Asian Indices:

- Australia's ASX 200 index rose by 16 points (0.23%) and currently trades at 7,046.30

- Japan's Nikkei 225 index has risen by 135.67 points (0.49%) and currently trades at 28,456.63

- Hong Kong's Hang Seng index has fallen by -105.42 points (-0.37%) and currently trades at 28,353.02

UK and Europe:

- UK's FTSE 100 futures are currently up 19 points (0.27%), the cash market is currently estimated to open at 7,037.05

- Euro STOXX 50 futures are currently up 9 points (0.22%), the cash market is currently estimated to open at 4,034.78

- Germany's DAX futures are currently up 32 points (0.21%), the cash market is currently estimated to open at 15,469.51

Friday US Close:

- DJI futures are currently up 137 points (0.4%), the cash market is currently estimated to open at 34,221.15

- S&P 500 futures are currently up 15.5 points (0.12%), the cash market is currently estimated to open at 4,171.36

- Nasdaq 100 futures are currently up 11.75 points (0.28%), the cash market is currently estimated to open at 13,423.49

Learn how to trade indices

Public holidays across Europe and Canada

We could be in for a quiet day for equities as Germany, France, Switzerland and Canada are on a public holiday. So, traders will have to focus on UK and US stocks whilst keeping in mind we are approaching the month end, so flows can make price action fickle anyway (in a month which has essentially flat, yet choppy, regardless.

Like its European and US peers, the FTSE 100 has lacked overall direction on the weekly charts these past two weeks, and whilst it has closed above 7,000 both weeks, it was just -25 points by Friday. Yet we have seen prices ricochet between sub-6900 and just shy of 7200. The daily chart managed to close above its 10-day eMA on Thursday and Friday (but only just) and prices remains inside Wednesday’s bearish range. So, until momentum tips its hand, traders would be wise to remain nimble and trade around key levels and within ranges. Today’s support zones are 6988 – 7,000 and 6900 – 6920, whilst its next resistance zone is 7067 – 7100.

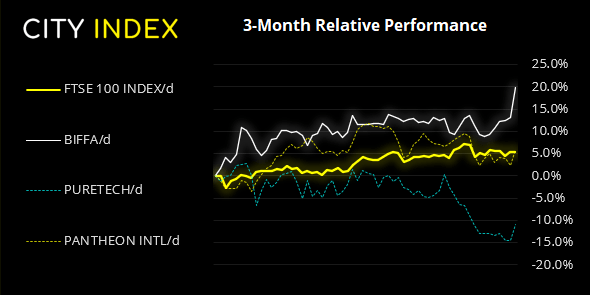

FTSE 350: Market Internals

FTSE 350: 7018.05 (-0.02%) 21 May 2021

- 168 (47.86%) stocks advanced and 169 (48.15%) declined

- 27 stocks rose to a new 52-week high, 3 fell to new lows

- 83.48% of stocks closed above their 200-day average

- 16.81% of stocks closed above their 20-day average

Outperformers:

- + 5.96% - Biffa PLC (BIFF.L)

- + 4.10% - PureTech Health PLC (PRTC.L)

- + 3.54% - Pantheon International PLC (PANI.L)

Underperformers:

- -8.35% - Diversified Energy Company PLC (DEC.L)

- -4.36% - Kingfisher PLC (KGF.L)

- -4.32% - Trainline PLC (TRNT.L)

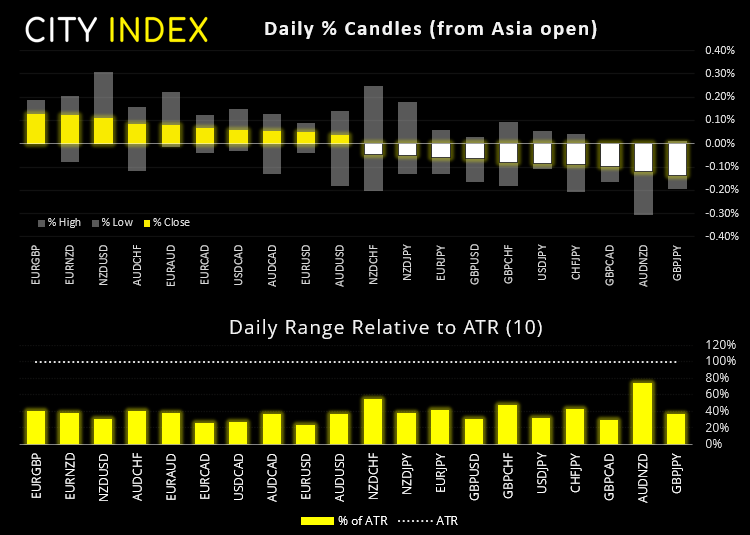

Forex: CAD on track for currency of the month

Month to date, CAD (3.4%), GBP (1.9%) and CHF (1.7%) are the strongest currencies, JPY (-0.9%), NZD (-0.4%) and AUD (-0.27%) are the weakest. Ranges were so tight overnight that they are not worth noting and, with a quiet calendar for today, we could be in for a quitter than usual Monday unless a fresh catalyst comes along.

EUR/AUD hit our initial target on Friday (just below the 1.5800 handle) yet a quick reversal saw it also test (and penetrate) key support around the 1.5700 breakout level. Our bias remain bullish above this level yet the double top just below 1.5800 is a cause for concern over the near-tern. Hopefully volatility can subside and a new level of support found above 1.5700.

NZD/JPY is approaching 77.90 support to consider a bearish breakout in line with our bias. The break of its daily trendline warned us about a potential reversal last week, so now we need a ‘risk-off’ catalyst to push it markedly lower.

GBP/JPY broke to a two-day on Friday in line with our bullish bias yet failed to break above the 154.84 high. Technically the cross remains in a sideways range but our bias remains bullish above 153.40.

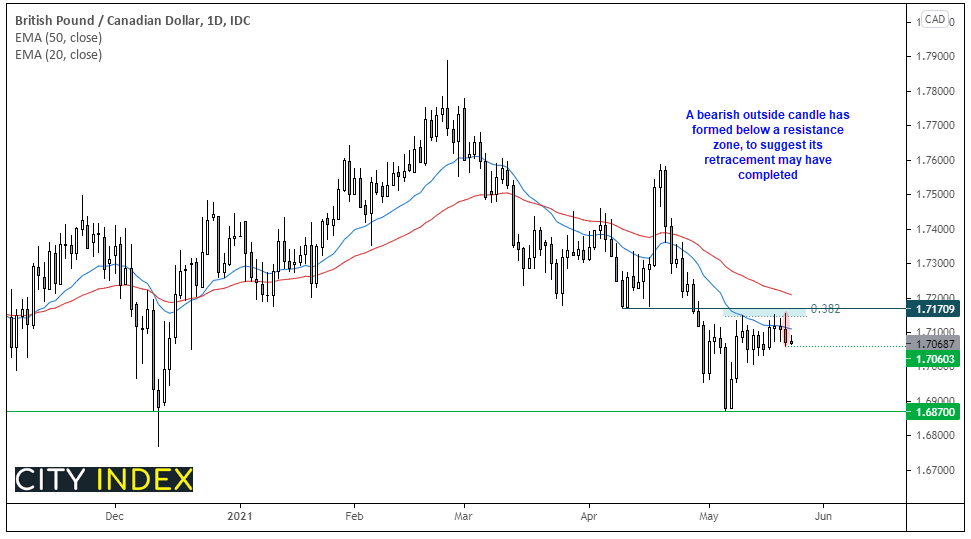

We’re keeping an eye on GBP/CAD for a potential short. The daily trend remains in a downtrend, although a steady retracement has materialised over the past two weeks since reaching its cycle low in May. The 20-day eMA has capped as resistance on a daily close basis, although several intraday highs have tried (yet failed) to hold above it. And the 38.2% Fibonacci ratio has also capped as resistance which paces a resistance zone around 1.7150/70. Moreover, a bearish engulfing candle formed on Friday to suggest momentum may be ready to realign with its dominant bearish trend.

- A break of Friday’s low assumes bearish continuation.

- Our bias remains bearish beneath the 1.7170 high.

- The initial target is around the 1.6900, which is just above historical support at 1.6870.

Learn how to trade forex

China crackdown o commodity prices weighs on base metals:

Copper was down -0.3% overnight and touched a fresh three-week low overnight as China warned domestic commodity companies to not drive-up prices on Sunday. Copper futures tested the 4.4350 low, but a key level that bulls need to defend is the 4.3755 high in late February. Technically and fundamentally we see this as part of a much needed correction and our core view remains bullish overall.

Oil prices moved higher overnight after doubts continued to grow over the Iran nuclear deal being reimplemented. WTI ow trades just above $64 and brent at $66.86, having found support at 64.64 on Friday with a bullish hammer.

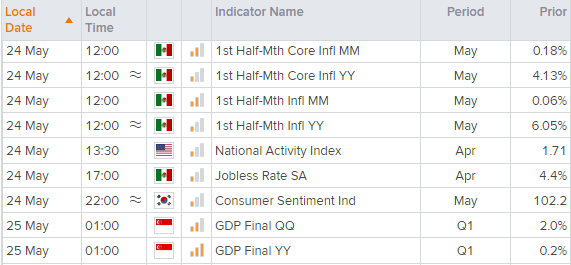

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM