Asian Indices:

- Australia's ASX 200 index fell by -3.3 points (-0.05%) and currently trades at 7,111.90

- Japan's Nikkei 225 index has risen by 87.21 points (0.31%) and currently trades at 28,641.19

- Hong Kong's Hang Seng index has risen by 206.32 points (0.71%) and currently trades at 29,117.18

UK and Europe:

- UK's FTSE 100 futures are currently down -1.5 points (-0.02%), the cash market is currently estimated to open at 7,028.29

- Euro STOXX 50 futures are currently up 15 points (0.37%), the cash market is currently estimated to open at 4,051.04

- Germany's DAX futures are currently up 65 points (0.42%), the cash market is currently estimated to open at 15,530.09

Tuesday US Close:

- DJI futures are currently up 87 points (0.25%), the cash market is currently estimated to open at 34,399.46

- S&P 500 futures are currently up 52.5 points (0.38%), the cash market is currently estimated to open at 4,240.63

- Nasdaq 100 futures are currently up 12.5 points (0.3%), the cash market is currently estimated to open at 13,670.23

Learn how to trade indices

Asian indices higher on Fed comments

Equites across Asia were higher overnight after the Fed’s Clarida said the Fed could limit inflation without knocking the economic recovery off track. Although Austria’s ASX 200 is down as COVID-19 cases are beginning to rise again in Melbourne, with the next 4 hours deemed as “critical” for what new measures may be implemented.

The Euro STOX 50 formed a small bearish pinbar after failing to hold above its prior record high. Given this month has been choppy at best and we are now approaching month end flows, its not impossible to envisage a scenario where prices move lower from current levels as they have twice already this month.

The FTSE 100 closed above its 20-day eMA for a fourth consecutive session yesterday, yet was down by -0.31% by the close and at the lows of its day. Whilst the converging trendlines are not textbook perfect, the potential for a triangle to form remains apparent, so we could see prices dip lower yet hold above the 6897 low (or even 6900) before recycling higher if a triangle is indeed forming on the daily chart.

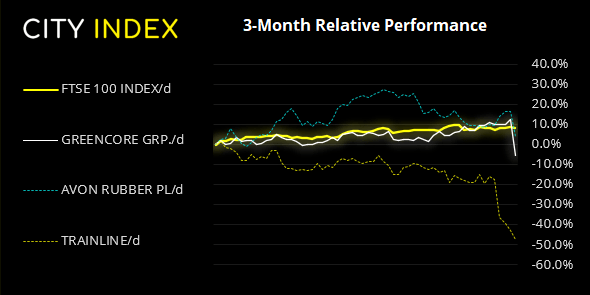

FTSE 350: Market Internals

FTSE 350: 7029.79 (-0.31%) 25 May 2021

- 138 (39.32%) stocks advanced and 194 (55.27%) declined

- 21 stocks rose to a new 52-week high, 2 fell to new lows

- 84.33% of stocks closed above their 200-day average

- 19.37% of stocks closed above their 20-day average

Outperformers:

- + 6.58% - Royal Mail PLC (RMG.L)

- + 4.78% - Cineworld Group PLC (CINE.L)

- + 4.52% - Just Eat Takeaway.com NV (TKWY.AS)

Underperformers:

- -15.7% - Greencore Group PLC (GNC.L)

- -10.7% - Avon Rubber PLC (AVON.L)

- -8.28% - Trainline PLC (TRNT.L)

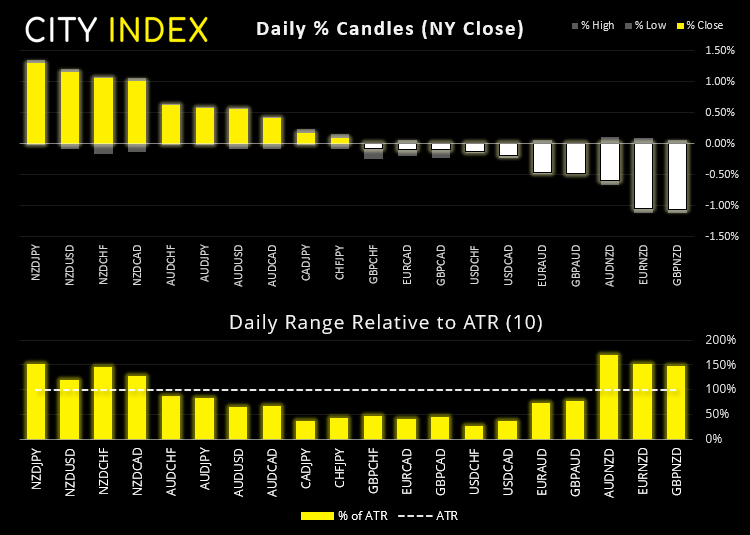

NZD strongest major after hawkish RBNZ meeting

The New Zealand dollar exploded higher after today’s RBNZ meeting, as the central bank sees the OCR rising to 0.49% (nearly a full 25 bp hike) by September 2022. Inflation is now seen at 1.5% by June (up from 1.4% at their previous meeting). Policy was unchanged today, so rates remain at 0.25% and the asset purchases and lending programs are to continue at their current rate.

AUD/NZD fell -0.6% and topped just shy of our initial 1.064 bearish target. With RBA sticking to their dovish guns and hinting rates won’t rise until 2024 then we see further downside potential for the cross.

NZD/USD touched it highest level since late February (just), EUR/NZD is down -0.9% and trades beyond our initial bearish target of 1.6825. NZD/JPY rose to a three-year high and a break above 79.62 resistance (April 2018 high) assumes bullish continuation.

AUD/USD also rose on the back of the higher NZD/USD, yet elsewhere trading ranges were very tight amongst FX majors and crosses. NZD is also the strongest currency this week, whilst CAD, CHF and GBP are the strongest this month.

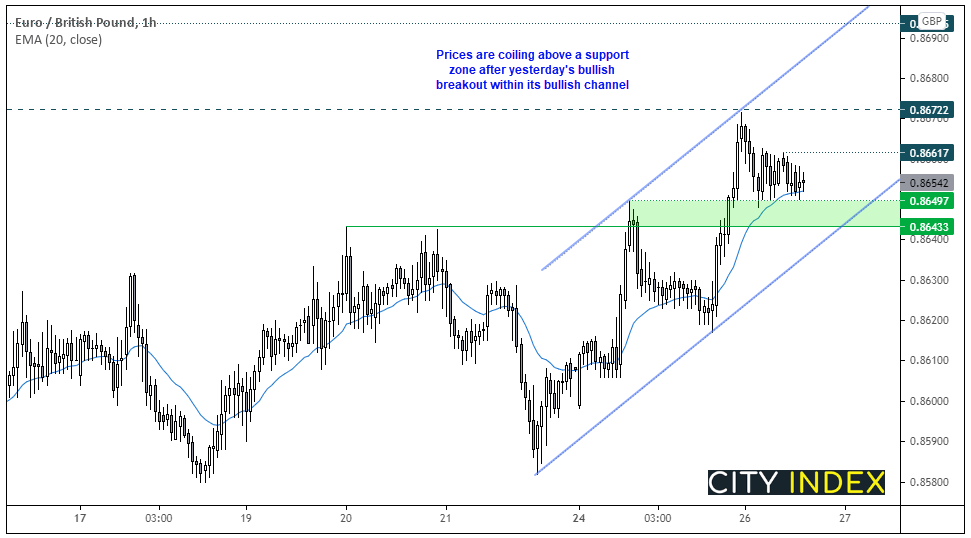

EUR/GBP closed to a two-week high thanks to yesterday’s stronger than expected IFO report from Germany. Prices have since been coiling into a tighter congestion zone on the four-hour chart and building a base above the 0.8643/53 support zone. Our bias remains bullish above this level and a break above the 0.8660 highs assumes bullish continuation. A break back below 0.8643 invalidates the bullish channel and takes it back into range, ahead of yesterday’s breakout.

EUR/USD is also coiling near its highs after breaking to a four-month high yesterday. The four-hour bar is on track for a bullish engulfing candle, so bulls look like they want to take this higher in the European session. As this assumes a weaker dollar, it could also provide a tailwind for metals.

Learn how to trade forex

Gold and silver remain firm

Metals continued to climb higher overnight after posting solid gains yesterday/ Gold is up around 0.4% and trades at 1906, whilst silver has risen 0.65% and sits above 28.00. Our core view remains bullish on both metals and low volatility dips would be welcomed whilst they hold above prior swing lows on the daily charts.

Oil’s rebound ran out of steam yesterday with WTI futures printing a small Doji candle just beneath the May’s high. Given we saw the market sell-off three times this month below 67.00 then traders would be prudent to be mindful of a dip lower from current levels, although we suspect it would be a retracement at best before prices eventually try to break above the 67.98 high.

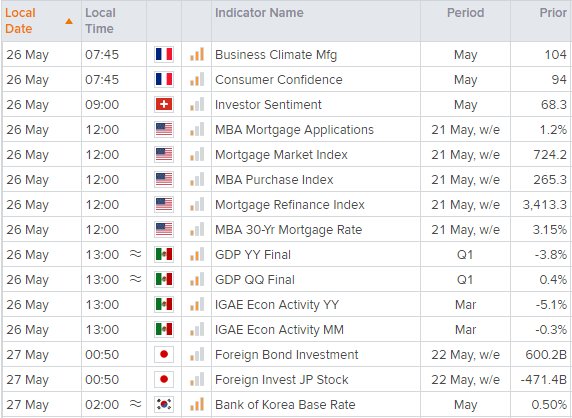

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM