Asian Indices:

- Australia's ASX 200 index fell by -6.7 points (-0.09%) and currently trades at 7,301.30

- Japan's Nikkei 225 index has risen by -23.26 points (0.08%) and currently trades at 29,043.15

- Hong Kong's Hang Seng index has fallen by 0 points (0%) and currently trades at 29,288.22

UK and Europe:

- UK's FTSE 100 futures are currently up 2.5 points (0.04%), the cash market is currently estimated to open at 7,138.57

- Euro STOXX 50 futures are currently down -2.5 points (-0.06%), the cash market is currently estimated to open at 4,118.16

- Germany's DAX futures are currently up 3 points (0.02%), the cash market is currently estimated to open at 15,610.97

US Futures:

- DJI futures are currently up 237.04 points (0.69%)

- S&P 500 futures are currently up 11.5 points (0.08%)

- Nasdaq 100 futures are currently up 2 points (0.05%)

Learn how to trade indices

Indices

It has been a quiet start to the week for equity markets. The ASX 200 recovered early losses which prices were under pressure as some Australian states reimpose lockdown restrictions across hotspot areas. Its currently just -0.1% lower but back above 7300 as we head towards the close. The Nikkei 225 was under pressure from technology stocks as the Nasdaq underwhelmed on Friday. After finding support at 29k, prices remained mostly within Friday’s range but higher timeframe analysis suggests it is trying to revert to its longer-term bullish trend. US and European indices mostly flat ahead of the open which points towards an uneventful open.

The FTSE 100 rose 0.37% on Friday and closed at the high of the week, rising over 2.7% since Monday’s low. Friday’s open was the low of the day and found support at its 10-day eMA. Industrial transportation stocks were the strongest performers last week, rising 6.5% by Friday’s close and 1.45% on the day. Energy stocks also had a good week, rising 4.8%. The best performers on Friday were travel and leisure stocks as the government is expected to unveil re-opening plans for fully vaccinated people.

We’d be keen to explore any bullish setups around 7120 as this mark’s Thursday’s high and Friday’s most actively traded price. If we get a clean break above Friday’s high then our bias is bullish for the da, with the next support level sitting around 7130/32 which marks Wednesday’s high and the upper value area for Friday’s range. A break beneath 7070 (Friday’s low) warns of further downside.

FTSE 350: Market Internals

FTSE 350: 4085.09 (0.37%) 25 June 2021

- 252 (71.79%) stocks advanced and 86 (24.50%) declined

- 20 stocks rose to a new 52-week high, 4 fell to new lows

- 84.33% of stocks closed above their 200-day average

- 53.85% of stocks closed above their 50-day average

- 13.68% of stocks closed above their 20-day average

Outperformers:

- + 6.68% - Ultra Electronics Holdings PLC (ULE.L)

- + 5.27% - Dr Martens PLC (DOCS.L)

- + 5.13% - John Wood Group PLC (WG.L)

Underperformers:

- -5.38% - Crest Nicholson Holdings PLC (CRST.L)

- -4.28% - Flutter Entertainment PLC (FLTRF.I)

- -2.93% - National Express Group PLC (NEX.L)

Forex: GBP loses ground to commodity currencies

The Australian dollar was lower overnight as new lockdown restrictions were imposed upon several states. 18 new cases were recorded in New South Wales but there are fears this could go much higher now the more contagious Delta variant has been detected. AUD/USD is currently -0.12% lower.

The Japanese yen was the strongest major overnight, the Swiss franc and euro were the weakest majors.

The British pound was notably lower against all three major commodity currencies last week (AUD, CAD and NZD). GBP/CAD formed a bearish engulfing week to close -0.85% lower, although it fell -1.4% against AUD. A bearish pinbar formed on GBP/CHF and GBP/EUR, with the former closing back within its nine-week rage after a failed breakout ahead of the BOE’s dovish meeting, which was the major driver behind the pounds demise over Thursday and Friday.

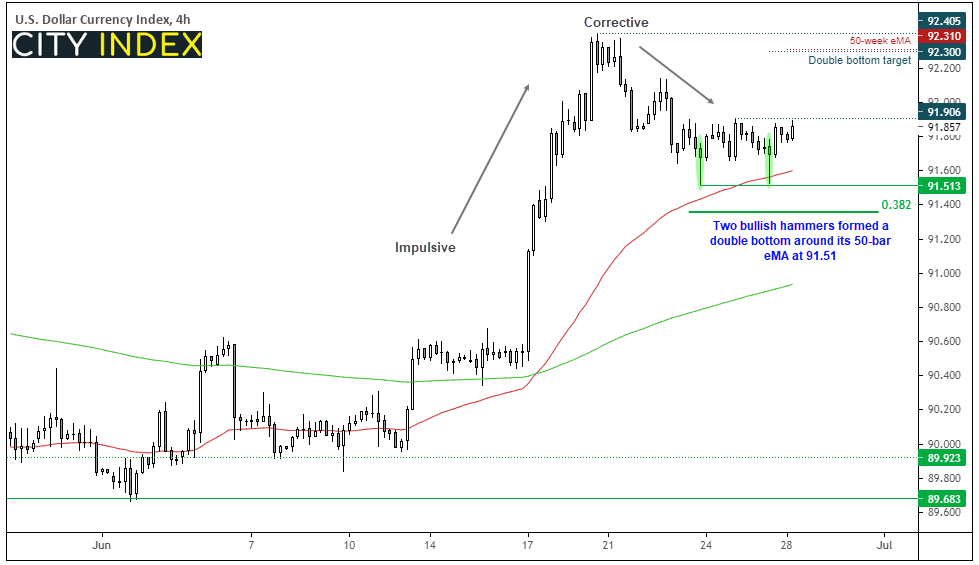

The US dollar index has formed a double bottom pattern at 91.5 with two bullish hammers (with the more recent one finding support at its 50-bar eMA on the four-hour chart). A break above 91.60 confirms the pattern and the measured move of the pattern projects an initial target around 92.30. Incidentally, this is right near the 50-week eMA which has capped as resistance for the past two weeks.

However, given there is very little in the way of news scheduled for today then its entirely possible we may lack the catalyst for a sustained breakout. In which case we would then monitor its potential for a triple bottom. Ultimately, our bias remains bullish above 91.50.

Learn how to trade forex

Commodities:

Oil prices toughed a marginal new high with WTI futures rising to 74.45, its highest level in over 2.5 years. Brent futures are currently trading at 76.12 during quiet trade, ahead of this week’s OPEC meeting on Thursday where expectations are for a mild production cut.

Gold and silver prices remain in choppy, intraday trading ranges which are more likely to favour mean reversion strategies until they break one way or another. In very loose terms gold is ranging between 1755 – 1800, although recently support is building above 1770 whilst small rallies are faltering around 1790. Traders would be wise to monitor DXY in tandem with gold prices to see if any breakout is confirmed by each market.

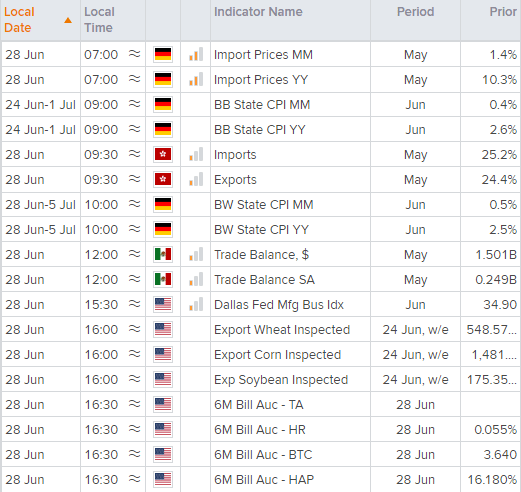

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM