Asian Indices:

- Australia's ASX 200 index rose by 17.1 points (0.23%) and currently trades at 7,350.60

- Japan's Nikkei 225 index has risen by 188.29 points (0.66%) and currently trades at 28,757.31

- Hong Kong's Hang Seng index has risen by 512.36 points (1.86%) and currently trades at 28,027.60

UK and Europe:

- UK's FTSE 100 futures are currently down -4.5 points (-0.06%), the cash market is currently estimated to open at 7,120.92

- Euro STOXX 50 futures are currently up 3.5 points (0.09%), the cash market is currently estimated to open at 4,096.88

- Germany's DAX futures are currently down -1 points (-0.01%), the cash market is currently estimated to open at 15,789.51

US Futures:

- DJI futures are currently up 126.02 points (0.36%)

- S&P 500 futures are currently up 12 points (0.08%)

- Nasdaq 100 futures are currently down -2 points (-0.05%)

Sentiment Remains Buoyant Across Asian indices

Asian equity markets tracked Wall Street higher overnight, which remain buoyant on positive expectations for Q1 earnings. China’s exports beat analyst expectations in June to also lift sentiment, rising 32.3% YoY compared with 23.3% forecast due to strong international demand. China’s trade surplus is now $51.53 billion, up from $45.54 in May.

Still, were it not for the rise of the Delta variant across parts of Asia then the today’s upside may have been more impressive. The Hang Seng was a top performer, rising 1.86%, the TOPIX rose 0.80%, the SCI 300 is up 0.25% and the ASX 200 is currently up 0.2%. Futures markets are currently pointing towards a firmer open.

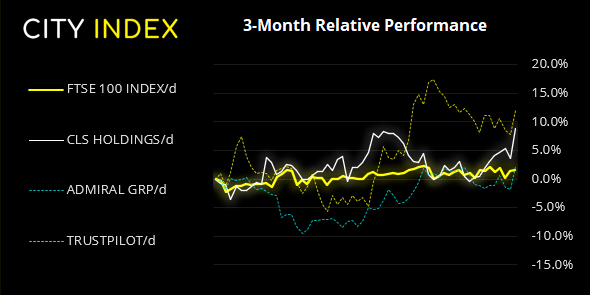

FTSE 350: Market Internals

FTSE 350: 4088.07 (0.05%) 12 July 2021

- 169 (48.15%) stocks advanced and 167 (47.58%) declined

- 35 stocks rose to a new 52-week high, 3 fell to new lows

- 82.34% of stocks closed above their 200-day average

- 57.26% of stocks closed above their 50-day average

- 24.79% of stocks closed above their 20-day average

Outperformers:

- + 5.03% - CLS Holdings PLC (CLSH.L)

- + 3.94% - Admiral Group PLC (ADML.L)

- + 3.83% - Trustpilot Group PLC (TRST.L)

Underperformers:

- -5.79% - Cineworld Group PLC (CINE.L)

- -5.21% - Rolls-Royce Holdings PLC (RR.L)

- -5.20% - Capita PLC (CPI.L)

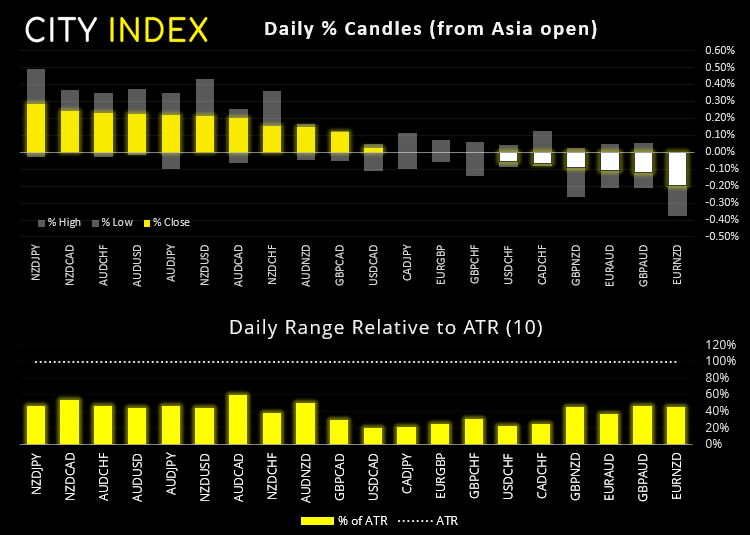

Forex:

AUD and NZD were the strongest currencies overnight, supported by strong trade data from China and a tone of risk-on from equity markets.

Business confidence in Australia was lower in May according to a survey by NAB (National Australia bank). Still, it has fallen from a record high of 37 to its second highest reading of 24 as lockdowns across New South Wales and Victoria weighed on sales and by historical standards overall activity remains high.

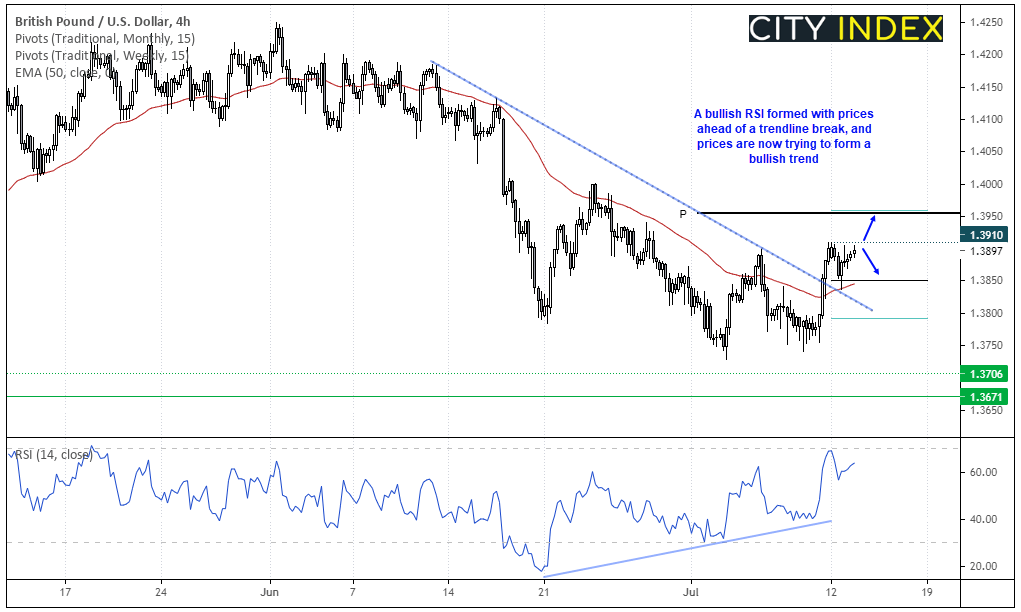

GBP/USD ticks a few of the boxes for a market which is trying to change trend. A bullish divergence formed in the later stages of its bearish move from 1.4200, prices have broken trend resistance and traded above a prior swing high. Furthermore, RSI is now tracking prices higher as a new trend tries to develop. Prices have since found support above the 50-day eMA and weekly pivot, and overnight price action has risen to last week’s high.

A break above 1.3910 brings 1.3950 into focus where the monthly pivot and weekly R1 reside, making it a viable near-term upside target for bulls. A break beneath yesterday’s low invalidates the near-term bias, although we would still monitor its potential for a bullish trend to develop given the clues just mentioned.

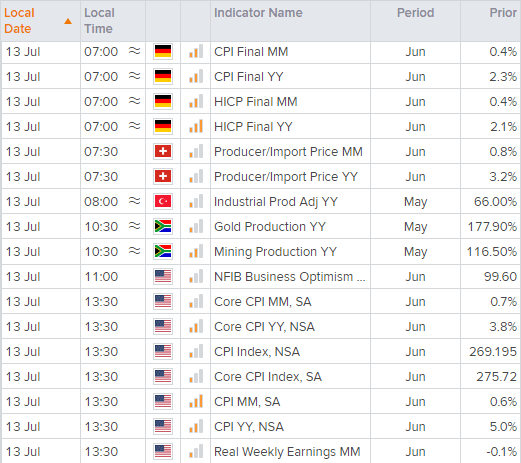

On the data front, final CPI reads for Germany are scheduled for 07:00 BST, otherwise it is a quiet economic calendar until 13:30 when the US release their inflation data. Whilst there are divisions among Fed members over how ‘transitory’ inflation is, a weaker than expected CPI print plays into the hands of doves (lower for longer) and also makes it easier for Jerome Powell to stick to his transitory guns when he testifies to congress on Wednesday. Should inflation run hotter today then it could support the dollar, and force Powell to face tougher questions from congress.

Learn how to trade forex

Commodities:

Platinum futures broke above the 1115 swing high with a firm bullish close yesterday. Holding near yesterday’s 3-week high overnight, momentum remains favourable for bulls today, so our bias remains bullish above the weekly pivot at 1110.

The Thomson Reuters CRB commodity index rose to a four-day high by yesterday’s close to strongly suggest its swig low is in place at 207.39. With the US dollar index failing to hold above its 50-week eMA then its possible we could see the index break to new highs, in line with its established bullish trend on the daily chart (taking oil price higher with it).

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM