Asian Indices:

- Australia's ASX 200 index rose by 53.5 points (0.74%) and currently trades at 7,327.30

- Japan's Nikkei 225 index has fallen by -1533.07 points (-0.51%) and currently trades at 29,686.68

- Hong Kong's Hang Seng index has risen by 122.4 points (0.51%) and currently trades at 24,221.54

UK and Europe:

- UK's FTSE 100 futures are currently up 14.5 points (0.21%), the cash market is currently estimated to open at 6,995.48

- Euro STOXX 50 futures are currently up 9.5 points (0.23%), the cash market is currently estimated to open at 4,107.01

- Germany's DAX futures are currently up 44 points (0.29%), the cash market is currently estimated to open at 15,392.53

US Futures:

- DJI futures are currently down -50.63 points (-0.15%)

- S&P 500 futures are currently up 10 points (0.07%)

- Nasdaq 100 futures are currently up 6.5 points (0.15%)

Learn how to trade indices

Indices

Eyes remained on Evergrande today to see how the saga would be dealt with (if at all) now China’s public holiday was over. Whilst it remained up for debate as to whether Beijing would step in, that question was answered with $120 billion cash injection into the markets. Sentiment was also lifted on news that Hengda Real Estate (Evergrande’s main unit) would fulfil its bond coupon payment which is due tomorrow. It’s a shame Hong Kong’s stock markets are closed as this would have likely lifted Evergrande’s stock (3333.HK) from its 11-year low, although it did allow competitors from the property sector across Asia to rally up to 10% after the open today. The ASX 200 rose 0.85% at time of writing and the Hang Seng is up around 0.2%. Shares across Japan were lower ahead of the Ed meeting.

The FTSE 100 retested 7,000 yesterday after gapping higher at the open and holding into earlier gains. As there was little trading activity between 6910 – 6964 then a break back into this range could see a quick move lower as the gap gets filled. But, if the FTSE can hold above yesterday’s gap then eyes are on a potential break above yesterday’s high of 7004 to resume yesterday’s bullish move.

FTSE 350: Market Internals

FTSE 350: 4042.43 (1.12%) 21 September 2021

- 256 (72.93%) stocks advanced and 83 (23.65%) declined

- 9 stocks rose to a new 52-week high, 10 fell to new lows

- 68.09% of stocks closed above their 200-day average

- 48.72% of stocks closed above their 50-day average

- 13.96% of stocks closed above their 20-day average

Outperformers:

- + 18.04% - Entain PLC (ENT.L)

- + 7.62% - National Express Group PLC (NEX.L)

- + 6.36% - 888 Holdings PLC (888.L)

Underperformers:

- -4.92% - Kingfisher PLC (KGF.L)

- -2.60% - Discoverie Group PLC (DSCV.L)

- -2.22% - Compass Group PLC (CPG.L)

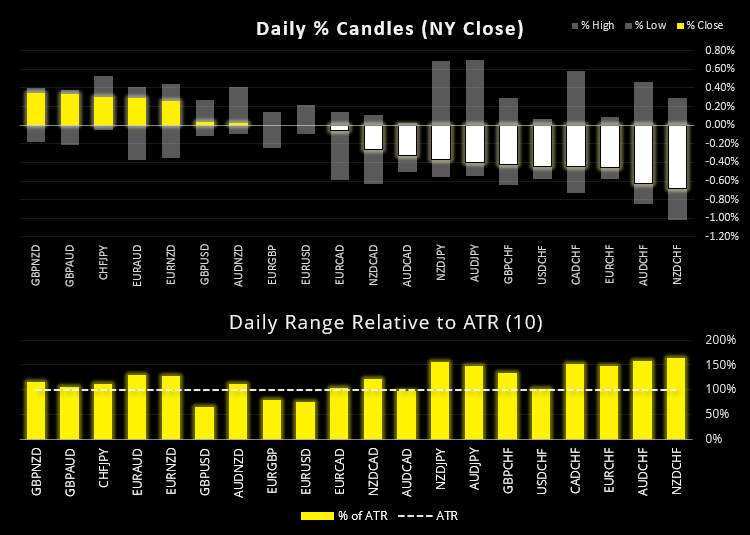

Forex:

Today’s main event is the conclusion of the FOMC meeting, which begins with the official cash rate being delivered at 19:00 BST (with no expectations of any change being made). At 19:30 Jerome Powell will hold the press conference, and it is here that traders will listen for any clues (or confirmation) that tapering will begin. There have been some speculation that the Fed may delay such an announcement due to the selloff in equities (as whopping -5%...), although a mere mention that tapering is in the pipeline would strongly suggest it may be announced at their November meeting.

Eyes will also be on the dot plot to see if there is an expectation for the Fed to raise rates before 2023, or upgrade their growth, inflation (or reduce) unemployment forecasts to underscore a stronger economy.

GBP/JPY is holding above the 149 support cluster, so the potential for a bounce remains should European markets take relief from the Evergrande news. A more dovish-than expected Fed would also likely be supportive of GBP. But as outlined in today’s Asian Open report, a break beneath the March low could open up for the floor for bears on GBP/JPY.

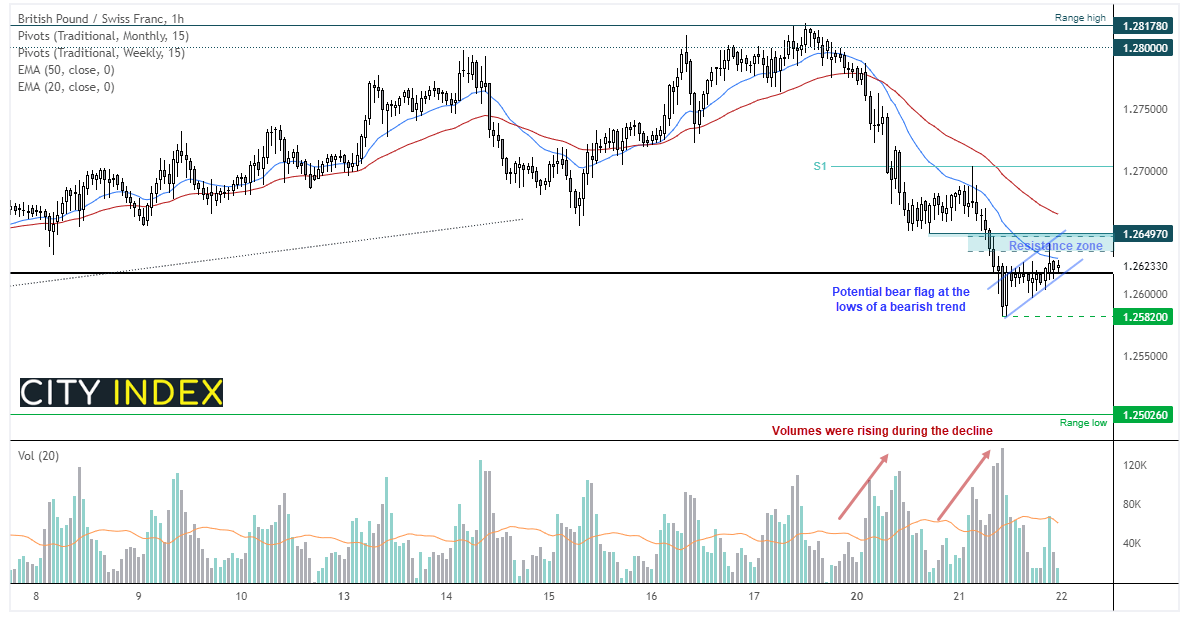

Another risk pair for pound traders to consider is GBP/CHF, although we’ll drop to the 1-hour timeframe. The pair fell nearly -2% over two days since rolling over at the top of the 1.250 – 1.2800 range, allowing a nice bearish trend has formed. The 20-hour and 50% retracement level is capping as resistance, and our bias remains bearish below 1.2650. Its hovering around the monthly pivot point and forming flag, which would be confirmed with a break of yesterday’s low.

Learn how to trade forex

Commodities:

WTI has gapped higher overnight and looks set to test yesterday’s high. A break above it confirms yesterday’s Doji as a swing low and could be part of its next leg higher.

Gold has broken out of a bull flag on the hourly chart and prices are now probing 1780 resistance. The trend structure is firmly bullish and a potential higher low has formed around 1770.

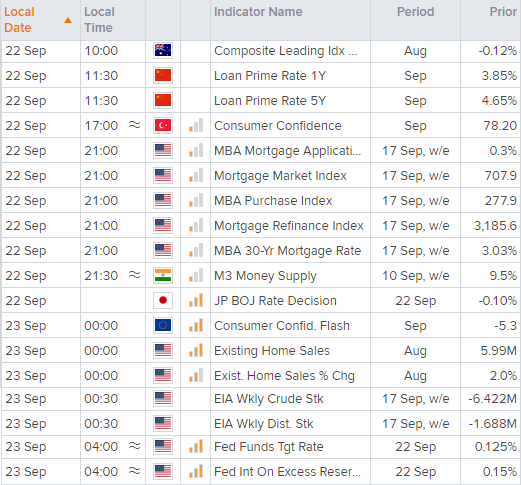

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM