Asian Indices:

- Australia's ASX 200 index rose by 47.5 points (0.64%) and currently trades at 7,422.40

- Japan's Nikkei 225 index has risen by 101 points (0.35%) and currently trades at 29,317.44

- Hong Kong's Hang Seng index has risen by 338.75 points (1.31%) and currently trades at 26,125.96

UK and Europe:

- UK's FTSE 100 futures are currently up 6 points (0.08%), the cash market is currently estimated to open at 7,223.53

- Euro STOXX 50 futures are currently down -3.5 points (-0.08%), the cash market is currently estimated to open at 4,163.33

- Germany's DAX futures are currently down -9 points (-0.06%), the cash market is currently estimated to open at 15,506.83

US Futures:

- DJI futures are currently up 198.7 points (0.56%)

- S&P 500 futures are currently down -15.25 points (-0.1%)

- Nasdaq 100 futures are currently down -1.5 points (-0.03%)

Indices

Asian equity markets sustained the positive vibe from Wall Street as traders remained optimistic about the global recovery. Which is in stark contrast to the recent selloff which was caused by concerns of stagflation.

Japan’s exports slumped to a 7-month low of 13% y/y in September, down from 26.2% in August and its peak of 49.6% in May. Exports to the US fell -3% although rose to 1.3% for Asian, 10.3% of which was to China. With imports costs rising thanks to the spike in oil prices and weaker yen, it is metric which could weigh on BOJ’s outlook when they revise their inflation forecasts later this month. The Nikkei 225 gave back early gains and now trades just 01% higher for the session.

The FTSE 100 is coiling up near its recent highs on the four-hour chart. With sentiment remaining positive for equities overall we’re hopeful to see an upside break. Key support levels for bulls to defend include 7180 and 7160.

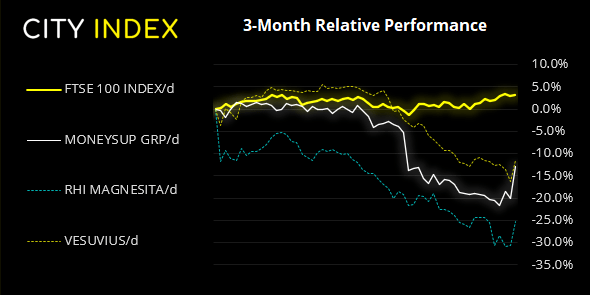

FTSE 350: Market Internals

FTSE 350: 4136.42 (0.19%) 19 October 2021

- 217 (61.82%) stocks advanced and 116 (33.05%) declined

- 9 stocks rose to a new 52-week high, 3 fell to new lows

- 60.11% of stocks closed above their 200-day average

- 31.91% of stocks closed above their 50-day average

- 20.51% of stocks closed above their 20-day average

Outperformers:

- + 8.9%-Moneysupermarket.Com Group PLC(MONY.L)

- + 7.7%-RHI Magnesita NV(RHIM.VI)

- + 5.8%-Vesuvius PLC(VSVS.L)

Underperformers:

- -5.8%-International Consolidated Airlines Group SA(ICAG.L)

- -5.6%-TUI AG(TUIT.L)

- -5.4%-Harbour Energy PLC(HBR.L)

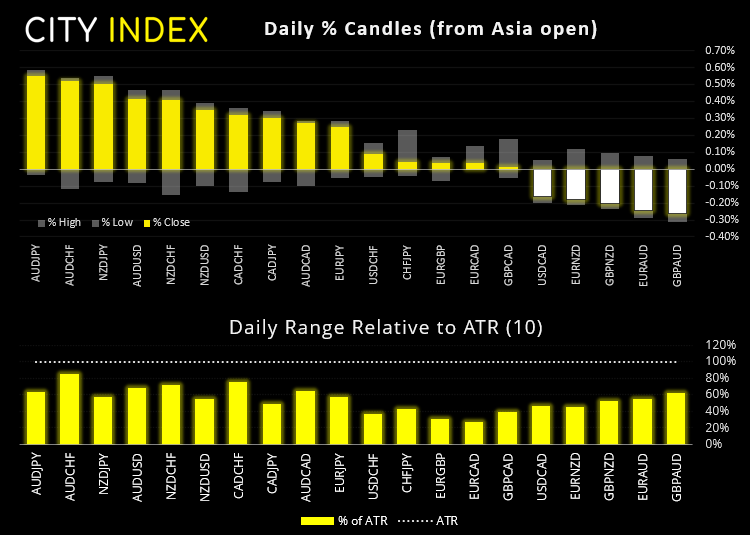

Forex:

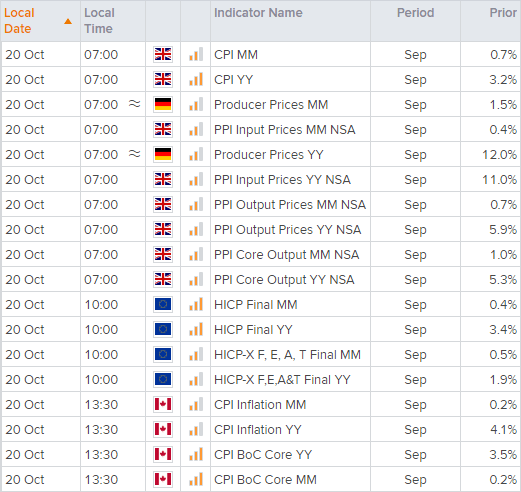

As my colleague Joe Perry pointed out, Wednesday really is inflation day – with consumer and producer price reports being released across Europe, Africa and North America. UK CPI kicks it all off at 07:00 BST which puts GBP pairs into focus for news traders. Following hawkish comments from BOE Governor Andrew Bailer, traders have been pricing in a November hike. And that means any disappointment in today’s figured could see the pound under pressure.

CPI is expected to have dipped to 0.4% in September from 0.7%, remained steady at 3.2% y/y and for Core CPI to have slipping to 3% from 3.1% prior. Conversely, should we see some punchy numbers today it will only exacerbate calls for an early rate hike and support GBP.

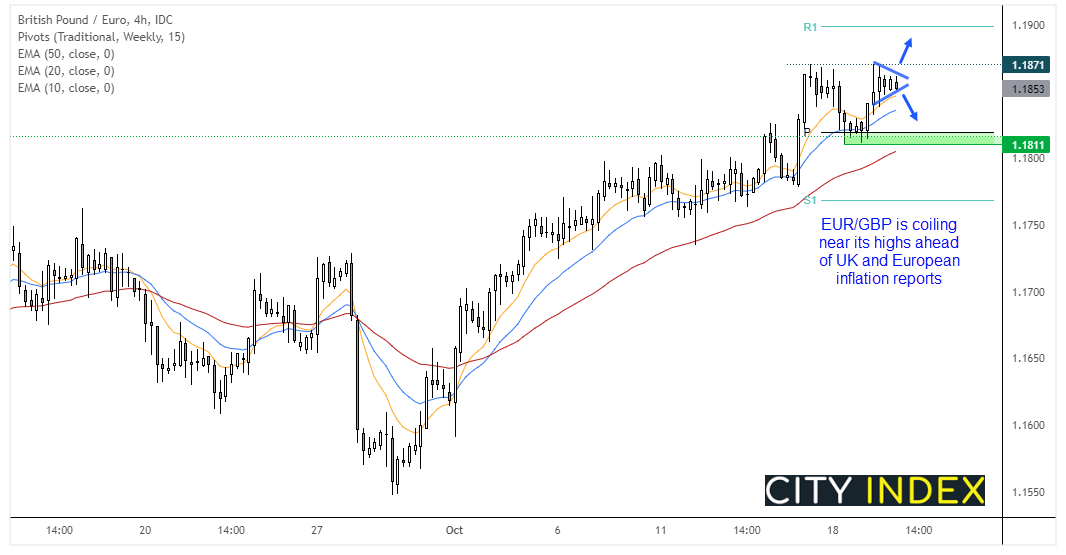

And the relative performance between European an UK’s CPI reports places EUR/GBP firmly into focus. EUR/GBP has rallied over 300 pips since September low from the 200-day eMA. It closed above the August high on Friday, then produced a bullish engulfing candle yesterday and closed near the highs.

The four-hour chart has bounced its way along the 20-bar eMA and is now coiling within a tight range ahead of these inflation reports. Today we are simply waiting to see if momentum breaks the cross to new highs or break lower from the small consolidation as part of a minor countertrend move. If it moves lower, we could then seek bullish setups above 1.1800 near the recent swing low and weekly pivot point, as the trend remains bullish overall.

Commodities:

Copper futures dipped to a 4-day low which confirmed two bearish pinbars on the daily chart. It’s holding above the July high but it is apparent a cooling-off period is required after last week’s strong rally. For now, we remain bullish above 4.50 and await further evidence is current retracement has neared completion.

Up Next (Times in BST)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 08:33 AM

Yesterday 11:48 PM

Yesterday 11:16 PM

Latest Forex articles

Yesterday 04:47 AM

April 16, 2024 12:00 PM

April 16, 2024 04:24 AM