Asian Indices:

- Australia's ASX 200 index fell by -16.6 points (-0.22%) and currently trades at 7,369.60

- Japan's Nikkei 225 index has fallen by -325.77 points (-1.11%) and currently trades at 28,967.28

- Hong Kong's Hang Seng index has risen by 80.13 points (0.28%) and currently trades at 28,516.97

UK and Europe:

- UK's FTSE 100 futures are currently down -31.5 points (-0.44%), the cash market is currently estimated to open at 7,153.45

- Euro STOXX 50 futures are currently down -16 points (-0.39%), the cash market is currently estimated to open at 4,135.76

- Germany's DAX futures are currently down -48 points (-0.31%), the cash market is currently estimated to open at 15,662.57

US Futures:

- DJI futures are currently down -85.85 points (-0.25%)

- S&P 500 futures are currently down -72 points (-0.51%)

- Nasdaq 100 futures are currently down -14.75 points (-0.35%)

Learn how to trade indices

Indices lower overnight

The sell-off which started in Europe and Wall Street continued through the Asian session, although equities pared earlier losses in the second half of the session. The TOPIX 400 is currently trading 0.75% lower and the ASX 200 is down -0.25% after falling around -0.6% after the open.

European an US futures have opened lower and point to a weaker open. We noted in todays video that 7238 (prior record high) could be a pivotal level for today’s session on the S&P 500, given it was tested and held as resistance three times in the closing hours of trade yesterday.

The FTSE is due to open lower today, after printing a bearish hammer at a 16-month high yesterday. Given the weaker sentient for equities globally and signs of a potential retracement on the FTSE, our intraday bias remains bearish below 7176.50 today.

FTSE 100 S/R Levels

- R5: 7200 - 7204

- R4: 7190

- R3: 7176.50

- R2: 7166 - 7169

- R1: 7153

- S1: 7147

- S2: 7143

- S3: 7130

- S4: 7117

- S5: 7100 - 7106

FTSE 350: Market Internals

FTSE 350: 7184.95 (0.17%) 16 June 2021

- 164 (46.72%) stocks advanced and 175 (49.86%) declined

- 24 stocks rose to a new 52-week high, 6 fell to new lows

- 86.61% of stocks closed above their 200-day average

- 19.37% of stocks closed above their 20-day average

Outperformers:

- + 4.45% - Watches of Switzerland Group PLC (WOSG.L)

- + 3.75% - Network International Holdings PLC (NETW.L)

- + 3.47% - Lancashire Holdings Ltd (LRE.L)

Underperformers:

- -4.09% - Hammerson PLC (HMSO.L)

- -3.85% - PureTech Health PLC (PRTC.L)

- -3.60% - Helios Towers PLC (HTWS.L)

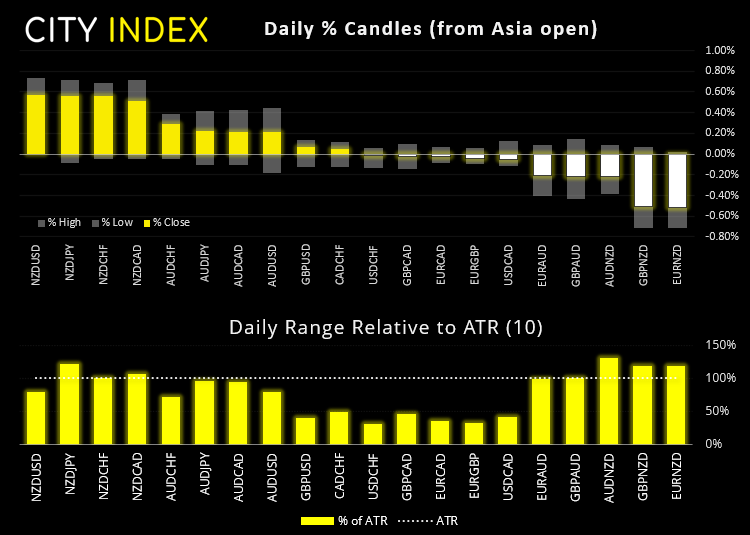

Strong data for AU and NZ overnight

The New Zealand dollar was the strongest major over night following a stronger-than expected GDP report. Q1 growth rose 1.6%, far beyond the consensus of 0.5% and the RBNZ’s own estimate for a -0.6% contraction. This means they escaped a second recession, and expectations for a hike have been brought forward. NZD was broadly higher against its peers, with NZD/JPY rising 0.6% and NZD/USD up 0.5%. AUD/NZD fell to an 8-day low after struggling to retake 1.0800 last week.

The Australian employment report also surpassed expectations with 115.2k jobs added and the unemployment rate falling to 5.1%, down from 5.5% and its lowest level since February. With the Fed now coming around to a hawkish bias it could make it trickier for RBA to simply replay the message to markets that rates won’t change until 2024. But then this is their best chance of keeping their currency lower to help exports, so perhaps they’ll be happy to beat that drum anyway (for the next 2-3 years…). We’ll see.

Asian currencies were lower overnight against the greenback after the Fed surprised with a hawkish FOMC meeting. Although the USD is the weakest major currencies, yet that’s no surprise given the magnitude of yesterday’s rally for the dollar. Over the near-term we see the potential for EUR/USD to bounce from yesterday’s low as part of a technical move but, further out, the downside beckons. GBP/USD is in a similar scenario but we need to see if it can break back above 1.4000.

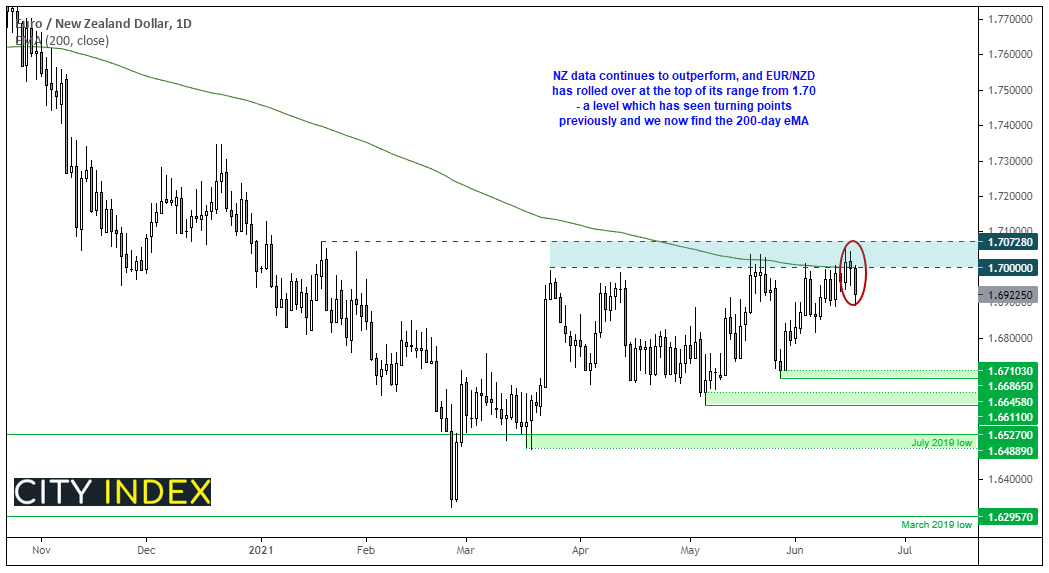

Hands-up, this may not be the prettiest chart you’ll see today. But it does tell a storey with the potential for a divergent theme. With data from NZ outperforming Europe and having the (by far) more hawkish central bank of the two economies then there’s a case for a lower EUR/NZD. And, from a technical perspective, it is of interest as it has rolled over from top of its range around 1.7000 – a round numbered level it has struggled with previously and where we find the 200-day eMA. So, over the near-medium term our bias is bearish whilst prices hold beneath last week’s high and bears would likely welcome any low volatility retracements towards 1.7000 to jump on board.

Learn how to trade forex

Metals remain anchored to yesterday’s low

Copper futures have fallen around -12.7% from their May high and stopped just shy of retesting its October trend support line. Purely from a technical viewpoint we see the potential for a bounce from current levels. Although our bias remains bearish overall beneath 4.435 resistance.

Gold and silver are behaving like most of the FX majors; in a state of shock. Gold has found support at its 200-day eMA so, like copper, the potential for a technical bounce seems apparent. But we’d also be keeping an eye on bearish patterns at higher prices to try and nail a potential swing high.

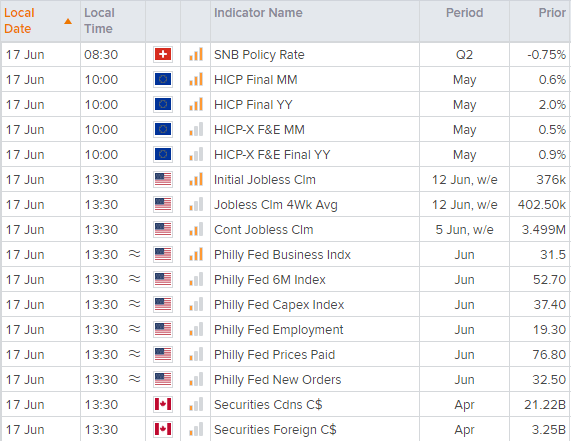

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM