Asian Indices:

- Australia's ASX 200 index rose by 66.3 points (0.93%) and currently trades at 7,208.90

- Japan's Nikkei 225 index has risen by 120.38 points (0.42%) and currently trades at 29,930.56

- Hong Kong's Hang Seng index has fallen by -129.68 points (-0.44%) and currently trades at 29,338.32

UK and Europe:

- UK's FTSE 100 futures are currently down -1 points (-0.01%), the cash market is currently estimated to open at 7,079.46

- Euro STOXX 50 futures are currently up 6 points (0.15%), the cash market is currently estimated to open at 4,077.75

- Germany's DAX futures are currently up 16 points (0.1%), the cash market is currently estimated to open at 15,583.36

US Futures:

- DJI futures are currently up 9 points (0.03%), the cash market is currently estimated to open at 34,584.31

- S&P 500 futures are currently up 1.25 points (0.01%), the cash market is currently estimated to open at 4,203.29

- Nasdaq 100 futures are currently up 0.75 points (0.02%), the cash market is currently estimated to open at 13,655.34

Learn how to trade indices

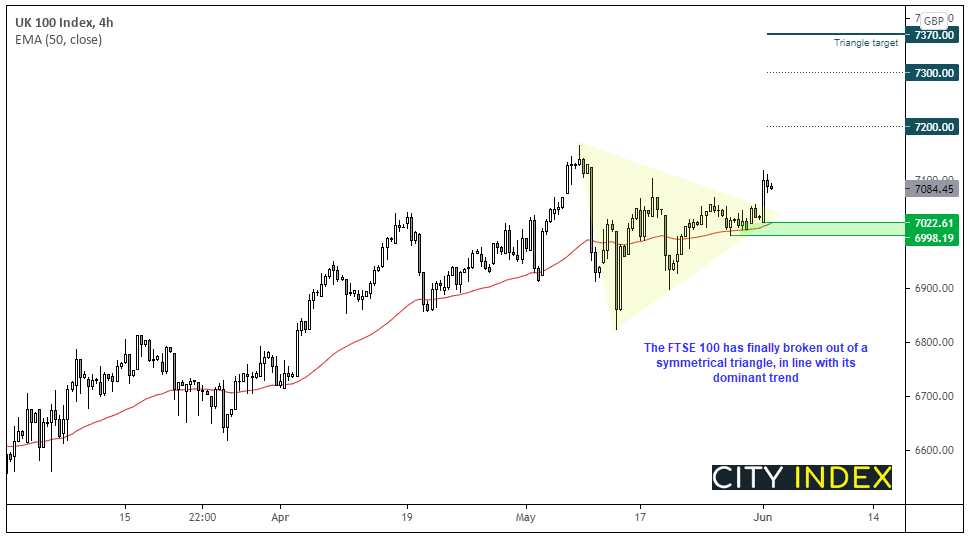

The FTSE 100 finally broke out of its triangle formation on the daily chart to the upside. When prices converge in such a manner it is usually indicative of pending volatility. We can see the four-hour chart produced a bullish opening Marabuzo candle which sprang higher from the 50-bar eMA. The symmetrical triangle projects a target around 7370, although the 7200 and 7300 handles make viable targets, assuming it can break above 7100 in due course. Our bias remains bullish above the 6998 swing-low.

The Euro STOXX 600 index rose 0.75% yesterday and all sectors except healthcare closed higher, led by basic resources, automobile and parts and oil and gas. The DAX hit a record high yet its bearish pinbar suggests near-term exhaustion. A break beneath 15,350 warns of a correction but, until then, we suspect dip buyers to take interest in potential longs above that swing low.

Asian shares were lower by the second half of the session led by China’s CSI300 (-0.95%) and Singapore STI (-0.85%). The ASX 200 bucked the trend with a near 1% gain and closed to a new record high following a strong GDP report for Q1, as traders looked past Melbourne headed for lockdowns to be extended for a further week.

FTSE 350: Market Internals

FTSE 350: 7080.46 (0.82%) 01 June 2021

- 245 (69.80%) stocks advanced and 86 (24.50%) declined

- 50 stocks rose to a new 52-week high, 1 fell to new lows

- 85.19% of stocks closed above their 200-day average

- 23.08% of stocks closed above their 20-day average

Outperformers:

- + 9.08% - Tullow Oil PLC (TLW.L)

- + 6.62% - Trainline PLC (TRNT.L)

- + 5.56% - IWG Plc (IWG.L)

Underperformers:

- -12.2% - Vectura Group PLC (VEC.L)

- -3.39% - Marks and Spencer Group PLC (MKS.L)

- -3.31% - IntegraFin Holdings plc (IHP.L)

Forex: AUD rallies on Australian GDP beat

The Australian dollar extended yesterday’s gains overnight thanks to a strong GDP print, which now sees underlying growth above pre-pandemic levels. It’s debatable as to whether the momentum will last, but a positive outcome none the less. GDP rose 1.8% in Q2, with 0.7% of it thanks to private household consumer spending.

AUD/USD briefly rose to a five-day high, AUD/NZD remains stuck beneath 1.0714 resistance and currently on track for a bearish pinbar (which would pique our bearish swing-trade interest). AUD/CAD and AUD/CHF are also higher yet remains in their sideways corrections at recent swing lows.

Bearish outside/engulfing candles formed across a few GBP pairs yesterday as traders were becoming concerned that a rise of a covid variant may delay the easing of lockdown restrictions. Boris Johnson has downplayed these fears, yet GBP traders don’t yet appear to be ‘buying it’.

GBP/USD failed to hold onto its brief break above the February high and closed with a bearish engulfing/outside day. Given the bearish hammer seen two week ago it appears that GBP is trying to carve out a messy top (whilst the US dollar index remains supported above 89.50).

So, we can now forget the potential for an inverted head and shoulders breakout on GBP/CHF following yesterday’s bearish close. But it could allow traders to indulge in the range between 1.2576 and 1.2817. Going into today’s session bears may be interested to see any signs of weakness around Monday’s low (also near the 20-day eMA which it now trades below). If sentiment remains sour for the British pound then the 1.2650 lows appears a feasible target for today, a break beneath which brings the lows around 1.2600 into focus.

Learn how to trade forex

Commodities: Metals to correct?

Gold and silver go into this session on the back foot, with the former printing a bearish outside day and the latter a bearish hammer yesterday. We suspect gold could ow be entering a bit of a choppy correction whilst the US dollar defends its lower, but our core view remains bullish above 1872. Silver’s bearish hammer (and lower high) is not constructive for our bullish case, even if prices do remain in the bullish channel. So, for us its one to step aside from until the picture becomes clearer. A break below 27.20 switches us toa bearish bias.

Brent held above $70 overnight and traders are trying to build a level of support. If we see prices dip below it today then take note of the trendline support nearby that may scupper chances of a large sell-off. Buy, given the bullish outlook for oil in general out bias remains bullish above 70, making it a pivotal level over the next few sessions.

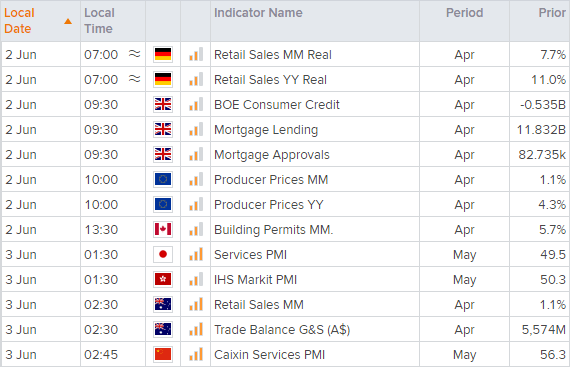

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 08:15 AM

Today 05:45 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM