Asian Indices:

- Australia's ASX 200 index fell by -5.4 points (-0.07%) and currently trades at 7,446.80

- Japan's Nikkei 225 index has fallen by 174.7 points (-0.59%) and currently trades at 29,332.35

- Hong Kong's Hang Seng index has fallen by -17.85 points (-0.07%) and currently trades at 24,745.92

- China's A50 Index has fallen by -82.1 points (-0.53%) and currently trades at 15,496.31

UK and Europe:

- UK's FTSE 100 futures are currently down -23 points (-0.32%), the cash market is currently estimated to open at 7,277.40

- Euro STOXX 50 futures are currently down -18.5 points (-0.43%), the cash market is currently estimated to open at 4,334.03

- Germany's DAX futures are currently down -49 points (-0.31%), the cash market is currently estimated to open at 15,997.52

US Futures:

- DJI futures are currently up 104.27 points (0.29%)

- S&P 500 futures are currently down -24 points (-0.15%)

- Nasdaq 100 futures are currently down -11.5 points (-0.24%)

Indices

Despite a positive start, equity markets across Asian traded lower overnight as investors squared up positions ahead of this week’s first set of inflation data from the US. The ASX 200 was an underperformer following weak earnings from banks.

Japan’s equity markets were the weakest performers on the day, with the TOPIX down around -0.7% and the Nikkei around -0.5% lower. Traders were seemingly underwhelmed with the government of Japan’s announcement that it would provide around ¥100k (around US $870) per child under 18, although reports had surfaced of this scenario over the weekend.

Futures markets are pointing to a lower open for European indices today.

FTSE 350: Market Internals

FTSE 350: 4190.92 (-0.05%) 08 November 2021

- 133 (37.89%) stocks advanced and 210 (59.83%) declined

- 14 stocks rose to a new 52-week high, 3 fell to new lows

- 64.1% of stocks closed above their 200-day average

- 63.82% of stocks closed above their 50-day average

- 21.08% of stocks closed above their 20-day average

Outperformers:

- + 12.4%-Darktrace PLC(DARK.L)

- + 7.06%-Investec PLC(INVP.L)

- + 5.89%-TI Fluid Systems PLC(TIFS.L)

Underperformers:

- -5.37%-Baltic Classifieds Group PLC(BCG.L)

- -4.21%-Discoverie Group PLC(DSCV.L)

- -3.91%-Sirius Real Estate Ltd(SRET.L)

Forex:

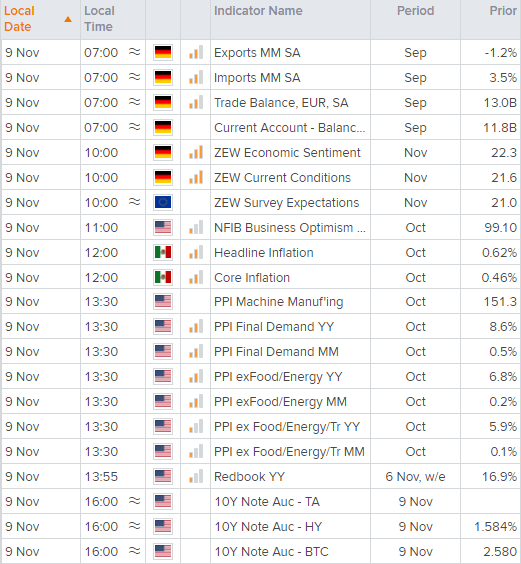

It’s a busy day for central bank speeches. The Fed’s Bullard kicks off at 12:50, Jerome Powell’s pre-recorded speech rolls from 14:00, BOE’s Governor Andrew Bailey speaks at 16:00, The Fed’s Daly at 16:35, BOC’s Beaudry speaks at 17:10 and the Governor himself at 22:45.

Then at 13:30 traders have US producer prices to look forward to, which in some ways could be seen as the warm-up act for Wednesday’s inflation report. Strong producer prices combined with weak data from Germany could see the dollar recoup some lost ground.

But first, German trade balance data is scheduled for 07:00 GMT. In October, exports contracted for the first month in 15 as bottlenecks in the supply chain continued to bite. They are expected to recover by 0.5% in October, up from -1.5% in September. Then at 10:00 the German ZEW economic report is released. It has fallen for five consecutive months and expected to slip for a 6th. A weak ZEW report with weaker exports could spell trouble for the euro today, whilst a (welcomed) upside surprise could help EUR/USD hold onto early gains.

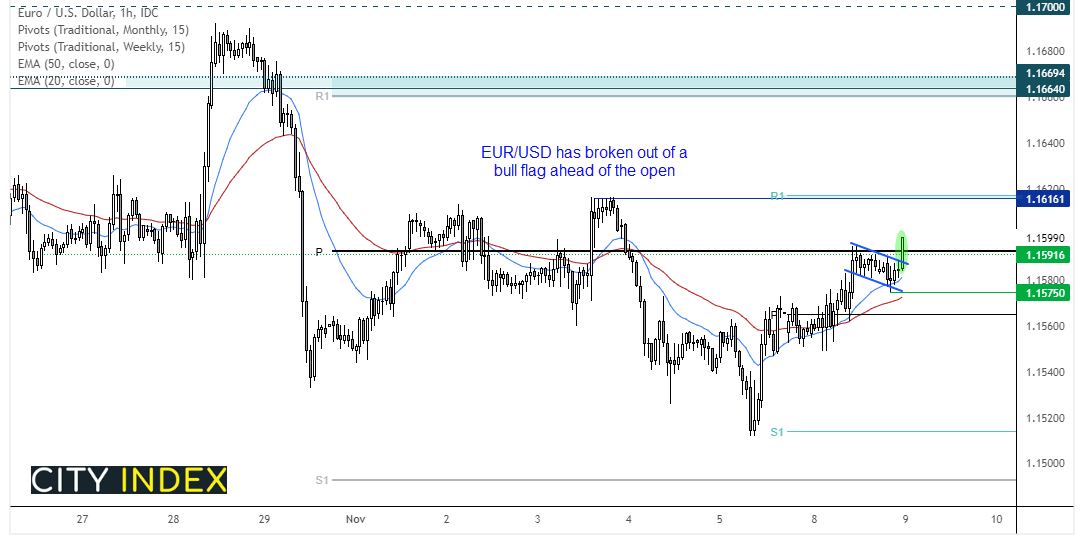

EUR/USD has broken out of a bull flag pattern ahead of today’s open. A bullish trend is forming on the hourly chart and holding above the 20 and 50-bar eMA’s. At the time of writing, the euro is trying to close above the monthly pivot. If it can perform a solid close then bulls need to break it above the 1.16 handle to continue its trend, in which case our bias would then be bullish above 1.1575 as we seek a run towards the 1.1616 high / weekly R1 pivot.

Commodities:

Silver’s rally has stalled just beneath the weekly R1 pivot and retraced, and currently show the potential for a bull flag breakout on the hourly chart.

Platinum futures are holding above trend support on the daily chart, with a swing low also resecting the 50 and 20-day eMA’s. We suspect it will eventually break higher (along with other metals) although inflation data and the US dollar’s reaction around this week’s inflation data will be key.

Up Next (Times in BST)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 08:15 AM

Latest Forex articles

Yesterday 11:09 PM

Yesterday 04:00 PM