Whilst today’s inflation print (core PCE) may be irrelevant if the Fed really don’t care about it rising, it still counts for gold if it comes in stronger than expected and could dictate which side of 1900 it closes today.

Asian Indices:

- Australia's ASX 200 index rose by 89.9 points (1.27%) and currently trades at 7,184.80

- Japan's Nikkei 225 index has risen by 141.59 points (0.41%) and currently trades at 34,464.64

- Hong Kong's Hang Seng index has risen by 183.98 points (0.63%) and currently trades at 29,297.18

UK and Europe:

- UK's FTSE 100 futures are currently up 24.5 points (0.35%), the cash market is currently estimated to open at 7,044.17

- Euro STOXX 50 futures are currently up 12 points (0.3%), the cash market is currently estimated to open at 4,051.21

- Germany's DAX futures are currently up 41 points (0.27%), the cash market is currently estimated to open at 15,447.73

Thursday US Close:

- DJI futures are currently up 162 points (0.47%), the cash market is currently estimated to open at 34,626.64

- S&P 500 futures are currently up 28.5 points (0.21%), the cash market is currently estimated to open at 4,229.38

- Nasdaq 100 futures are currently up 13.25 points (0.32%), the cash market is currently estimated to open at 13,671.10

Learn how to trade indices

Asian indices retain bullish streak

Stronger economic data from the US lifted sprits which now sees Asian equities on track to close higher for a seventh consecutive day. MSCI’s world equity index traders just off its record high, and their broad index of Asian shares (excluding Japan) rising 0.3% whilst Japan’s Nikkei 225 rose 1.9% earlier in the session.

The FTSE 100 closed a touch lower during a low-ranging day, to produce a small inside day following Wednesday’s Doji. That this is occurring near at a supposed apex of a symmetrical triangle, with its heaviest single day volume in two months continues to suggest we could be approaching a breakout. Sure, ‘end-of-month’ flows could be attributed to the large volume day, but ultimately this needs to make an impact on the index at some point. So we’ll continue to watch the FTSE to see if it can break below 7,000 or above 7067 with conviction. But, as mentioned in yesterday’s report, as the OBV indicator (on balance volume) continues to trend lower then we suspect a downside break may be more likely at resent.

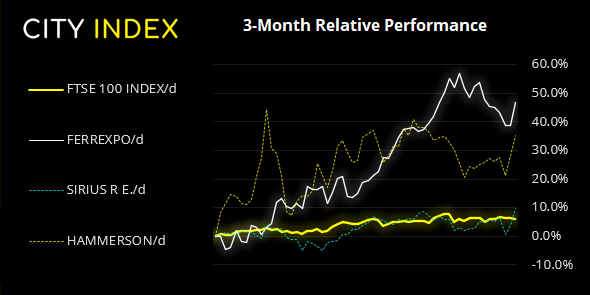

FTSE 350: Market Internals

FTSE 350: 7019.67 (-0.10%) 27 May 2021

- 174 (49.57%) stocks advanced and 161 (45.87%) declined

- 28 stocks rose to a new 52-week high, 2 fell to new lows

- 83.48% of stocks closed above their 200-day average

- 23.65% of stocks closed above their 20-day average

Outperformers:

- + 5.74% - Ferrexpo PLC (FXPO.L)

- + 5.57% - Sirius Real Estate Ltd (SRET.L)

- + 5.54% - Hammerson PLC (HMSO.L)

Underperformers:

- -12.35% - C&C Group PLC (GCC.L)

- -6.07% - Tate & Lyle PLC (TATE.L)

- -5.98% - Centamin PLC (CEY.L)

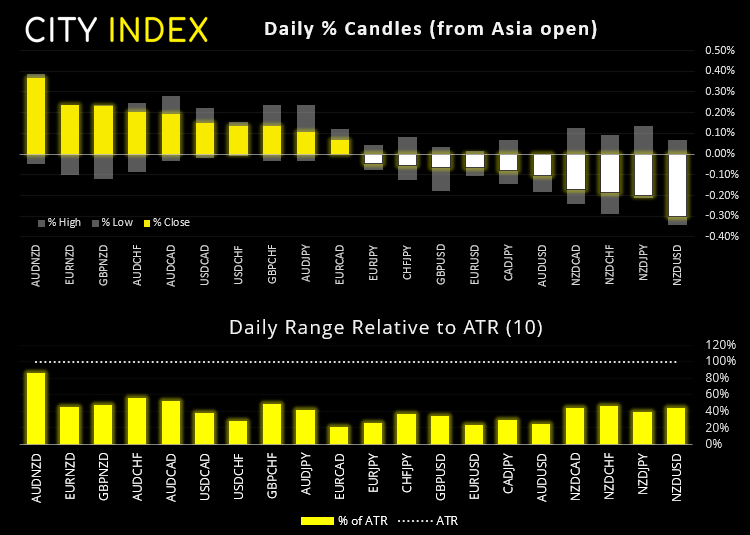

Forex: USD continues to chop around in its range

The US dollar index was a touch lower overnight, although the range it needs to break out of for its next directional move is above 90.30 or (convincingly) below 90.0. Given its direction has mostly alternated each day over the past seven, it could take a surprising inflation beat today to see it break convincingly higher.

The New Zealand dollar was the weakest currency overnight as traders book profits following two days of strong gains post-RBNZ. The Japanese yen was also lower as the jobless rate rose to 2.8%, Tokyo’s CPI fell to 0.2% and Japan readies itself to extend its state of emergency measures just weeks ahead of the Olympics games.

NZD/JPY closed above 80.0 in line with our bullish bias, so we are now hoping to see prices accepted above this breakout level and a new level of support be found. USD/JPY sits just shy of our original 110 target and could well break higher, but at current levels the reward to risk ratio is undesirable.

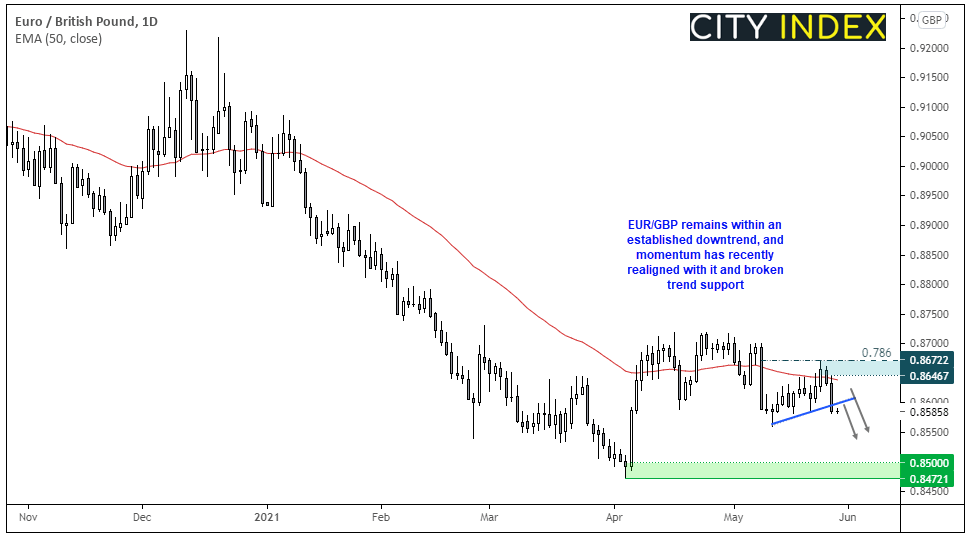

EUR/GBP bears just getting started?

The pound was strong yesterday on rising expectations that a rate hike could come sooner than anticipated. GBP/USD is accelerating away from its 20-day eMA after printing a bullish engulfing candle and is just 25 pips shy of its 2021 high. A break above here brings the 1.4344 target into focus, projected from the head and shoulders breakout. GBP/JPY rose to its highest level since January 2018 and, were it not for the historical swing high sitting just 50 pips away we’d be tempted with a bullish setup.

EUR/GBP has been giving us the run-around recently and, after a few twists and turns, we think we have finally seen the required lower high we wanted to identify after its hard fall from 0.8700 on May 10th. Its post-drop correction found resistance at the 7806% Fibonacci ration and has since closed lower for two straight sessions. The session closed beneath trend support and, with momentum now realigned with its dominant bearish trend we are seeking a move back towards the 0.7472 – 0.8500 lows. If the bearish trend has truly been re-established, we wouldn’t expect to see prices break back above yesterday’s high.

Learn how to trade forex

Commodities: Platinum hold below resistance, gold sits just off its high

Platinum futures broke to a two-day low yesterday, following Wednesday’s bearish pinbar which respected the broken trendline as resistance to form a three-bar bearish reversal on the daily chart (Evening Star Reversal). Our bias remains bearish beneath the hammer high at 1217.60 and a break beneath the 1155.60 low brings 1110 into focus for bears.

Gold is holding steady ahead of today’s inflation data from the US. Whilst it can be argued the print does not matter (as the Fed still think any coming inflation will be both temporary and manageable), gold remains a hedge against inflation so a strong print could send the yellow metal back above 1900 and to new highs. However, with TIPS (treasury inflation-protected securities) rising it does suggest gold may be headed for a correction unless TIPS begin to fall once more. Alternatively, a weak inflation print could help knock gold from its perch.

Copper is also looing constructively bullish after yesterday’s 3% gain. Our bias remains bullish above 4.4350 although we’d like to see prices hold above the 4.5815 high ahead of its next leg higher.

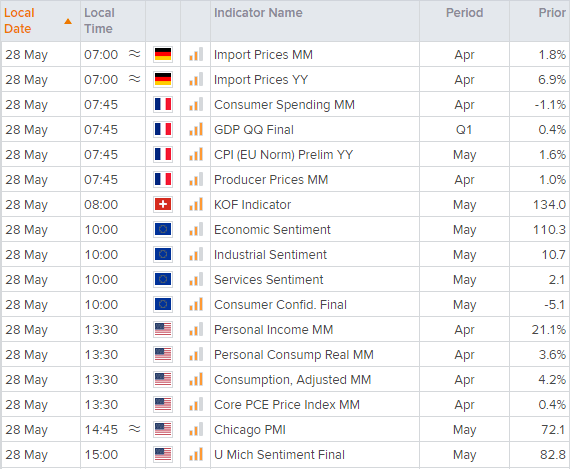

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM