Indices mostly higher in Asia (barring Japan)

It was a strong close for the Australian share market with consumer sentiment jumping to an 11-year high. Looking past a slow vaccination rollout (not that it seems too urgent with such low cases anyway…), consumer have an optimistic outlook on family finances and the economy according to the Westpac-Melbourne institute survey.

Yet that weas clearly not the case in Japan as machinery orders unexpectedly plummeted, dashing hopes of an investment-led recovery. Machinery orders contracted -7.1% YoY in February, down from 1.5% in January, and orders contracted -8.5% MoM verses -4.5% prior. Equity makers in Japan were broadly lower with the TOPIX and Nikkei 225 falling -0.5% at one stage, helped lower by a stronger yen which saw USD/JPY hit a three-week low and fall beneath 109.00.

The FTSE 100 was effectively flat yesterday’s the close, following a bad start as oil stocks and soft GDP data initially sent it lower. Yet it recovered later in the session and closed the day with a bullish pinbar above its 10-day eMA. Looking at the four-hour chart shows a double bottom at 6853 which shows upside potential, although we’d now like to see prices recover above the January high of 6903 if it is to stand any chance of new highs today.

Learn how to trade indices

FTSE 100: Market Internals

FTSE 100: 6890.49 (0.02%) 13 April 2021

- 55 (54.5%) stocks advanced and 43 (42.5%) declined

- 86.14% of stocks closed above their 200-day average

- 85.24% of stocks closed above their 50-day average

- 83.17% of stocks closed above their 20-day average

- 3 hit a new 52-week high, 0 hit a new 52-week low

Outperformers

- + 5.11% - Just East Takeaway (JET.L)

- + 2.43% - Polymetal International (POLY.L)

- + 2.18% - Autotrader Group (AUTO.L)

Underperformers:

- 5.11% - United Utilities Group (UU.L)

- 2.43% - Severn Trent (SVT.L)

- 2.18% - Lloyd Banking Group (LLOY.L)

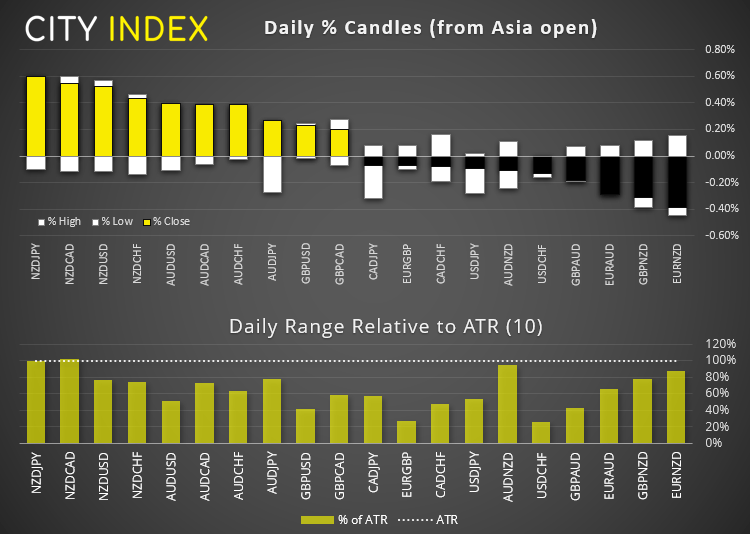

Forex: RBNZ hold rates, dollar on the back ropes

NZD is the strongest major after RBNZ held interest rates at record lows. Whilst they hinted that lower rates are still possible, they have hopes that the trans-Tasman bubble between Australian and New Zealand should support income and employment, which removes any immediate fears of a rate cut.

- The US dollar index (DXY) edge lower overnight to print a fresh three-week low. It’s a touch below its 50-day eMA but trying to build support above the 23rd March low. We see the potential for a minor bounce from current levels, and bears may seek to fade into minor rallies below 92.00 resistance and its 200-day eMA on the four-hour chart.

- EUR/USD has nudged its way to a new cycle high overnight and 1.2000 appears within reach (which is just 35 pips at the time of writing). Today’s bias remains bullish above last week’s high of 1.1928.

- USD/CAD keeps on struggling around its 50-day eMA and bears appear to have the upper hand once more. If prices can break and hold beneath 1.5230 then perhaps our bearish bias will finally come to fruition.

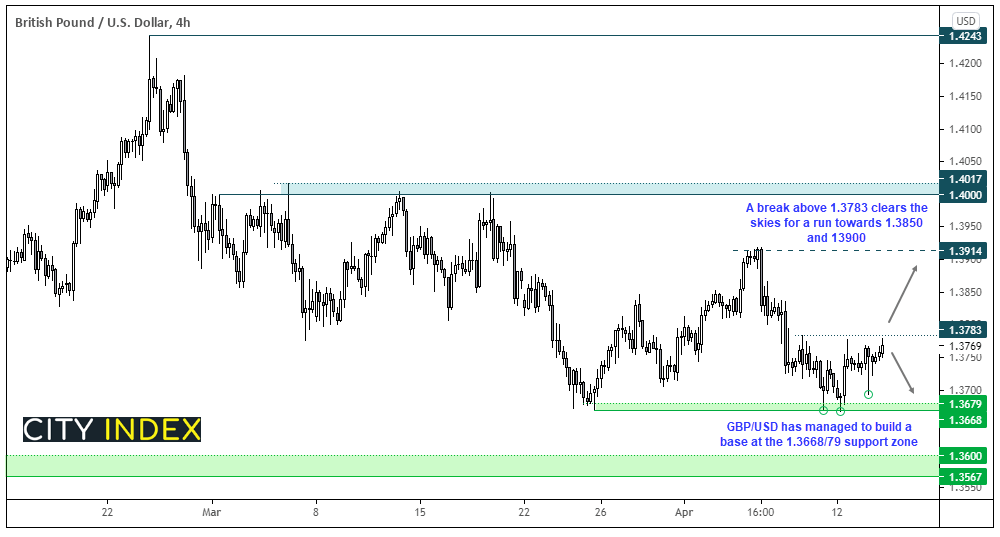

GBP/USD is slowly making bullish progress after finding support at 1.3670. Whilst price action continues to look corrective on the daily chart, it appears demand is slowly building on the intraday timeframes. The four-hour chart shows two ‘buying tails’, with the latter being a higher low. It has drifted into resistance ahead of the open, so 1.3783 may provide interim resistance for range traders, but a break above this level clears the skies for a potential run towards 1.3850 and 1.3900.

- 1.3783 is a pivotal level going into the next session.

- A break above it brings 1.3850 and potentially 1.3900 into focus, but any reversal pattern below it could see it headed back towards range lows.

- A break below 1.3668 brings the support zone around 1.3600 into focus.

Learn how to trade forex

Commodities: Oil ready to wake up?

WTI futures are back above $60 and gapped up at the open. Now nearing the top third of its 57.25 – 62.27 range, a break above yesterday’s high brings the top of its range into focus.

Platinum futures closed below trend support outlined in yesterday’s video. If our bias is correct, price are still within a corrective phase from its February high and could be headed for 1100, or even 1000. This bias remains whilst prices remain beneath 1250.

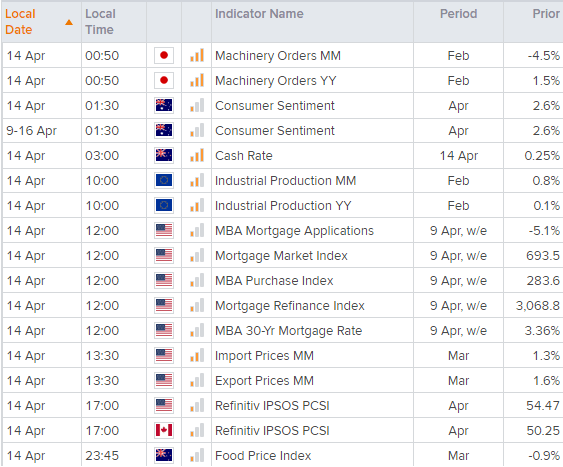

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM