices

Can indices sustain Tuesday’s rebound?

Japan’s share market was broadly higher and led by small caps, thanks to a rebound on Wall Street and strong export data in Japan. The ASX 200 was a strong performer, rising 1.2% after weak retail sales confirms the RBA’s dovish stance.

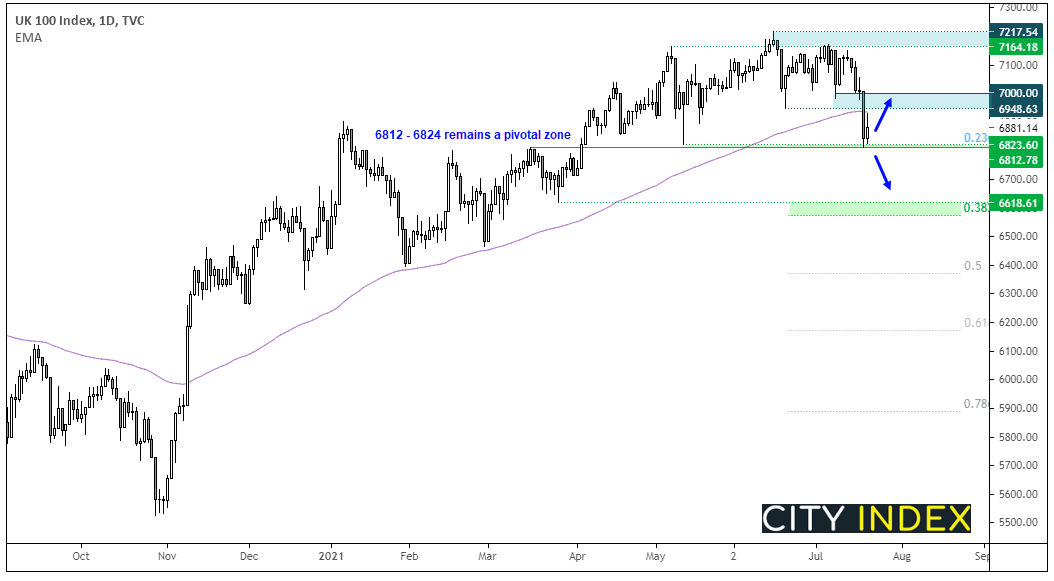

US futures are a touch lower at the open although European futures are pointing towards a slightly higher open. FTSE 100 futures are 10 points higher (+0.15%) and suggest the cash market to open around 6891.

As we discuss on today’s video, the jury is still out as to whether yesterday’s ‘rally’ on Wall Street marks the end of a correction or whether it is a prelude to the next leg lower. The FTSE 100 is no exception.

Monday’s sell-off stalled at pivotal zone (an area which has provided both support and resistance) where the 23.6% Fibonacci also resides. And whilst it closed higher on Tuesday, the 100-day eMA capped as resistance, and it remains 119 points below 7,000. Both the mentioned support and resistance levels carry some significance with them, so the FTSE finds itself between a rock and a hard place between the 6800 – 7000 area. So, until either one of those levels breaks, range-trading strategies are preferred and the 6812 – 6824 support zone is a key focal point for today’s session.

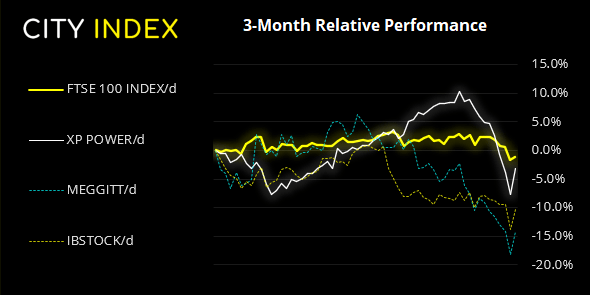

FTSE 350: Market Internals

FTSE 350: 3948.19 (0.54%) 20 July 2021

- 258 (73.50%) stocks advanced and 83 (23.65%) declined

- 4 stocks rose to a new 52-week high, 16 fell to new lows

- 69.23% of stocks closed above their 200-day average

- 4.56% of stocks closed above their 20-day average

Outperformers:

- + 5.04% - XP Power Ltd (XPP.L)

- + 4.91% - Meggitt PLC (MGGT.L)

- + 4.10% - Ibstock PLC (IBST.L)

Underperformers:

- -4.94% - Hochschild Mining PLC (HOCM.L)

- -4.82% - Just Eat Takeaway.com NV (TKWY.AS)

- -3.00% - Fresnillo PLC (FRES.L)

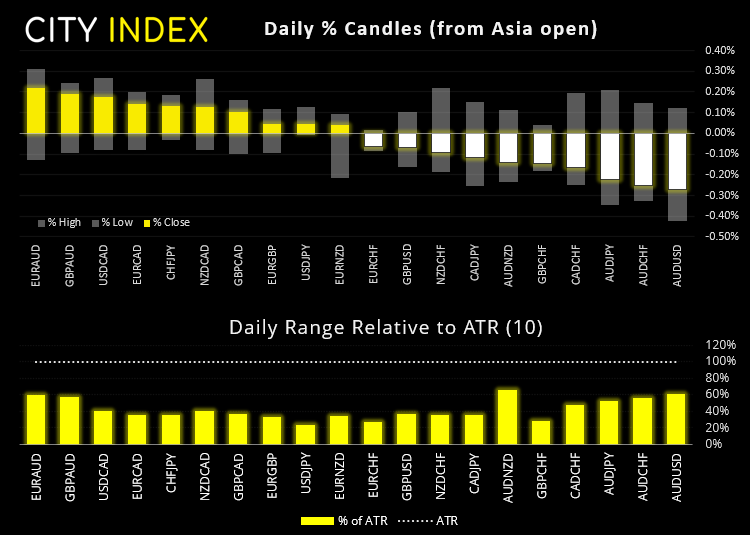

Forex: Retail sales and covid weigh on AUD

The Australian dollar was broadly lower that’s to rising coronavirus cases and weaker-than-expected retail sales. With lockdowns setting the stage for a -0.6% decline, the -1.8% contraction in June took some by surprise as the June figures mostly contain details from Victoria. And with lockdowns across New South Wales likely to be extended (due to rising cases) then is does not bode well for July’s retail sales either.

Japan’s exports beat expectations in June, thanks to car demand from the US and chip-making equipment set for China. Rising 48.6% YoY, it’s the second highest reading in 40 years.

A strong trend is developing on EUR/AUD ahead of tomorrow’s ECB meeting. Its just off its year-to-date highs and consolidating in a potential continuation pattern. Should prices retrace we’d be interested in bullish setups around the 1.5950 – 1.6000 area, unless it breaks to new high first.

The US dollar was little changed overnight, and with a light calendar and ECB meeting tomorrow we may be in for a quieter session unless we are treated to some equity/bond fireworks.

Learn how to trade forex

Commodities look for direction from a sideways dollar:

WTI futures printed a small bullish hammer around trend support and the 100-day eMA. We see the potential for a sympathy bounce but, given the magnitude of Monday’s -7% decline we cannot rule out new lows further out. With a lack of economic news and a ranging US dollar then traders may want to remain nimble and not ‘marry’ positions.

Silver remains just below $25 and touched a fresh 3-month low but, very much like yesterday’s European open report, the lack of selling pressure could leave it vulnerable to a bounce and break its 3-day losing streak. Overall, we remain bearish below 25.52 resistance.

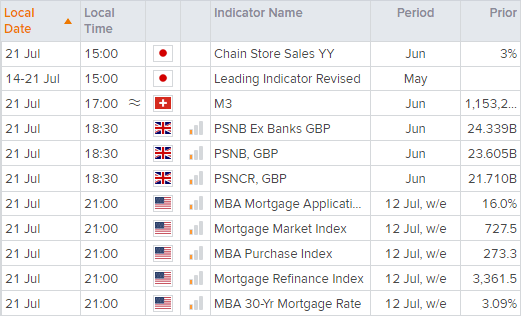

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

10.1.1

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM