Asian Indices:

- Australia's ASX 200 index fell by -36.1 points (-0.49%) and currently trades at 7,306.1

- Japan's Nikkei 225 index has risen by 13.83 points (0.05%) and currently trades at 28,899.1

- Hong Kong's Hang Seng index has risen by 412.09 points (1.46%) and currently trades at 28,721.86

UK and Europe:

- UK's FTSE 100 futures are currently up 8.5 points (1.2%), the cash market is currently estimated to open at 7102.50

- Euro STOXX 50 futures are currently down -2.5 points (-0.06%)

- Germany's DAX futures are currently up -7 points (-0.04%)

US Futures:

- DJI futures are currently up 79 points (0.23%)

- S&P 500 futures are currently up 6.75 points (0.16%)

- Nasdaq 100 futures are currently down 33 points (0.23%)

Learn how to trade indices

APAC flash PMIs off to a soft start

A lift of coronavirus restrictions saw UK business confidence rise to its highest level since 2016, rising 21 percentage points to 11. Furthermore, employers confidence also rose to a near-5-year high of 29. The pound remained flat yet firm overnight, ahead of flash PMI data today.

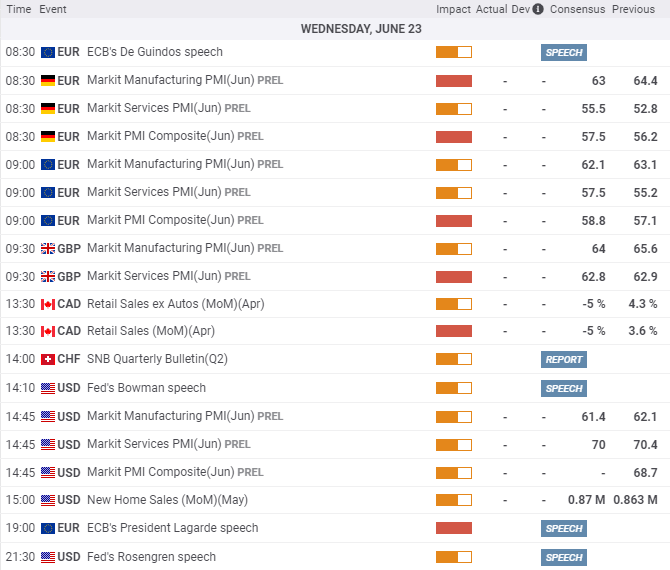

Flash PMI data for Europe and the US are the main data points today in the calendar. Data from the APAC region came in softer than expected, with Australian manufacturing falling to 58.54 (64.4 prior) and service down to 56 (58 prior). This dragged the composite down to 56.1 from 58.0. It was a similar case for Japan’s manufacturing sector which expanded at the slower pace of 51.5 compared with 52.3 expected down from 53.

The FTSE 100 rose 0.39% yesterday to a two-day high and has recouped around half of Friday’s bearish range. It is the second strongest performer week to date at 1.03%, with DAX taking top place at 1.22%. A break above 7100 also takes it back above the 10-day eMA, and we’d like to see prices hold above the 7073.55 low to retain an intraday bullish bias.

FTSE 350: Market Internals

FTSE 350: 4064.49 (0.39%) 22 June 2021

- 255 (72.65%) stocks advanced and 80 (22.79%) declined

- 14 stocks rose to a new 52-week high, 2 fell to new lows

- 85.19% of stocks closed above their 200-day average

- 17.09% of stocks closed above their 20-day average

Outperformers:

- + 7.20% - Sirius Real Estate Ltd (SRET.L)

- + 6.71% - Travis Perkins PLC (TPK.L)

- + 6.17% - Beazley PLC (BEZG.L)

Underperformers:

- -3.37% - Network International Holdings PLC (NETW.L)

- -3.07% - Capita PLC (CPI.L)

- -2.64% - Hargreaves Lansdown PLC (HRGV.L)

Forex: Aussie trade surplus hits a record

Preliminary trade data for Australia saw exports rise 11% and take its trade surplus to a new record of A$13.3 billion. 42% of exports were sent China’s way, and Iron ore accounted for 18% of exports last month. AUD/NZD pared around ¾ of yesterday’s losses after probing the weekly low. It nudged its way higher against the yen, euro, pound, Canadian dollar and Swiss franc. AUD/USD is currently -0.04% lower against the dollar. However, with an outbreak in Sydney behind 120 exposure venues, talk of another lockdown is ramping up with QLD following VIC’s move to close their border with NSW.

The US dollar was the strongest major overnight, rising against all major currencies whilst CHF and NZD were the weakest. GBP/JPY is resting beneath yesterday’s high after reaching out upside target, so the UK’s PMI release could be a make or break for bullish momentum over the near term.

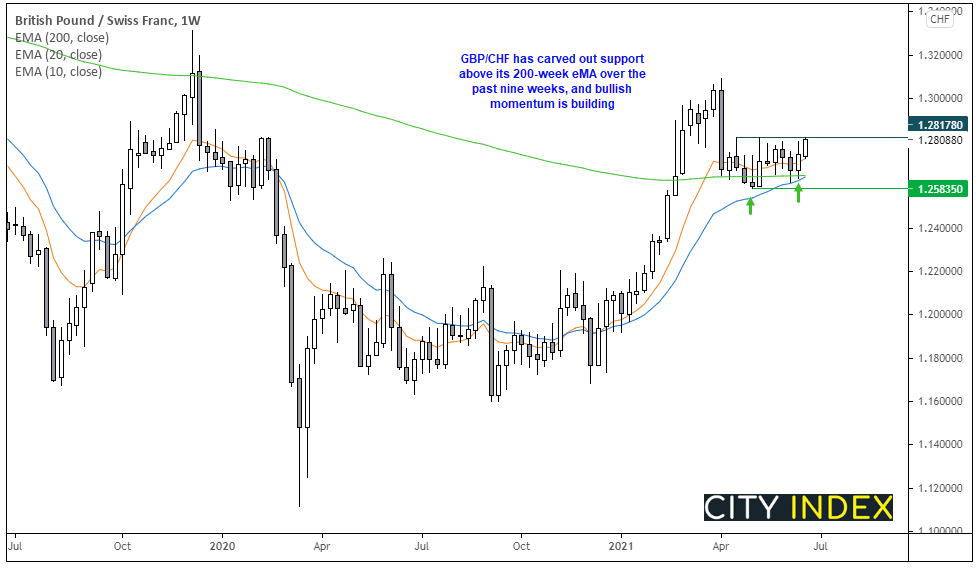

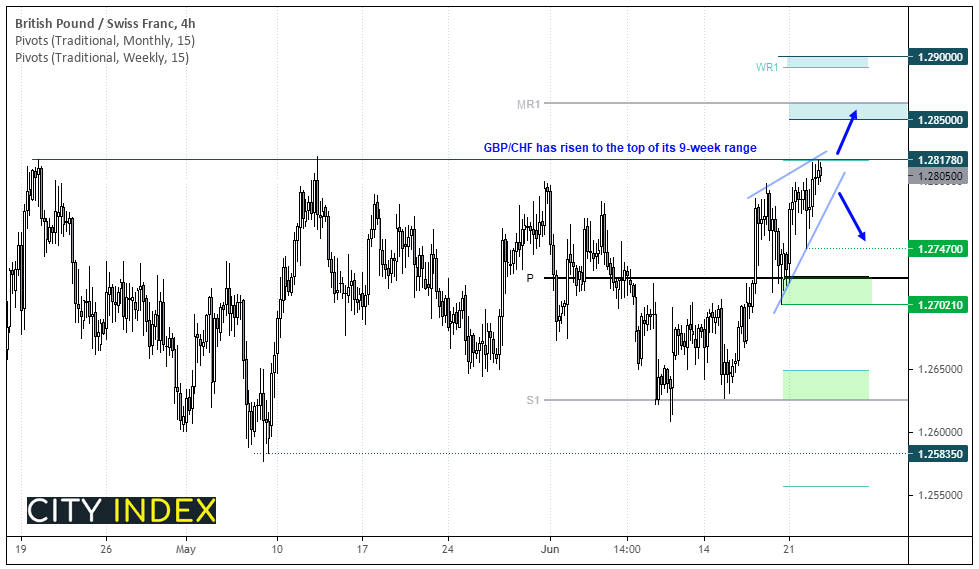

GBP/CHF has risen to the top if its 9-week range ahead of the European open, which places 1.2820 as the main focal point this session. Over this period of time, the weekly chart has mostly held above its 200-week eMA and is now trying to accelerate away from the 10-week eMA. So there is a case for a bullish breakout on the higher timeframes, although whether that occurs today is yet to be seen.

The four-hour chart shows a potential bearish wedge (not textbook, but its there in spirit) which would take prices back towards 1.2700 is confirmed. The weekly R1 pivot is also capping as resistance, so another dip lower is out of the question. But if we can see a break or a hourly close above 1.2820 then it could signal a bullish breakout from its 9-week range and bring

Learn how to trade forex

Commodities drift higher after Powell’s testimony:

Commodities were higher overnight after Jerome Powell kept to his transitory inflation script and pledged to keep rates low.

Copper prices rose 1% overnight and are now testing the broken trendline outline in today’s Asian open report, Take note that the weekly pivot is around 4.85 which leaves a clear line in the sand for bullish or bearish setups today.

Gold futures rose 0.25% although remains within yesterday’s bearish range, and silver futures are currently 0.65% higher.

Brent futures are probing yesterday’s high although we’d need to see a break above 75.58 (April 2019 high) before assuming resumption of its bullish trend. Prices gave back earlier gains yesterday after OPEC+ talked about raising production.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM