Asian Indices:

- Australia's ASX 200 index fell by -80.1 points (-1.12%) and currently trades at 7,092.70

- Japan's Nikkei 225 index has fallen by -858.74 points (-0.28%) and currently trades at 28,666.90

- Hong Kong's Hang Seng index has fallen by -613.45 points (-2.15%) and currently trades at 27,982.21

UK and European futures:

- UK's FTSE 100 futures are currently down -91.5 points (-1.29%), the cash market is currently estimated to open at 7,032.18

- Euro STOXX 50 futures are currently down -54 points (-1.35%), the cash market is currently estimated to open at 3,969.35

- Germany's DAX futures are currently down -186 points (-1.21%), the cash market is currently estimated to open at 15,214.41

US futures:

- DJI futures are currently down -92 points (-0.27%), the cash market is currently estimated to open at 34,456.53

- S&P 500 futures are currently down -125 points (-0.94%), the cash market is currently estimated to open at 4,063.43

- Nasdaq 100 futures are currently down -22.25 points (-0.53%), the cash market is currently estimated to open at 13,336.83

Asian indices and futures point lower

Shares across Asia were lower overnight, following a weak lead from Wall Street. The Hang Seng was down -2.2%, the TOPIX came off -1.9% and the ASX 200 fell down -1.2% in early trade. China’s producer prices rose at their fastest pace in by 6.8% YoY versus 6.5% expected whilst inflation rose 0.9% YoY, up from 0.4% prior. Yet with factory prices rising so sharply in the world’s second largest economy, it only adds to the concerns that inflation will rise faster than expected and catch some central bank off guard – prompting them to raise interest rates ‘behind the curve’.

Futures are also pointing lower, with the S&P 500 E-mini breaking to three day low after printing a bearish engulfing candle at its record high yesterday. And once again tech stocks are leading the decline with the Nasdaq 100 E-mini contract down over -1% in overnight trade.

FTSE 350: Market Internals

FTSE 350: 7123.68 (-0.08%) 10 May 2021

- 137 (39.14%) stocks advanced and 208 (59.43%) declined

- 56 stocks rose to a new 52-week high, 2 fell to new lows

- 86.57% of stocks closed above their 200-day average

- 26.29% of stocks closed above their 20-day average

Outperformers

- + 10.5% - Greggs PLC (GRG.L)

- + 8.16% - Safestore Holdings PLC (SAFE.L)

- + 7.28% - Victrex PLC (VCTX.L)

Underperformers:

- -6.67% - Baillie Gifford US Growth Trust PLC (USAB.L)

- -6.55% - Allianz Technology Trust PLC (ATT.L)

- -6.21% - Scottish Mortgage Investment Trust PLC (SMT.L)

Learn how to trade indices

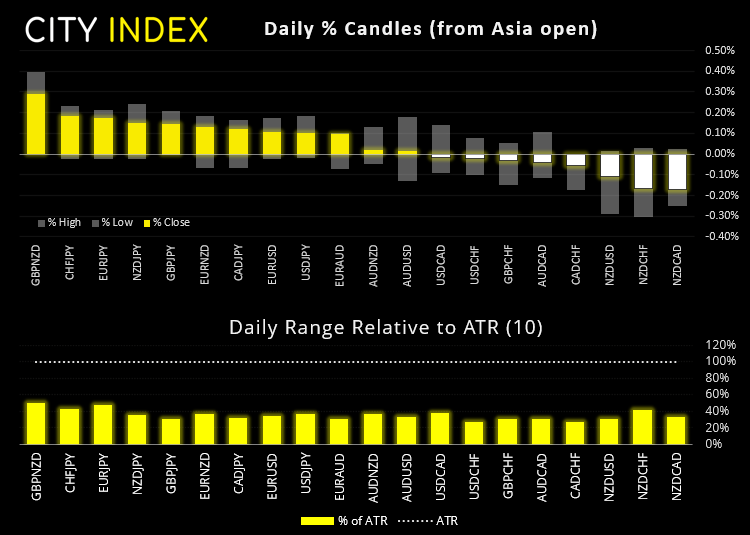

Forex: GBP holds onto gains overnight

The US dollar index (DXY) is holding above 90.00 and yesterday’s small doji warns of its potential to produce a minor countertrend bounce. This has seen EUR/USD meander around April’s high after reaching its bullish wedge target and leaves the door open for a slightly deeper retracement from current levels before its next leg higher resumes. 1.2130 and 1.2100 are key levels for bulls to defend over the coming session/s.

FX pairs remained in tight ranges, which saw GBP hold onto gains following a strong bullish session yesterday. GBP/CHF reached our initial target at 1.2736 and now consolidates in a tight range around resistance. GBP/JPY closed to a near three-year high, so today’s pivotal level is the breakout at 153.42. And GBP/USD closed above 1.4000 to confirm a bullish reversal pattern (head and shoulders) which, if successful, projects a target around 1.4344. Our bias remains bullish above the 1.4000 neckline.

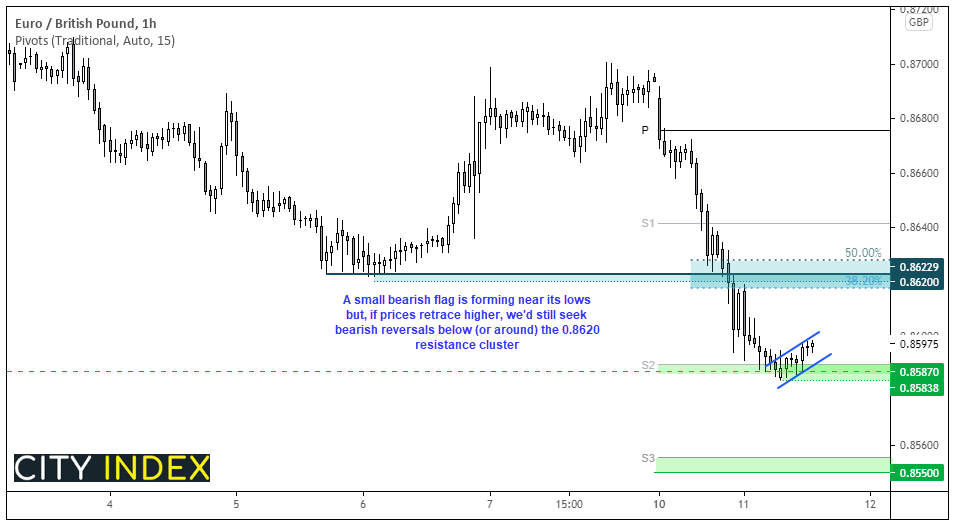

Price action on EUR/GBP’s daily chart looked like a slam dunk (in that prices were slammed aggressively lower). After suffering its worst day in seven months, EUR/GBP closed practically on the April 19th low and overnight trade has made little effort to retrace from it.

If we switch to the one-hour chart we can see how direct losses were yesterday, so we’d prefer to fade into minor rebounds and anticipate a break beneath the 0.8587 low. And given support has also been found at the monthly S2 support level, then the potential for a technical bounce is on the cards – but the question is to how deep it may be, if one occurs at all. Ultimately, we would consider bearish setup beneath the resistance cluster around 0.6820 (swing low, Fibonacci retracements) and for a run towards the monthly S3 pivot near 0.8555.

Learn how to trade forex

Metals remain anchored to their highs

Gold remains around its three-month high at 1835, although a small selling tail (upper wick) yesterday shows a minor sign of exhaustion at its high. The monthly S2 resistance level and trendline resistance also reside around 1850-1860, making the reward to risk ratio for bulls a little undesirable around current levels. We’d prefer to wait for dips but overall out bias remains bullish above 1800.

Silver has printed two bearish hammers at the top of its resistance channel to warns of a hesitancy to continues its trend. However, support from the monthly R1 is at 27.00 and prior resistance at 26.63 provide potential areas for bulls to reload.

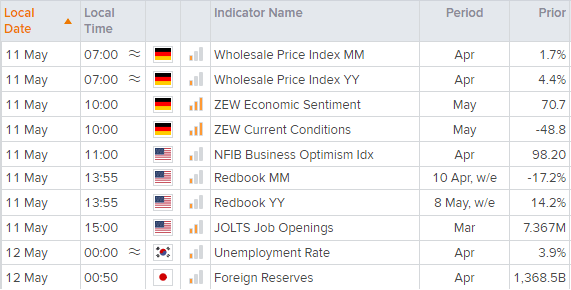

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM