Asian Indices:

- Australia's ASX 200 index rose by 27.5 points (0.37%) and currently trades at 7,443.00

- Japan's Nikkei 225 index has risen by 264.57 points (0.92%) and currently trades at 28,540.28

- Hong Kong's Hang Seng index has risen by 23.31 points (0.09%) and currently trades at 26,150.24

UK and Europe:

- UK's FTSE 100 futures are currently up 11.5 points (0.16%), the cash market is currently estimated to open at 7,216.05

- Euro STOXX 50 futures are currently up 8 points (0.19%), the cash market is currently estimated to open at 4,196.81

- Germany's DAX futures are currently up 13 points (0.08%), the cash market is currently estimated to open at 15,555.98

US Futures:

- DJI futures are currently up 73.92 points (0.21%)

- S&P 500 futures are currently up 13 points (0.08%)

- Nasdaq 100 futures are currently up 2.5 points (0.06%)

Indices

Earnings season heats up with week and finance is off to a good start ahead of the open. HSBC beat market expectations with a 74% rise in profits in Q3. Facebook release their earnings today after US market close.

China’s NDRC (National Development and Reform Commission) has summoned several property developers to meet on Tuesday, most of which are large dollar bond issuers. Presumably linked to the Evergrande debacle, all eyes will be on China’s markets tomorrow. The CSI300 is currently flat whilst the SSE composite is 0.3% higher.

The FTSE 100 didn’t see a compelling breakout of its potential bull flag on Friday, but it gave it a shot – and the patterns remains one to monitor. The 10-day eMA continues to support, although a flag could still allow for minor new lows to e printed before it eventually breaks higher.

The DAX remains in a period of consolidation at around the midway point between its August high to October low. A 3-wave rally began with a bullish hammer at the 200-day eMA, so if this is an impulsive move higher, we should not see much of a pullback (as wave 3 tends to be the strongest). Ultimately our bias remains bullish above 15,300 and for a break above last week’s high to suggest trend continuation.

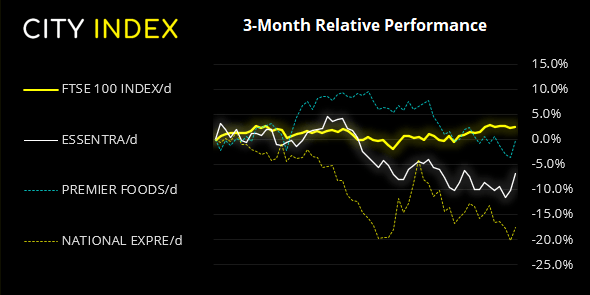

FTSE 350: Market Internals

FTSE 350: 4126.41 (0.20%) 22 October 2021

- 195 (55.56%) stocks advanced and 143 (40.74%) declined

- 10 stocks rose to a new 52-week high, 4 fell to new lows

- 56.98% of stocks closed above their 200-day average

- 33.9% of stocks closed above their 50-day average

- 22.79% of stocks closed above their 20-day average

Outperformers:

- + 3.93%-Essentra PLC(ESNT.L)

- + 3.54%-Premier Foods PLC(PFD.L)

- + 3.41%-National Express Group PLC(NEX.L)

Underperformers:

- -5.99%-London Stock Exchange Group PLC(LSEG.L)

- -4.69%-Micro Focus International PLC(MCRO.L)

- -3.92%-AO World PLC(AO.L)

Forex:

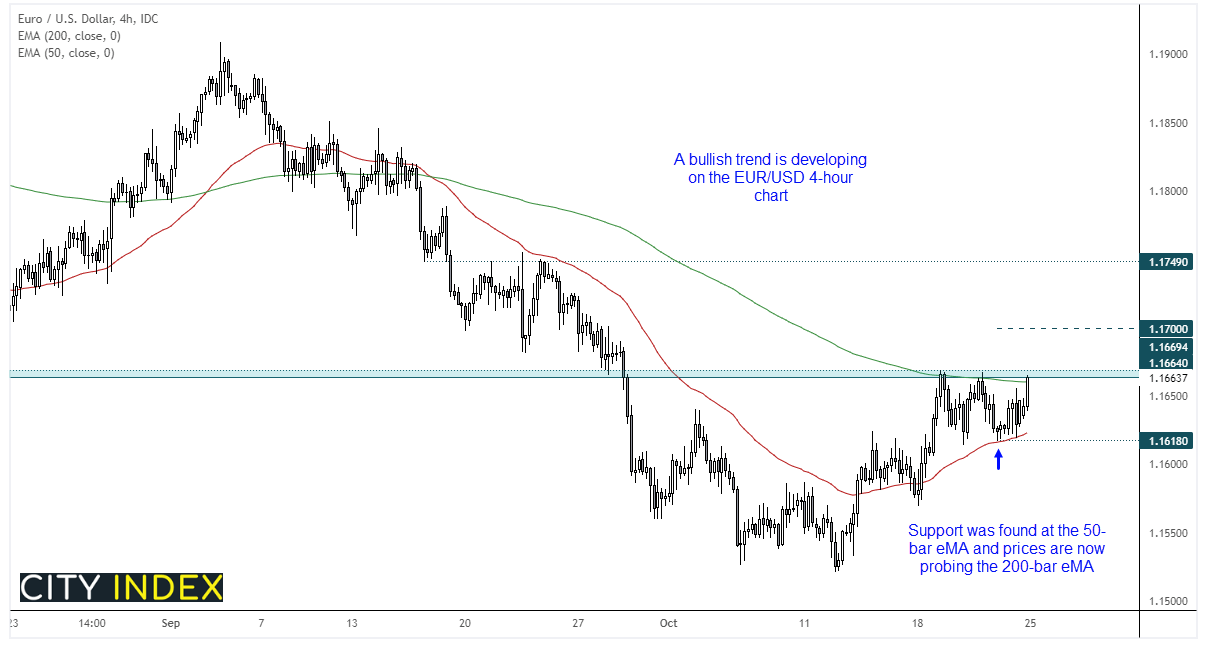

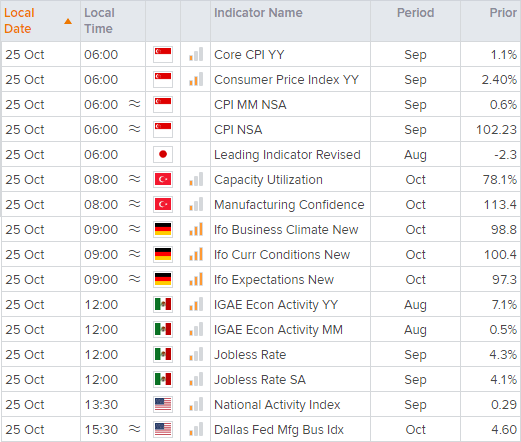

German IFO business report is scheduled for 09:00 BST, and the focus is on whether their economy continues to be weighed down by the ‘bottleneck recession’. The business climate indicator topped 4-months ago and remains below 100 (with conditions) to show contraction. Flash PMI data on Friday also underwhelmed, so further weakness appears more likely than not in today’s report. That said, an upside surprise would likely provide the more volatile reaction for Euro pairs. Outside of that there is little in the way of market-moving data sets, with Mexican employment data at 12:00 and US business sentiment reads at 13:30 and 15:30 today.

A bullish trend is developing on the four-hour EUR/USD chart. The 50-dar eMA recently provided support for its second higher low, and prices are now trying to break above the 200-bar eMA. A disappointing IFO report could send this initially low, yet with weak data expected anyway it may not come as much of a surprise, so it may only require a minor beat for Euro to gain more strength.

We’re now looking for a break above last week’s high to assume bullish continuation with its first major resistance level being the 1.174 handle. Our bias remains bullish above 1.1618.

Commodities:

Copper futures have retraced around -7.5% from last week’s high and it is trying to establish a base above 4.500. Whilst we cannot say for sure the correction is nearing completion we do remain bullish above 4.00 over the longer-term, and now looking for prices to build a layer of support above the broken trendline on the daily chart.

WTI has hit a fresh 7-year high overnight and the front-month futures contract trades around 84.55. Should it close higher this week it will be the 8th consecutive bullish week which is a metric it has not achieved since 2013.

Up Next (Times in BST)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Trade Ideas articles

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM