Asian Indices:

- Australia's ASX 200 index rose by 44 points (0.62%) and currently trades at 7,111.90

- Japan's Nikkei 225 index has risen by 62.08 points (0.21%) and currently trades at 29,053.67

- Hong Kong's Hang Seng index has risen by 2.66 points (0.01%) and currently trades at 28,559.80

UK and Europe:

- UK's FTSE 100 futures are currently up 50 points (0.73%), the cash market is currently estimated to open at 6,973.17

- Euro STOXX 50 futures are currently up 32 points (0.82%), the cash market is currently estimated to open at 3,956.80

- Germany's DAX futures are currently up 105 points (0.71%), the cash market is currently estimated to open at 14,961.48

Tuesday US Close:

- The Dow Jones Industrial rose 238.38 points (0.7%) to close at 34,113.23

- The S&P 500 index fell -28 points (-0.667834%) to close at 4,164.66

- The Nasdaq 100 index fell -255.051 points (-1.85%) to close at 13,544.67

In a nutshell, it was a sea of red for European bourses yesterday, with the DAX leading the declines by falling -2.5%, the Euro STOXX 60 index shedding -1.4% with all sectors in the red. Technology, apparel and financial services weighed on the broader index, falling -3.8%, -3.2% and -2.7% respectively. In stark contrast, the ASX 200 is on track to close above 7100 for the first time since February 2020. All but the technology sector is trading higher, led by materials and healthcare stocks. Otherwise, it has been a quiet day in Asia China and Japan on public holidays.

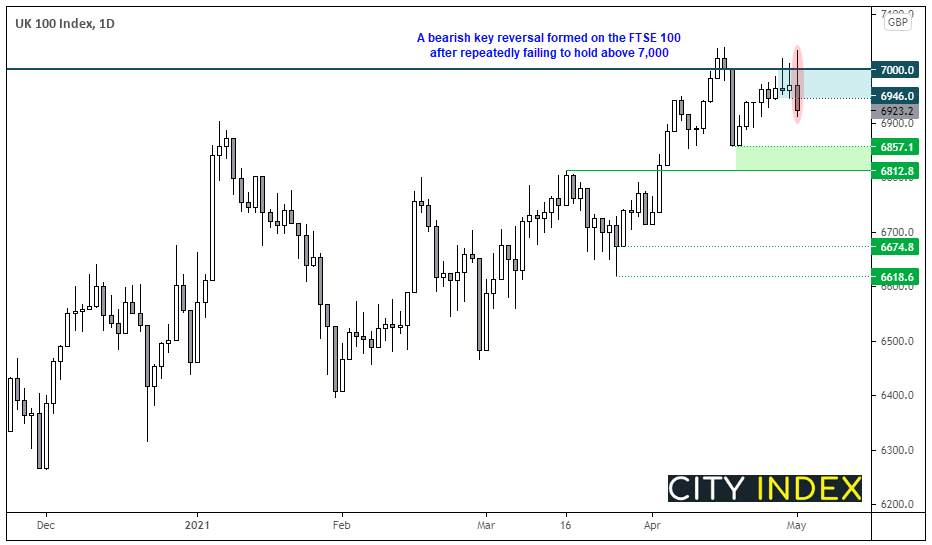

FTSE 100 Prints a Key Reversal below 7,000

Alas, we may have finally seen the swing high on the FTSE after a gruelling climb towards, and failure to hold above, 7,000. Closing the day with a bearish outside candle and closing beneath its 20-day eMA, we strongly suspect its high is in place. And, with above average volume we can label it a key reversal.

- The bias remains bearish below 7,000

- Although, the lows around 6946 should probably hold as resistance if bears really have regained control

- The initial target is the 6812 – 6857 zone

FTSE 350 Internals:

FTSE 350: 6923.17 (-0.67%) 04 May 2021

- 92 (26.21%) stocks advanced and 255 (72.65%) declined

- 49 stocks rose to a new 52-week high, 4 fell to new lows

- 84.33% of stocks closed above their 200-day average

- 18.8% of stocks closed above their 20-day average

Outperformers

- + 5.72% - Frasers Group PLC (FRAS.L)

- + 3.91% - Vectura Group PLC (VEC.L)

- + 3.66% - Workspace Group PLC (WKP.L)

Underperformers:

- -7.00% - Network International Holdings PLC (NETW.L)

- -6.91% - AO World PLC (AO.L)

- -6.05% - Baillie Gifford US Growth Trust PLC (USAB.L)

Learn how to trade indices

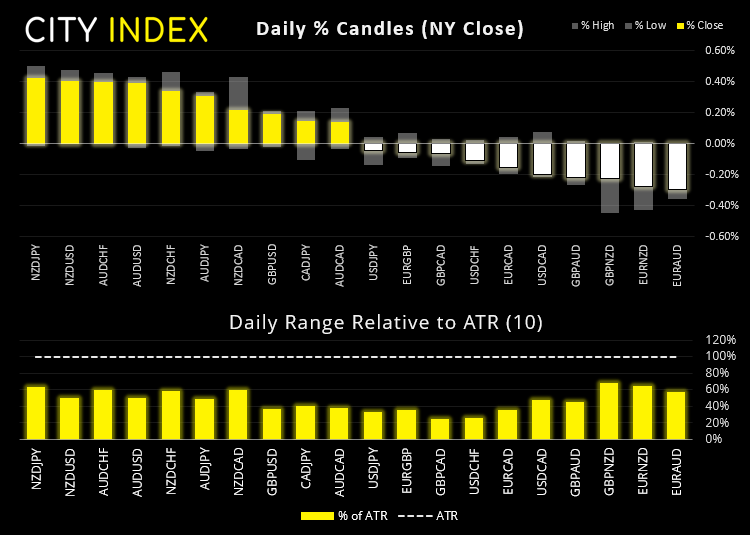

Forex: Falling NZ Unemployment Buoys NZD and AUD

The New Zealand and Australian dollar are the strongest majors overnight, both helped higher by a stronger-than-expected employment report, which saw NZ unemployment fall to 7.4% in Q1. This has helped AUD/CAD remain above yesterday’s low, although our bias remains bearish below 0.9535 resistance and for a break below 0.9457 support.

- The USA dollar is the weakest currency overnight, although volatility remains capped.

- Key resistance for the US dollar index (DXY) remains to be 91.40, making it a pivotal level this session for bears to fade into, or bulls wait for a break above it.

- GBP/CAD is consolidating around 1.7090, on its 20-day eMA yet beneath its 50-day . Given the bearish trend on the four-hour chart, our bias remains bearish beneath 1.7155 resistance and for a re-test of last week’s low around 1.6960.

- GBP/JPY is grinding higher, although two ‘buying tails’ have appeared at or above 150.83 support to show demand is increasing. If it can hold above this support level then the bias is for a run towards the 153.40 high.

Learn how to trade forex

Commodities: Copper and Oil Eye Fresh Highs

Copper prices tried to extend their gains overnight, having printed a fresh 10-year high yesterday. As mentioned in the Asian open report, as it only just closed above the milestone level so we would want to see direct gains today to avoid it rolling over, back beneath the August 2011 high.

Brent futures are within striking distance of $70, making it a key level to monitor this session. Being such a milestone level, we could expect some noise around it but, given yesterday’s bullish engulfing candle and its longer-term bullish trend, the bias remains for an eventual break above it.

Up Next (Times in BST)

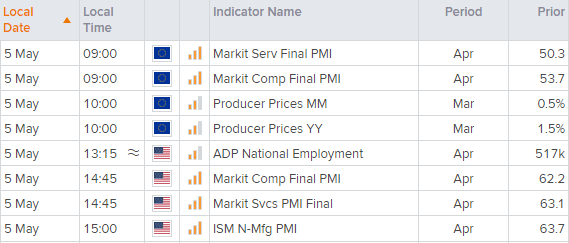

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 08:15 AM

Today 05:45 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM