Asian Indices:

- Australia's ASX 200 index rose by 22.6 points (0.3%) and currently trades at 7,512.50

- Japan's Nikkei 225 index has risen by 262.72 points (0.96%) and currently trades at 27,756.96

- Hong Kong's Hang Seng index has risen by 392.16 points (1.56%) and currently trades at 25,501.75

UK and Europe:

- UK's FTSE 100 futures are currently up 15 points (0.21%), the cash market is currently estimated to open at 7,124.02

- Euro STOXX 50 futures are currently up 8.5 points (0.2%), the cash market is currently estimated to open at 4,184.92

- Germany's DAX futures are currently up 24 points (0.15%), the cash market is currently estimated to open at 15,876.79

US Futures:

- DJI futures are currently up 215.63 points (0.61%)

- S&P 500 futures are currently up 20.75 points (0.14%)

- Nasdaq 100 futures are currently up 7.5 points (0.17%)

Learn how to trade indices

Asian markets trade higher

Asian equity markets tracked Wall Street higher, led by the Hang Seng Enterprise (2.1%) and Hang Seng Index (1.7%). China’s A50 market rose 0.3%, whilst Japan’s TOPIX and Nikkei 225 rose around 1%. The ASX 200 traded cautiously higher but lacks the bullish momentum of its US counterparts, although it is currently on track to close back above 7500. Travel stocks were strong performers as the government backed plans to reopen.

The FTSE 100 rallied almost immediately from the open to yesterday’s upper 7150 target, before handing back early gains and forming a potential bearish hammer on the daily chart. Given last week’s break of the July trendline, we could still see a new low on the FTSE, so a break beneath yesterday’s low (which also takes it back beneath 7100) spells trouble for bulls over the near-term.

FTSE 350: Market Internals

FTSE 350: 4107.01 (0.24%) 24 August 2021

- 178 (50.1%) stocks advanced and 154 (44.0%) declined

- 178 stocks rose to a new 52-week high, 0 fell to new lows

- 71.23% of stocks closed above their 200-day average

- 63.53% of stocks closed above their 50-day average

- 20.8% of stocks closed above their 20-day average

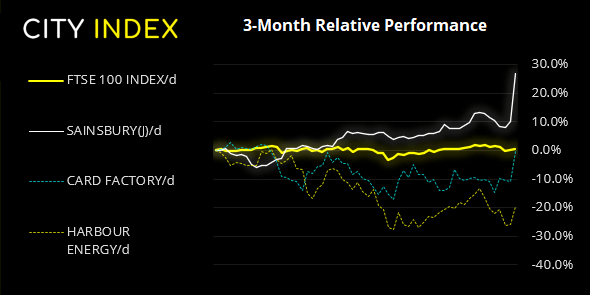

Outperformers:

- + 15.3% - J Sainsbury (SBRY.L)

- + 12.0% - Card Factory PLC (CARDC.L)

- + 8.33% - Harbour Energy PLC (HBR.L)

Underperformers:

- - 4.89% - Workspace Group PLC (WKPL.L)

- - 3.35% - Pennon Group PLC (PNN.L)

- - 3.03% - BT Group PLC (BT.L)

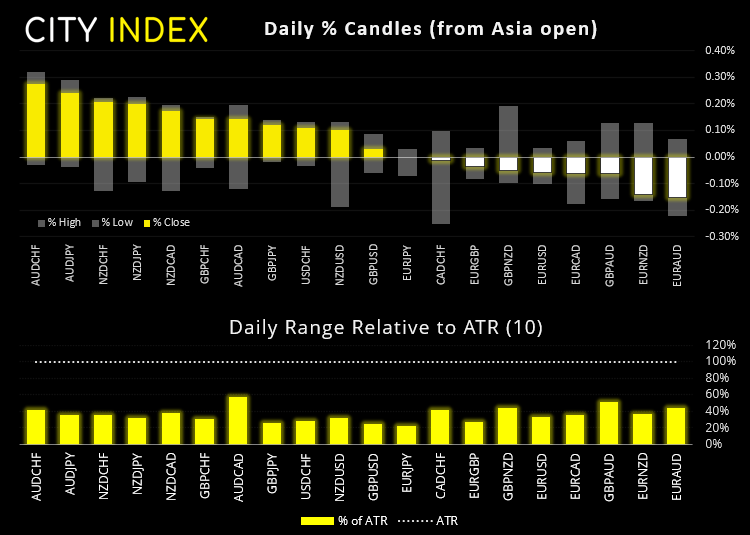

Forex: AUD and NZD take the lead

The US dollar index (DXY) remained near yesterday’s lows after weak PMI’s pushed back expectations that Jerome Powell would announce tapering at this week’s Jackson Hole symposium. Coupled with good vaccine news, it continued to benefit risker currencies overnight such as AUD and NZD which are the strongest FX majors of the day. AUD/USD sits just beneath the November 16th low but formed a 3-bar bullish reversal (Moring Star).

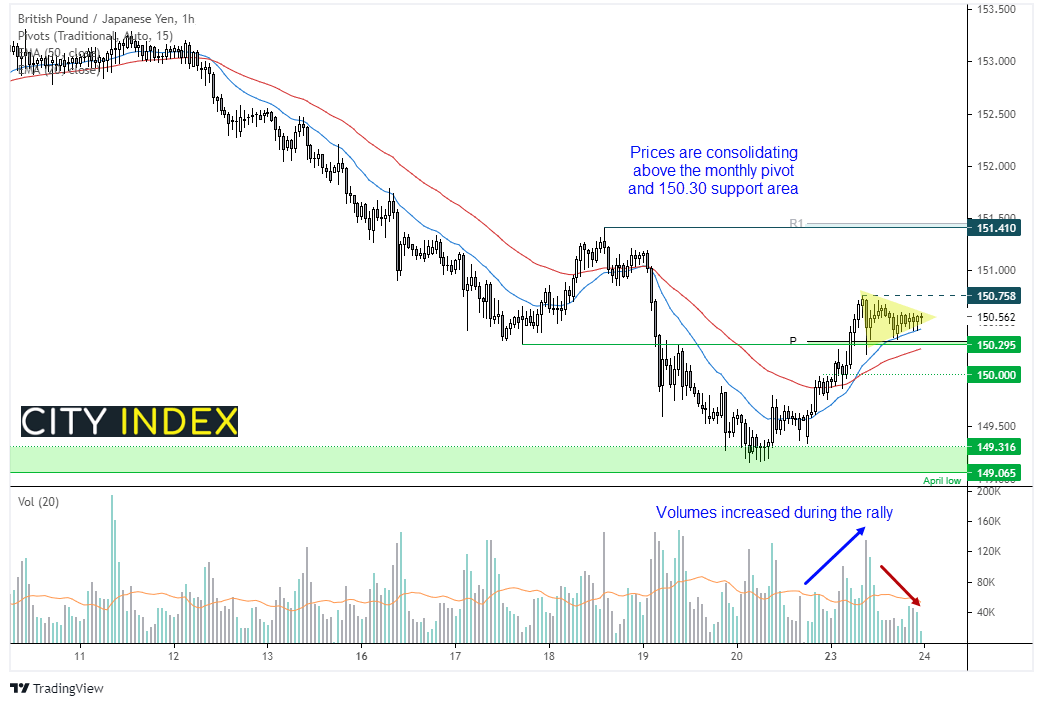

GBP/JPY broke above 150 yesterday and, within a few hours after the open, reached our 150.30 target. Given the risk-on tone across markets in general, we’re now looking for prices to once again break higher from compression as part of a countertrend move against recent yen strength.

We can see on the hourly chart that volumes were rising during the recent rally, and have declined overall during its consolidation, suggesting this is part of retracement. The 20-hour eMA has crossed above the 50-hour eMA and continues to support prices, and the consolidation has held above the monthly pivot point.

We always allow for some volatility around the open, so will retain a bullish bias if we see any ‘buying tails’ (low wicks) which close back above the monthly pivot. And a break either out of the pennant or a break above the 150.75 high could assume bullish continuation, with 151 being an interim target on the way to the 151.40 highs were the monthly S1 resides.

Learn how to trade forex

Commodities:

Oil prices continued to climb overnight after breaking a 7-day losing streak yesterday. Hopes for increased demand have returned since the FDA fully approved the Pfizer-BioNTech vaccine, which paves the way for rivals to also get the all-clear and help speed up the economic recovery.

Gold prices are consolidating into a potential bull-flag on the four-hour chart after breaking out of a (larger) bull-flag yesterday. A convincing break above yesterday’s highs clears the 200-day eMA and monthly pivot and assumes bullish continuation.

Silver rose to a 3-day high after finding support around 23.0 and now shows the potential to retest 24.0. Yet out of the two gold has the stronger bullish structure on the daily chart.

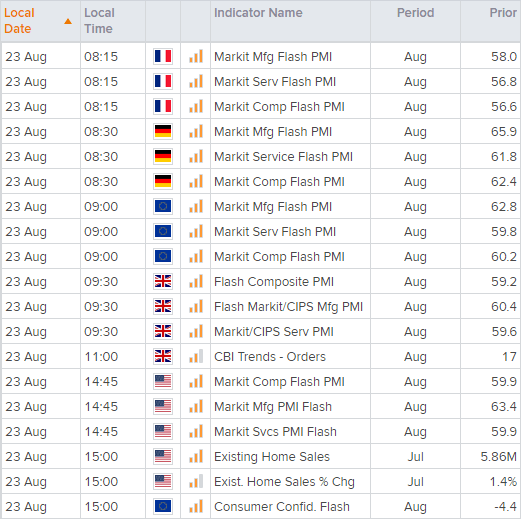

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM